China’s Unified Crackdown: RWA Deemed Illegal, No Room for “Technological Innovation”

By Liu Honglin

In a move that has sent shockwaves through the global cryptocurrency industry, China has delivered its most explicit and coordinated condemnation yet of Real World Asset (RWA) tokenization. A joint statement, signed by seven prominent Chinese financial industry associations, unequivocally labels RWA activities as illegal, signaling a fundamental shift from regulatory scrutiny to outright prohibition.

An Unprecedented Joint Warning

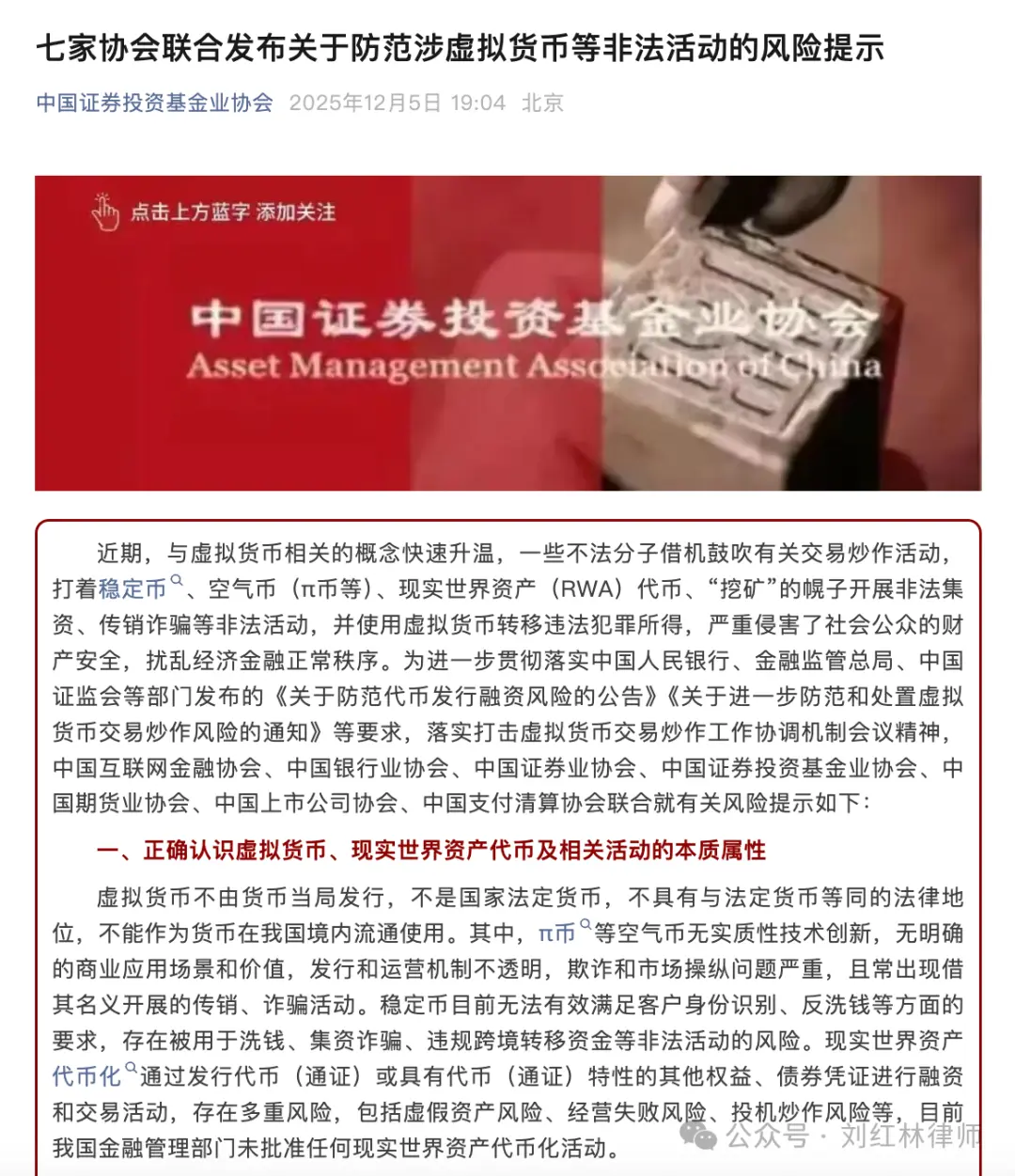

The “Risk Warning Regarding Preventing Illegal Activities Related to Virtual Currencies” was simultaneously issued by the China Internet Finance Association, China Banking Association, Securities Association of China, Asset Management Association of China, China Futures Association, China Association for Public Companies, and Payment & Clearing Association of China. This unified front, spanning the entire financial regulatory landscape, is highly unusual and typically reserved for addressing systemic financial risks.

For industry observers, the message is clear: this is no mere regulatory update, but a coordinated suppression campaign across industries and supervisory systems. The question on many minds is, “Could RWA truly pose such a systemic threat?”

RWA: From Innovation to Illegality

The document’s most striking feature is its explicit mention and qualitative assessment of RWA. For the first time, RWA is grouped alongside stablecoins, meme coins (like Pi Coin), and crypto mining as a primary form of “illegal activities related to virtual currencies.” This direct naming and shaming is a potent signal: RWA is no longer viewed as an emerging technology awaiting regulatory clarification, but rather a “risky business model” directly targeted for elimination.

The warning describes RWA as: “Financing and trading activities through the issuance of tokens or other rights and bond certificates with token characteristics, which carry multiple risks, including false asset risk, operational failure risk, and speculative trading risk. Currently, China’s financial management departments have not approved any Real World Asset tokenization activities.”

This statement draws three critical red lines:

- RWA as “Financing and Trading Activities”: Regardless of underlying asset or blockchain use, RWA is fundamentally a fundraising mechanism. Any involvement in token issuance, asset trading, or profit distribution automatically places it under the existing financial legal framework, specifically within the prohibitions of laws like the “Securities Law” and “Measures for the Prohibition of Illegal Financial Institutions and Illegal Financial Business Activities.”

- Emphasis on Inherent Risks: Regulators highlight “false asset risk,” “operational failure risk,” and “speculative trading risk.” This goes beyond condemning fraudulent schemes; it preemptively dismisses the potential market risks of even “legitimate” projects. The regulatory stance is that RWA token structures cannot guarantee legal ownership or liquidation capabilities of underlying assets, leading to uncontrollable risk spillovers.

- Zero Approval: The most definitive statement: “China’s financial management departments have not approved any Real World Asset tokenization activities.” This declaration strips all RWA-related assets, services, platforms, and trading activities of any legal operational basis. There is no room for arguments of “regulatory exploration” or “awaiting approval.”

Legal Ramifications and Enforcement

For some time, RWA has been seen by many in the industry as an “alternative tokenization path” to circumvent tightening stablecoin regulations, often leveraging “real asset anchoring” or “offshore compliance.” This new document, however, systematically dismantles these justifications.

The warning explicitly links RWA activities to severe legal risks such as “illegal fundraising, unauthorized public issuance of securities, and illegal operation of futures businesses.” These are not vague threats but direct references to specific articles in China’s Criminal Law and Securities Law:

- Issuing RWA tokens to the public for fundraising may constitute illegal fundraising.

- Facilitating transactions or distributing tokens without proper authorization could be deemed illegal issuance of securities.

- RWA transactions involving leverage or gambling mechanisms may lead to charges of illegally operating futures businesses.

These legal applications are well-established, with numerous court judgments in recent years applying similar logic to crypto-related cases. RWA is not a novel legal challenge but a “familiar target” within existing financial enforcement tools.

The Scapegoat: Rising Fraud

The timing of this stringent warning is no coincidence. It directly correlates with a surge in fraudulent activities operating under the guise of RWA. The document’s opening paragraph explicitly states: “Unlawful elements take the opportunity to promote relevant trading and speculation activities, using the guise of stablecoins, meme coins (e.g., Pi Coin), Real World Asset (RWA) tokens, and ‘mining’ to conduct illegal fundraising, pyramid schemes, and other illegal activities.” This places RWA on the same risk level as notorious scams, reflecting the alarming frequency of cases and significant societal harm observed by enforcement agencies.

Unpacking “Joint Liability”: A Game Changer

Perhaps the most far-reaching aspect of this notice is its emphasis on the joint liability of service institutions and intermediaries. The document warns: “Domestic personnel of relevant overseas virtual currency and Real World Asset token service providers, as well as domestic institutions and individuals who knowingly or should know that they are engaged in virtual currency-related businesses and still provide services for them, will be held accountable according to law.”

This statement has profound implications:

- It targets not only project founders but the entire ecosystem of service providers: project planners, tech outsourcers, marketing agents, KOLs, and payment gateway providers.

- “Knowingly or should know” establishes a legal presumption of liability, extending beyond subjective intent. If an objective basis for reasonable judgment exists, liability can be assigned.

- It closes a common loophole in the Web3 industry: even if a company is registered overseas, if its team operates from China or provides services to the Chinese market, it cannot escape the definition of “providing services domestically.”

This means that arguments like “we’re just a pure technology company” or “we only provide infrastructure” are no longer valid defenses. If you are aware a project is conducting RWA activities in China and choose to provide services, you risk legal accountability.

No Room for “Technical Innovation” Defense

This policy effectively terminates the entire Web3 service chain built around RWA within China. Not only are RWA projects themselves prohibited, but the commercial logic for supporting services also ceases to exist. For future RWA teams, the only viable path is “complete overseas relocation.” Every aspect—legal structure, asset custody, user access, compliance auditing, and financial services—must be entirely detached from the Chinese market, leaving no domestic footprint or residual links. Even hiring an operations staff member in China could trigger legal risks.

Many projects have attempted to argue for policy space based on “technological innovation,” highlighting on-chain settlement efficiency, asset transfer transparency, or proposing “technical solutions” like KYC integration and multi-layered audit structures. However, the regulatory signal is unequivocally clear: this is not a technical or mechanism problem. The perceived financial risks far outweigh any potential technological benefits. The absence of terms like “technology pilot,” “classified regulation,” or “prudent development” in the warning indicates that the regulatory goal is not to optimize RWA operations but to explicitly exclude them from legitimate boundaries.

A “Fundamental Rejection,” Not Just Regulation

This is not merely a policy tightening; it is a complete directional negation. It dismantles the foundational premise of the entire RWA model. Whether tokens are distributed via SPV structures or underlying rights are managed with on-chain contracts, if the ultimate structure possesses “financing + trading” attributes, it falls squarely within the definition of illegal financial activities. Projects still expanding their reach in Chinese social media groups (WeChat, Telegram, X/Twitter) under the guise of “node partners” or “regional representatives” are no longer considered marginal explorations but are directly classified as participating in illegal activities.

For domestic teams, this means the entire RWA narrative—from asset origination and tech development to market matchmaking and supporting consulting, outsourcing, and promotional services—lacks any sustainable business logic. Any Chinese node in the chain constitutes a potential risk.

For international projects, the situation is equally stark. China is no longer a market “awaiting regulatory clarity” but a region that has explicitly expressed a stance of rejection—not a pause, not a wait-and-see, but an explicit exclusion.

In this new landscape, the choices for practitioners are unambiguous: either completely relocate their business operations to a compliant system with no intersection with Chinese regulation, or completely abandon RWA.

(The above content is an excerpt and reproduction authorized by partner PANews, original link | Source: Manku Blockchain)

Disclaimer: This article is for market information purposes only. All content and views are for reference only, do not constitute investment advice, and do not represent the views and positions of BlockTempo. Investors should make their own decisions and transactions. The author and BlockTempo will not bear any responsibility for direct or indirect losses incurred by investors’ transactions.