Grayscale’s 2026 Digital Asset Outlook: The Dawn of Institutional Crypto

This article, compiled by Peggy for BlockBeats, summarizes Grayscale’s “Digital Asset Outlook 2026.”

The cryptocurrency market is undergoing a profound transformation. After years defined by volatile, narrative-driven retail cycles, digital assets are now entering a new, more mature phase. This shift is primarily fueled by rising global demand for alternative stores of value, a rapidly maturing regulatory landscape, and the increasing integration of spot Exchange Traded Products (ETPs), stablecoin legislation, and institutional capital allocations. These forces are fundamentally reshaping how funds flow into the crypto ecosystem.

Grayscale’s core thesis in its 2026 outlook is clear: the crypto market’s driving force is transitioning from speculative retail enthusiasm to the steady hand of institutional capital. Price movements will increasingly be dictated by compliant investment channels, long-term funding, and sustainable fundamentals, signaling the potential end of the traditional “4-year cycle” narrative.

This report meticulously outlines 10 pivotal investment themes poised to shape the market in 2026. From the role of digital assets as a store of value and the proliferation of stablecoins to asset tokenization, decentralized finance (DeFi), AI integration, and privacy infrastructure, these themes paint a picture of a crypto ecosystem progressively embedding itself within the mainstream financial system. Furthermore, the report critically identifies popular topics likely to be “noise” rather than significant market drivers in the short term.

Key Takeaways for 2026

Grayscale anticipates that 2026 will be a year of accelerated structural shifts in digital asset investment, underpinned by two dominant forces:

- **Growing Macro Demand for Alternative Value Stores:** Global economic uncertainties are driving investors to seek transparent, programmable, and scarce digital assets like Bitcoin and Ethereum.

- **Significant Regulatory Clarity:** The evolving regulatory environment is paving the way for broader adoption and institutional participation.

These combined trends are expected to unlock new capital sources, expand digital asset adoption among wealth management advisors and institutional investors, and further integrate public blockchains into core financial infrastructure. Consequently, Grayscale projects an overall increase in digital asset valuations in 2026, marking the potential conclusion of the “4-year cycle.” Bitcoin, in particular, is expected to reach new all-time highs in the first half of the year.

- Bipartisan Legislation: Grayscale forecasts that bipartisan-supported structural legislation for the crypto market will officially become law in the US by 2026. This will solidify blockchain finance’s role in US capital markets, enable compliant trading of digital asset securities, and open doors for on-chain issuances by both startups and established enterprises.

- Scarcity & Fiat Uncertainty: Amidst rising uncertainty in the fiat currency system, the programmatic scarcity of assets like Bitcoin (with the 20 millionth BTC projected to be mined in March 2026) and Ethereum will drive increased demand.

- ETP Expansion & Institutional Inflow: The success of crypto ETPs, which began a strong rollout in 2024, is set to continue. As more platforms complete due diligence and integrate digital assets into allocation processes, a steady influx of institutional capital is expected throughout 2026.

Grayscale has identified 10 critical investment themes for 2026, reflecting the diverse and expanding applications of public blockchain technology:

- USD Devaluation Risk Fuels Demand for Monetary Alternatives

- Enhanced Regulatory Clarity Drives Widespread Digital Asset Adoption

- Stablecoin Influence Expands Post-GENIUS Act

- Asset Tokenization Reaches a Critical Inflection Point

- Mainstream Blockchain Adoption Increases Demand for Privacy Solutions

- AI Centralization Spurs Demand for Blockchain-Based Solutions

- DeFi Accelerates, Led by Lending Protocols

- Mainstream Adoption Necessitates Next-Generation Infrastructure

- Increased Focus on Sustainable Revenue Models

- Investors Will “Default” to Staking for Yield

Conversely, Grayscale highlights two topics that, despite significant media attention, are unlikely to materially impact the crypto market in 2026:

- **Quantum Computing:** While research into post-quantum cryptography will advance, its market valuation impact is not expected within the next year.

- **Digital Asset Treasury Companies (DATs):** Despite past hype, DATs are unlikely to be a decisive market variable in 2026, with demand having cooled and forced selling being improbable.

2026 Digital Asset Outlook: The Dawn of the Institutional Era

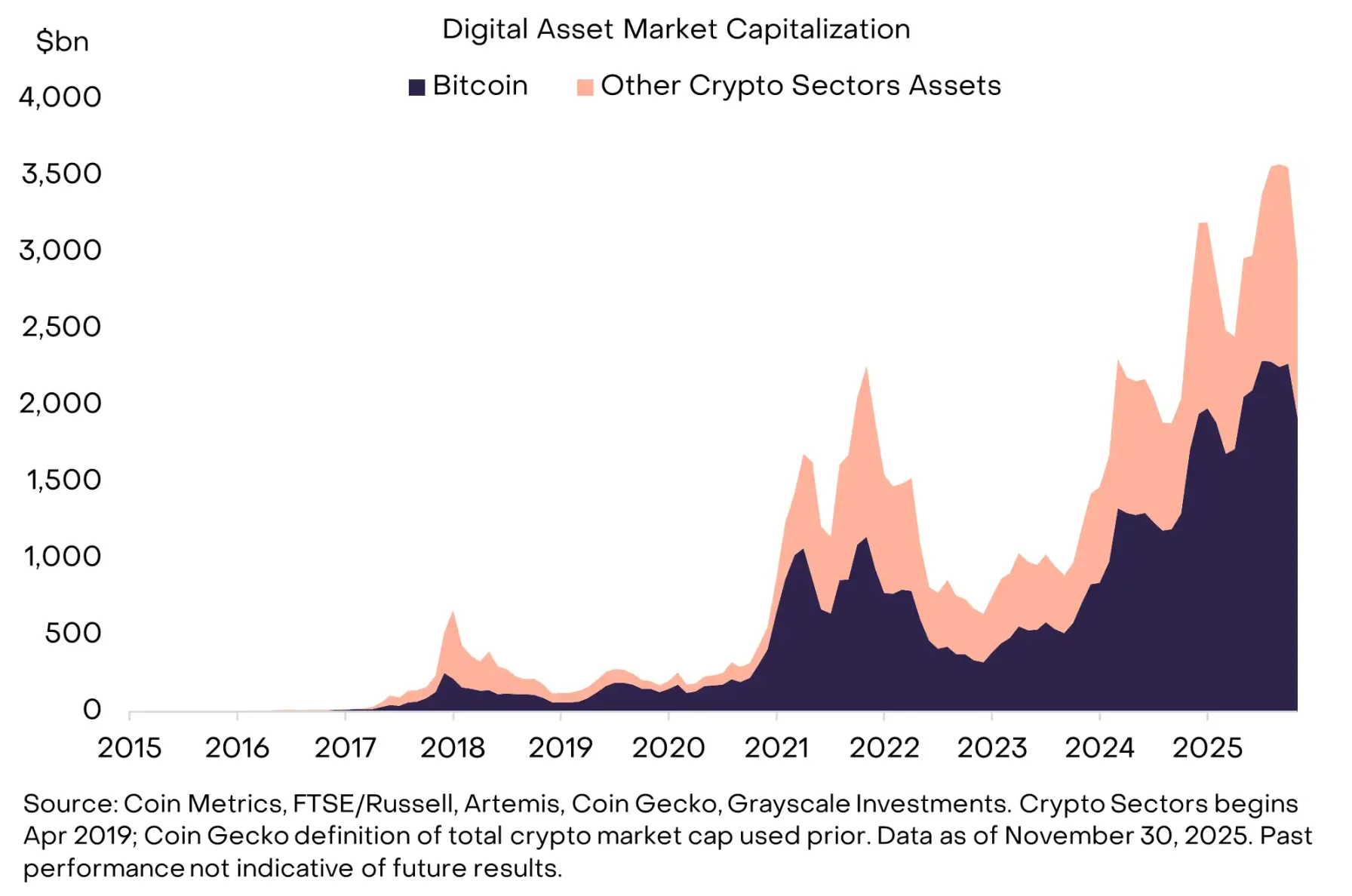

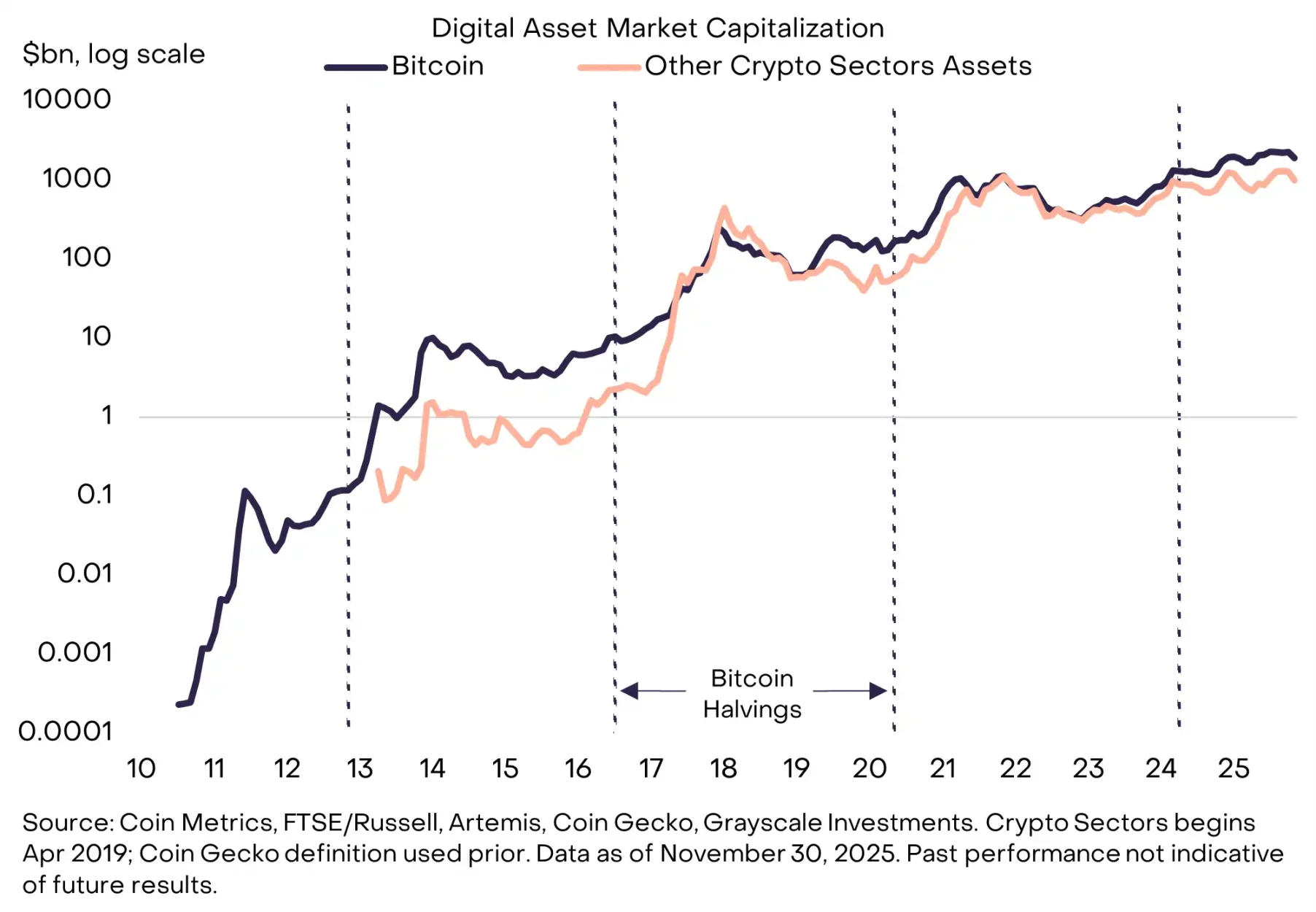

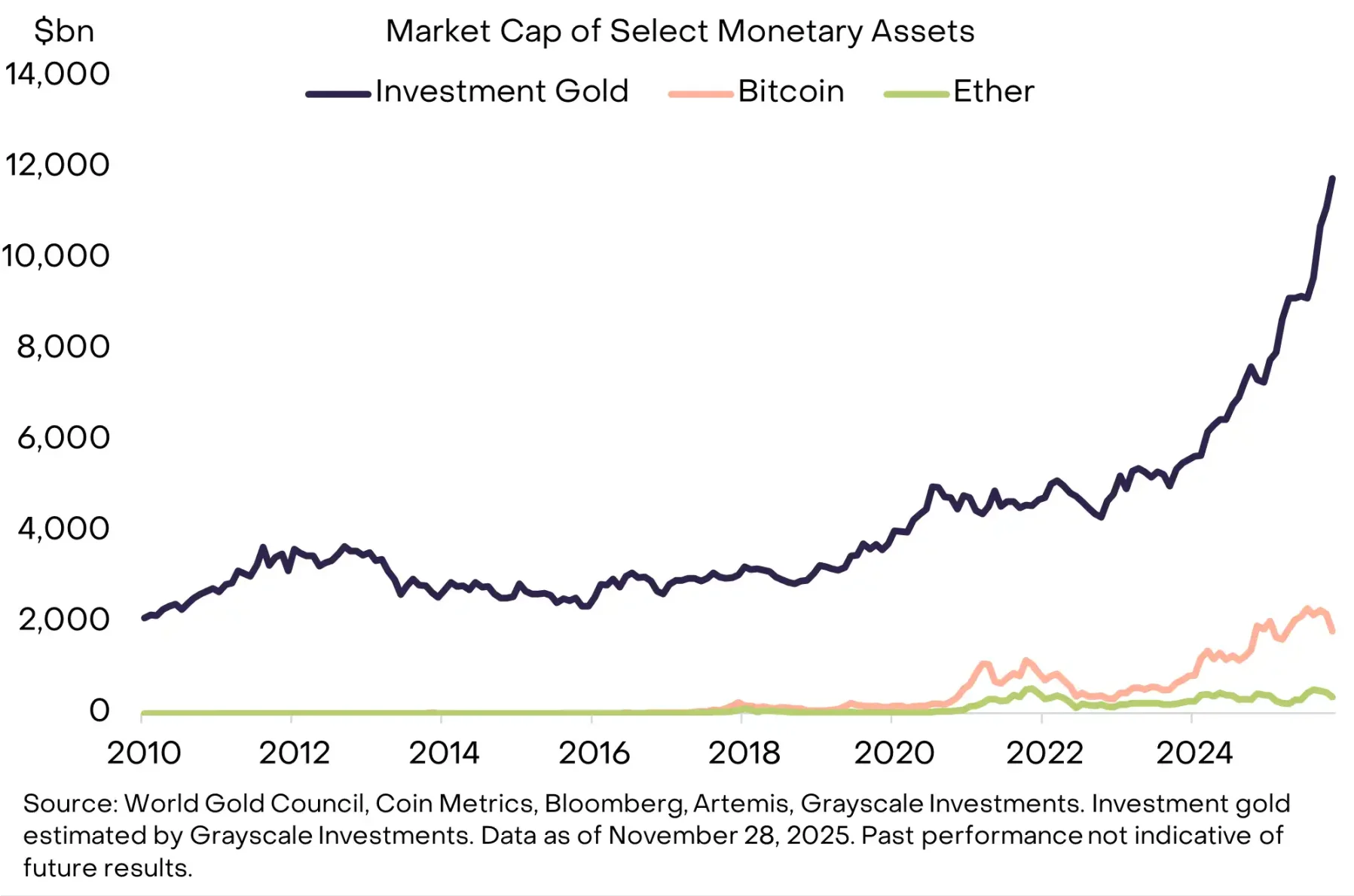

From an experimental concept fifteen years ago—a single asset, Bitcoin, valued at roughly $1 million—cryptocurrency has blossomed into a thriving industry. Today, it stands as a medium-sized alternative asset class, comprising millions of tokens with a collective market capitalization nearing $3 trillion.

This remarkable growth is paralleled by an accelerating convergence between public blockchains and traditional financial systems. As major economies establish clearer regulatory frameworks, this integration is attracting a steady flow of long-term, allocation-driven capital, fundamentally altering the market’s dynamics.

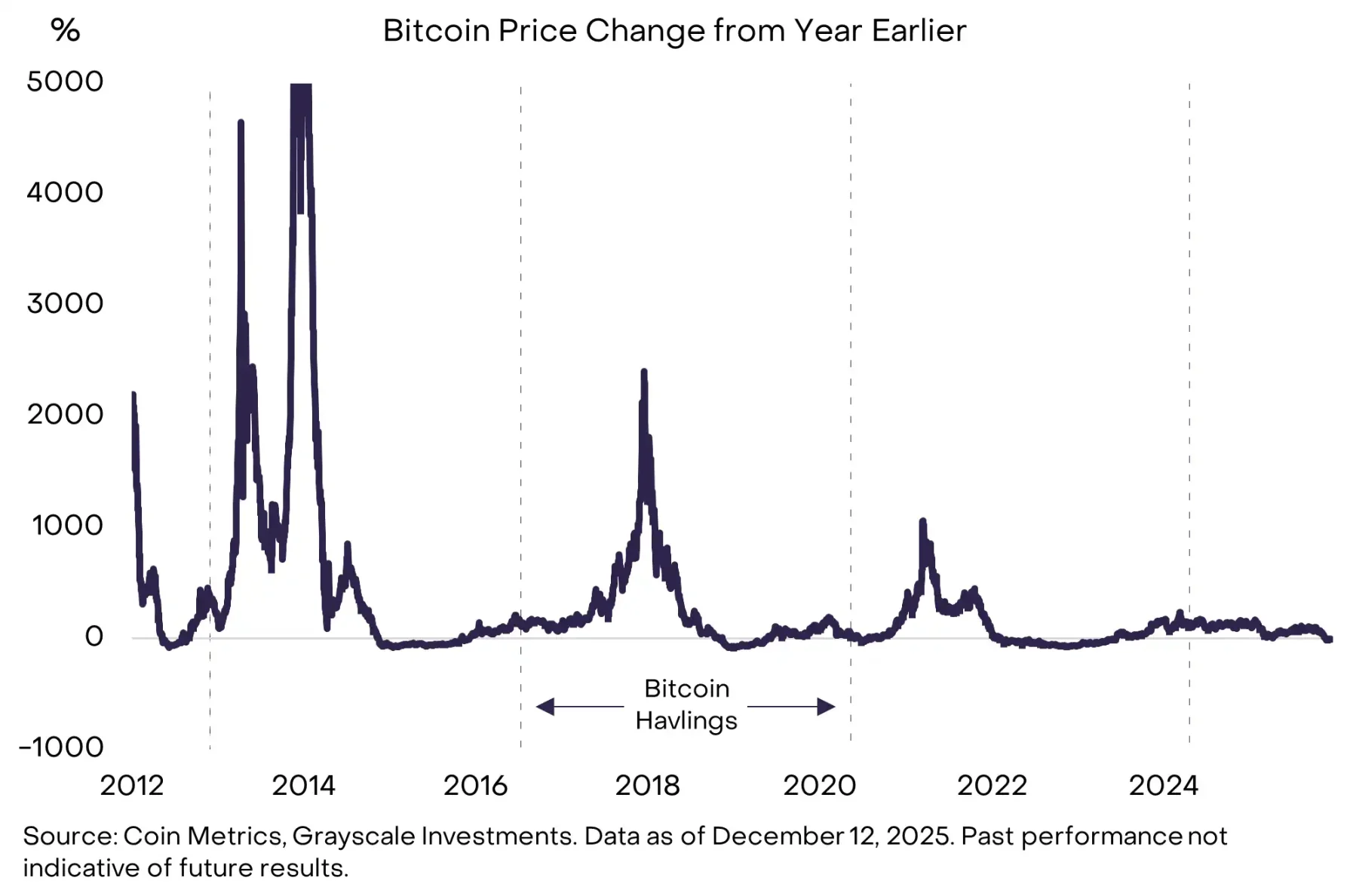

Historically, token valuations have experienced four significant cyclical drawdowns, typically occurring approximately every four years. Three of these cyclical peaks followed Bitcoin’s halving events by 1 to 1.5 years, with halvings themselves occurring on a four-year cycle.

Given that the current bull market has persisted for over three years, and the most recent Bitcoin halving occurred in April 2024 (over 1.5 years ago), some market observers, relying on historical patterns, predict a potential Bitcoin price peak in October and a challenging year for crypto returns in 2026.

However, Grayscale posits that the crypto asset class is in a sustained bull market, and 2026 will mark the decisive end of the “4-year cycle” paradigm. We foresee comprehensive valuation growth across the six primary crypto asset sectors, with Bitcoin projected to surpass its previous all-time high in the first half of 2026.

Our optimistic outlook rests on two foundational pillars:

1. Persistent Macro Demand for Alternative Stores of Value

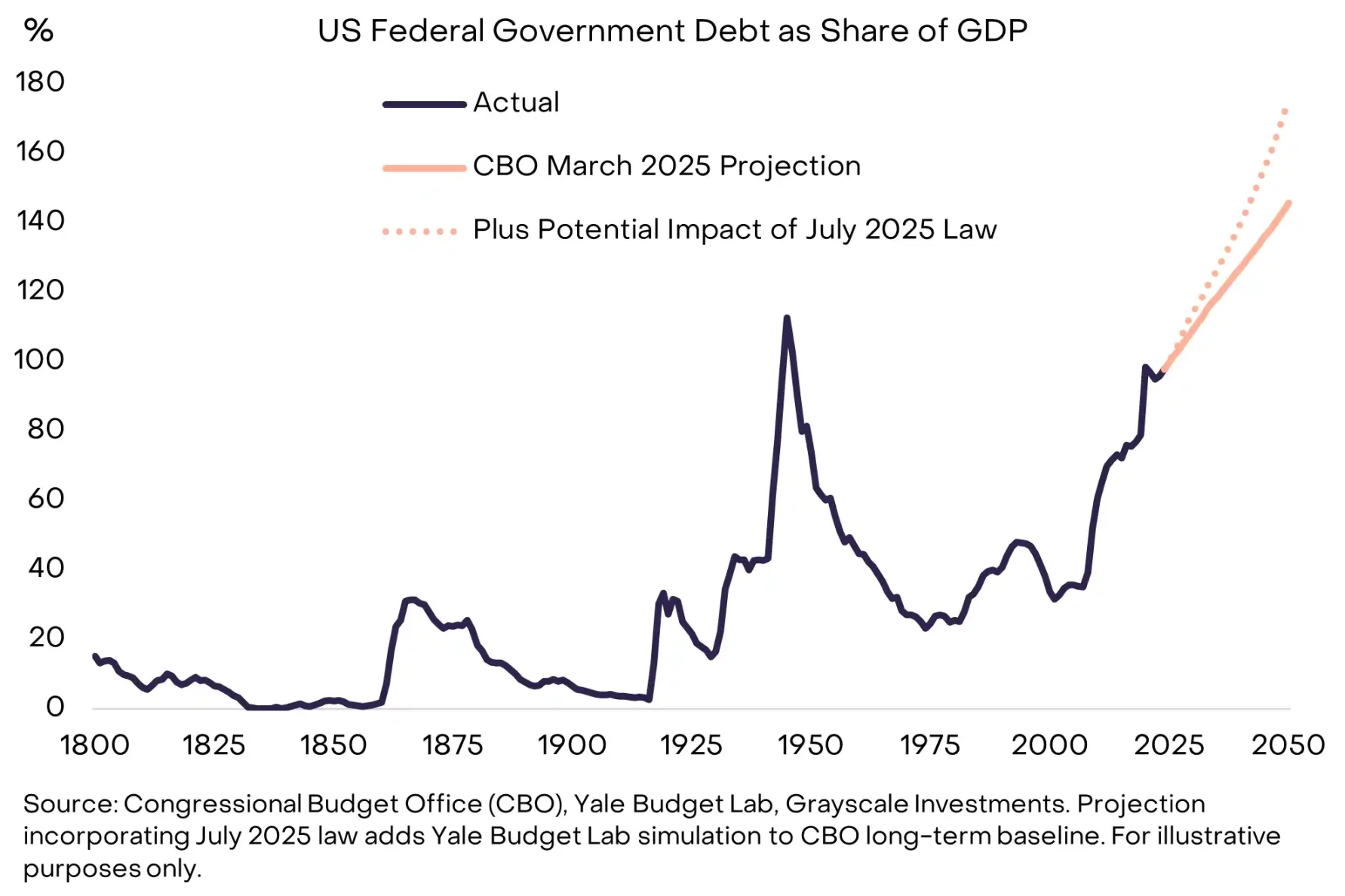

Bitcoin and Ethereum, the two largest crypto assets by market capitalization, are increasingly recognized as scarce digital commodities and alternative monetary assets. This recognition is amplified by the growing instability within the fiat currency system, where burgeoning public sector debt poses a medium- to long-term inflationary risk.

In this environment, scarce commodities—be they physical gold and silver, or digital counterparts like Bitcoin and Ethereum—serve as crucial portfolio hedges against fiat currency debasement. We believe that as long as the risks associated with fiat currency devaluation persist, the demand for Bitcoin and Ethereum within investment portfolios will continue to strengthen.

2. Regulatory Clarity Driving Institutional Capital into Public Blockchains

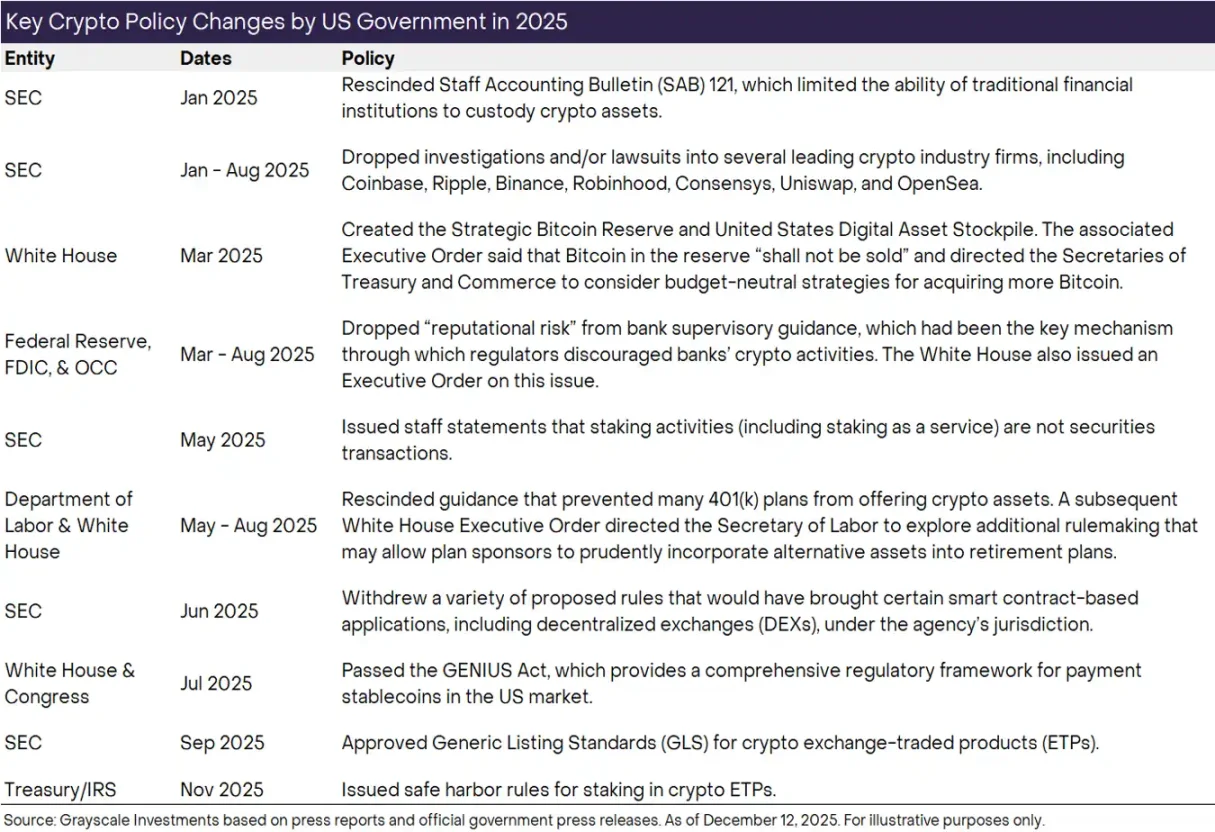

It’s easy to overlook the significant regulatory headwinds the US crypto industry faced until recently, with leading entities like Coinbase, Ripple, Binance, Robinhood, Consensys, Uniswap, and OpenSea under investigation or litigation. Even now, spot market exchanges and intermediaries often lack clear, unified regulatory guidance.

Yet, a perceptible shift is underway:

- In 2023, Grayscale’s landmark victory against the US Securities and Exchange Commission (SEC) paved the way for crypto spot ETPs.

- 2024 saw the official launch of Bitcoin and Ethereum spot ETPs.

- 2025 brought the passage of the GENIUS Act for stablecoins by the US Congress, coupled with a notable shift in regulatory attitudes towards collaboration and clearer guidance, alongside continued emphasis on consumer protection.

- By 2026, Grayscale anticipates the passage of bipartisan structural legislation for the crypto market. This will institutionally embed blockchain finance within US capital markets, fostering sustained institutional investment inflows.

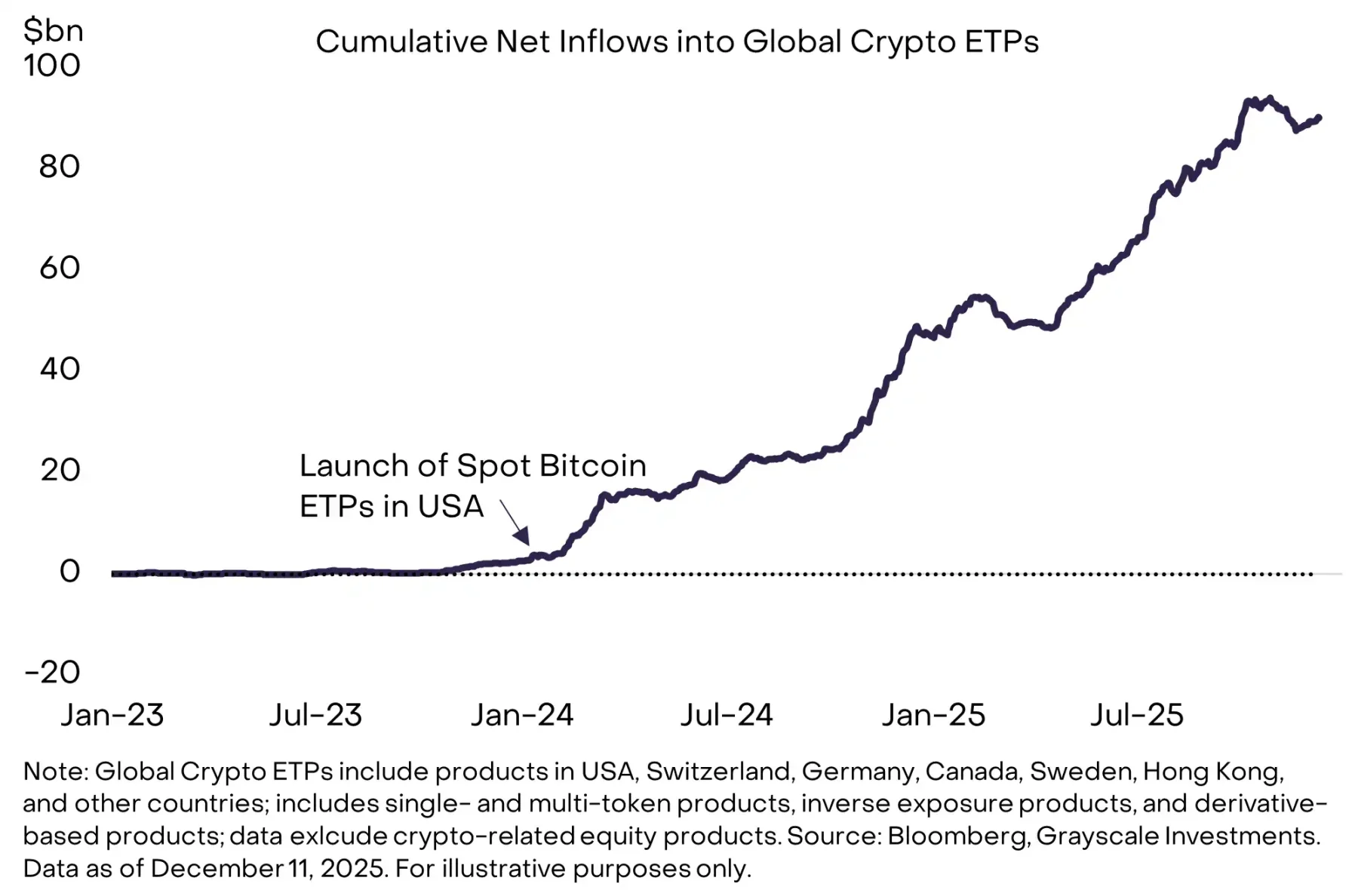

The primary conduit for new capital entering the crypto ecosystem is expected to be spot ETPs. Since the US launch of Bitcoin spot ETPs in January 2024, global crypto ETPs have collectively registered approximately $87 billion in net inflows.

Despite this impressive initial success, the integration of crypto assets into mainstream investment portfolios remains in its nascent stages. Grayscale estimates that less than 0.5% of US fiduciary/advisor-managed wealth is currently allocated to crypto. This percentage is poised for significant growth as more investment platforms complete their due diligence, establish capital market assumptions, and incorporate crypto assets into their model portfolios.

Beyond wealth management channels, pioneering institutions like Harvard Management Company and Mubadala (an Abu Dhabi sovereign wealth fund) have already integrated crypto ETPs into their portfolios. We anticipate this list of institutional adopters will expand considerably by 2026.

As institutional capital increasingly drives the crypto market, the characteristics of price performance are evolving. Unlike previous bull markets where Bitcoin saw annual surges of at least 1,000%, the current cycle’s peak annual increase has been around 240% (as of March 2024).

This divergence, in our view, reflects a pattern of robust, sustained institutional buying rather than the emotional, retail-driven rallies of past cycles. While crypto asset investment still carries inherent risks, we believe the probability of a deep, prolonged cyclical drawdown is relatively low. Instead, a smoother, more gradual upward price trend, propelled by continuous institutional inflows, is likely to dominate next year’s market.

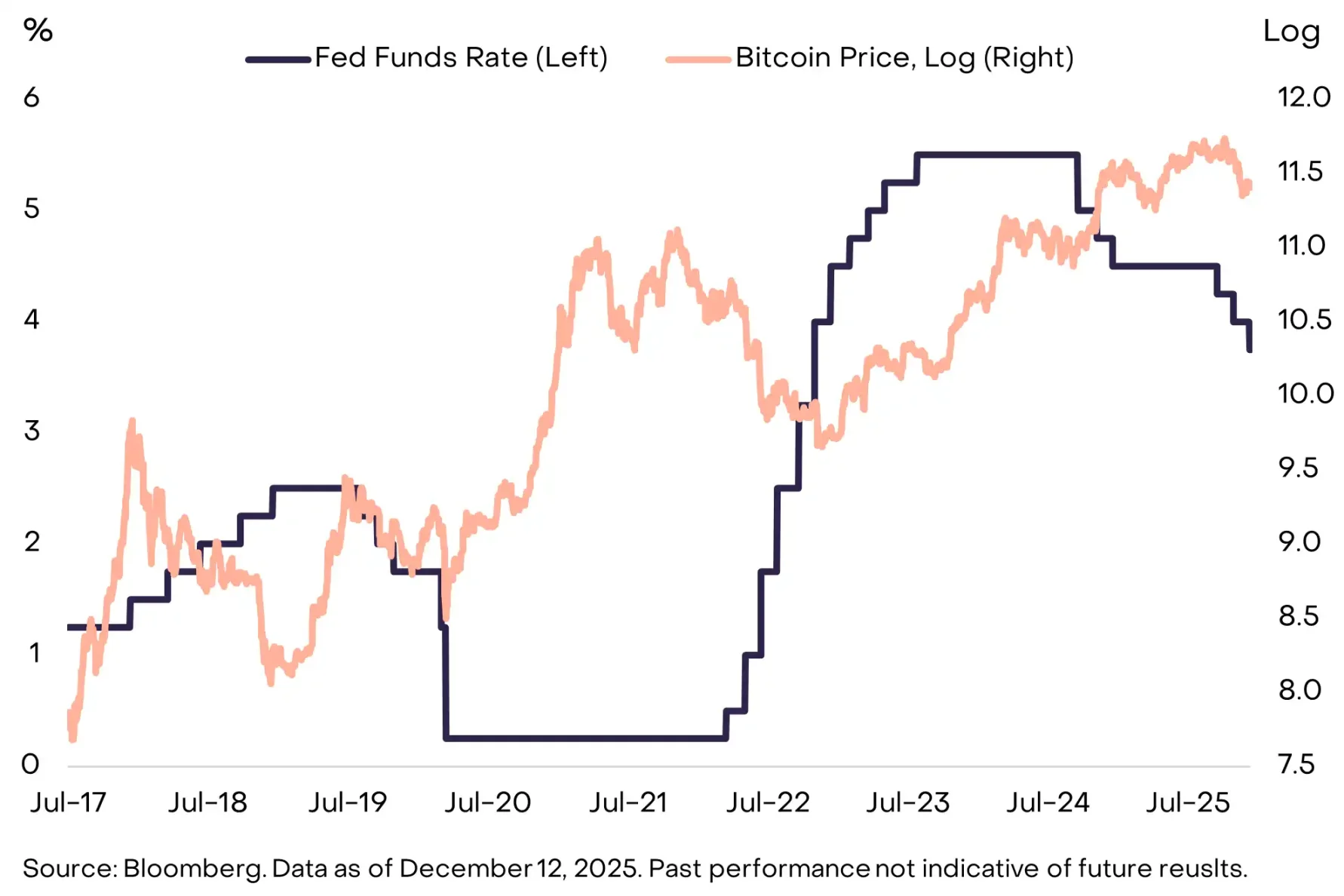

A favorable macro market environment is also expected to cushion potential downside risks for token prices in 2026. Historically, the previous two cyclical peaks coincided with periods of Federal Reserve interest rate hikes. In stark contrast, the Fed implemented three rate cuts in 2025 and is projected to continue lowering rates next year.

Kevin Hassett, a potential successor to Fed Chair Powell, recently remarked on “Face the Nation” that “the American people can expect President Trump to choose someone who will help them get cheaper car loans and easier housing mortgages at lower rates.” This sentiment underscores a broader trend. Generally, economic growth coupled with accommodative Fed policy tends to boost investor risk appetite, creating a fertile ground for risk assets, including cryptocurrencies.

Like all asset classes, crypto prices are influenced by both fundamentals and capital flows. While commodity markets are cyclical, and crypto assets may experience prolonged drawdowns in the future, we believe the conditions for such a downturn are not present in 2026.

Fundamentally, the drivers remain strong: sustained macro demand for alternative stores of value and institutional capital entry due to regulatory clarity are establishing a long-term foundation for public blockchain technology. Concurrently, new capital continues to flow into the market. By the end of next year, crypto ETPs are likely to be a staple in an increasing number of investment portfolios. This cycle is characterized not by a singular, concentrated wave of retail speculation, but by consistent, stable allocation demand for crypto ETPs across diverse portfolios. In a generally supportive macro environment, we believe this sets the stage for the crypto asset class to reach new highs in 2026.

Top 10 Crypto Investment Themes for 2026

The crypto asset class is remarkably diverse, reflecting the myriad applications of public blockchain technology. Below, Grayscale outlines its top 10 crypto investment themes for 2026, along with two “red herrings.” For each theme, we highlight the most relevant tokens from our perspective. For a deeper understanding of digital asset classifications, refer to our Crypto Sectors framework.

Theme 1: USD Devaluation Risk Fuels Demand for Monetary Alternatives

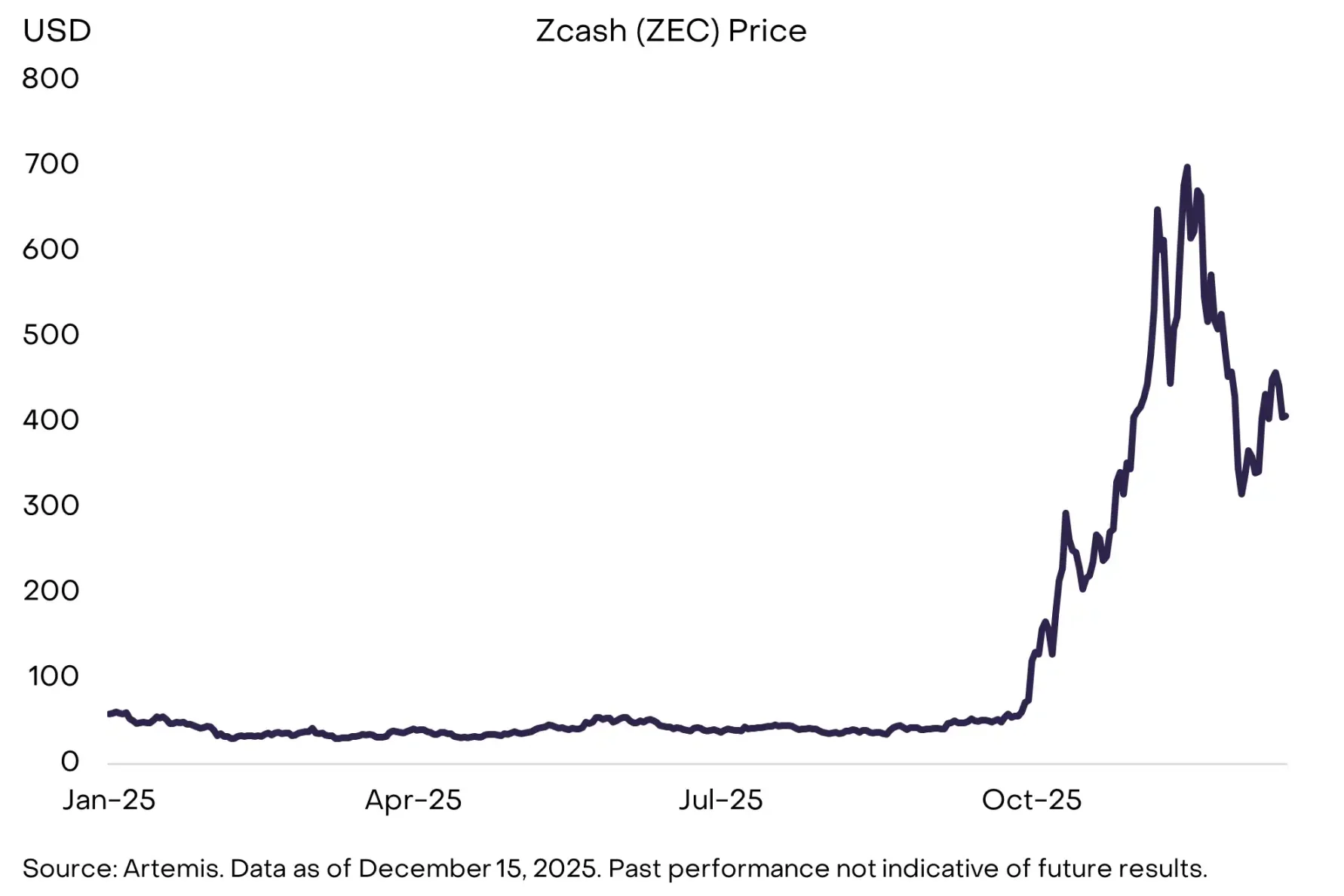

Relevant Crypto Assets: BTC, ETH, ZEC

The US economy faces structural debt challenges, which could pressure the dollar’s long-term status as a store of value. While similar issues exist globally, the dollar’s role as the world’s preeminent international currency makes US policy credibility paramount for cross-border capital flows.

We believe only a select few digital assets possess the viability to serve as effective stores of value. These assets must demonstrate broad adoption, highly decentralized network structures, and constrained supply growth. Bitcoin and Ethereum, the two largest by market cap, are prime examples. Their value, akin to physical gold, derives partly from their inherent scarcity and autonomy.

Bitcoin’s total supply is programmatically capped at 21 million, with the 20 millionth coin expected to be mined in March 2026. This transparent, predictable, and ultimately scarce digital monetary system, while conceptually simple, gains increasing appeal amidst the tail risks facing the fiat system. As macro imbalances exacerbating fiat currency risks persist, demand for alternative store-of-value assets in portfolios is likely to continue rising.

Additionally, Zcash (ZEC), a smaller, privacy-focused decentralized digital currency, may also serve as a valuable portfolio allocation for hedging against USD devaluation risks (further discussed in Theme 5).

Theme 2: Enhanced Regulatory Clarity Drives Widespread Digital Asset Adoption

Relevant Crypto Assets: Nearly All

2025 marked a pivotal year for crypto regulatory clarity in the US. Key developments included the passage of the GENIUS Act for stablecoins, the revocation of SEC Staff Accounting Bulletin 121 (SAB 121), the introduction of common listing standards for crypto ETPs, and initial steps to address the crypto industry’s access to traditional banking services.

Looking to 2026, we anticipate an even more decisive step: the passage of bipartisan structural legislation for the crypto market. While specific terms are still under negotiation, this legislation, conceptually aligned with the House-passed “Clarity Act,” aims to provide a comprehensive regulatory framework for crypto capital markets. This framework will cover registration, disclosure requirements, asset classification, and insider conduct standards, mirroring traditional finance.

In practical terms, a more complete regulatory environment across the US and other major economies means regulated financial institutions will likely integrate digital assets into their balance sheets and conduct transactions on blockchains. This also promises to foster on-chain capital formation, allowing both startups and established companies to issue compliant on-chain tokens. By unlocking blockchain’s full potential, regulatory clarity is expected to collectively elevate the overall value of the crypto asset class.

Given the critical role of regulatory clarity in 2026, any significant bipartisan divergence or breakdown in this legislative process should be considered a major downside risk.

Theme 3: Stablecoin Influence Expands Post-GENIUS Act

Relevant Crypto Assets: ETH, TRX, BNB, SOL, XPL, LINK

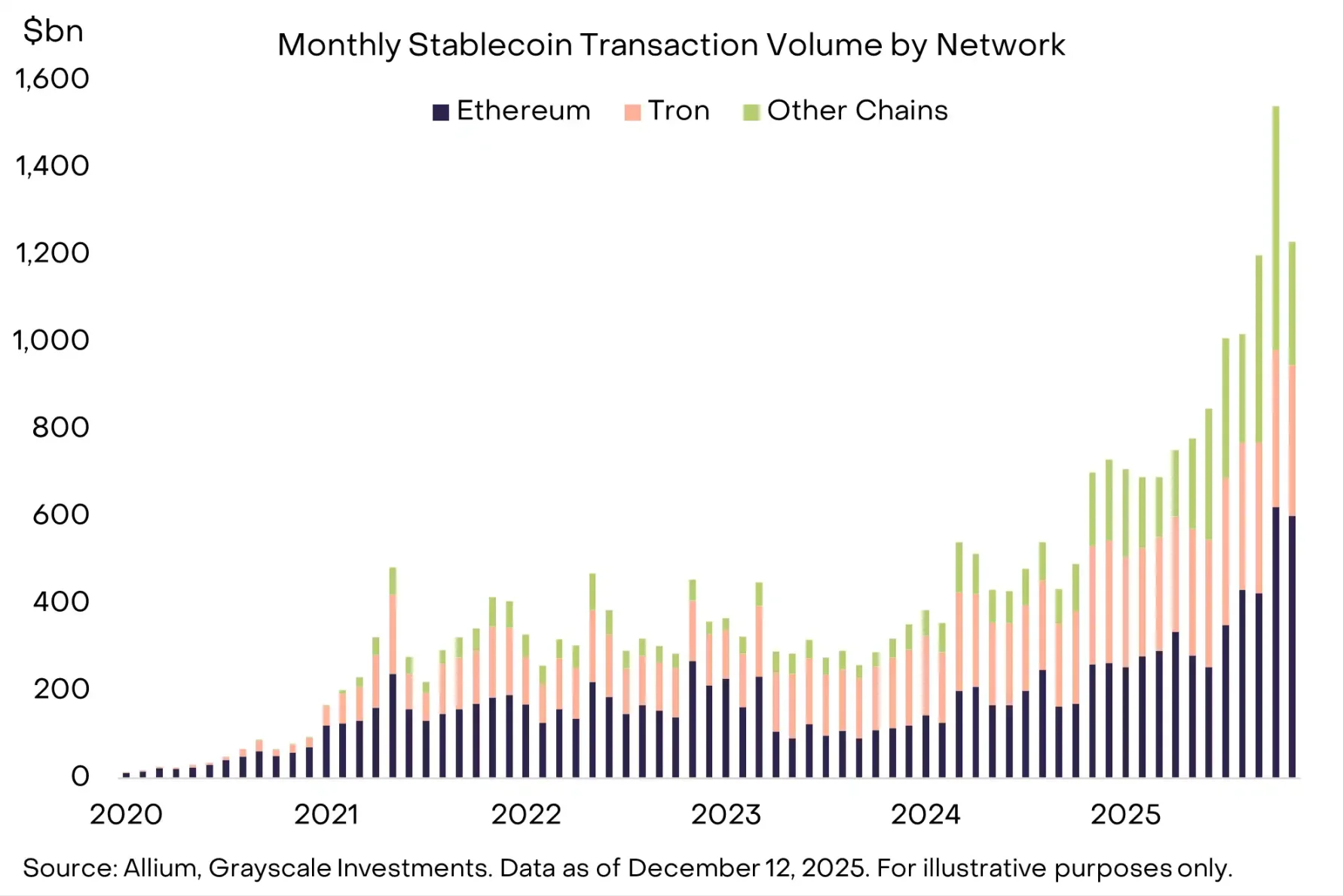

2025 was the year stablecoins truly broke into the mainstream. Their circulating supply surged to approximately $300 billion, with an average monthly transaction volume of around $1.1 trillion over the six months ending November. This growth was further propelled by the passage of the GENIUS Act in the US Congress, attracting a significant acceleration of institutional capital into the sector.

For 2026, we expect these shifts to translate into tangible, widespread applications. Stablecoins will become more deeply embedded in cross-border payments, serve as collateral for derivatives exchanges, appear on corporate balance sheets, and emerge as a viable alternative to credit cards for online consumer payments. The continued growth of prediction markets may also generate additional demand for stablecoins.

Sustained growth in stablecoin transaction volumes will directly benefit the underlying blockchain networks (e.g., ETH, TRX, BNB, SOL) and drive the development of supporting infrastructure (e.g., LINK) and decentralized finance (DeFi) applications (as detailed in Theme 7).

Theme 4: Asset Tokenization Reaches a Critical Inflection Point

Relevant Crypto Assets: LINK, ETH, SOL, AVAX, BNB, CC

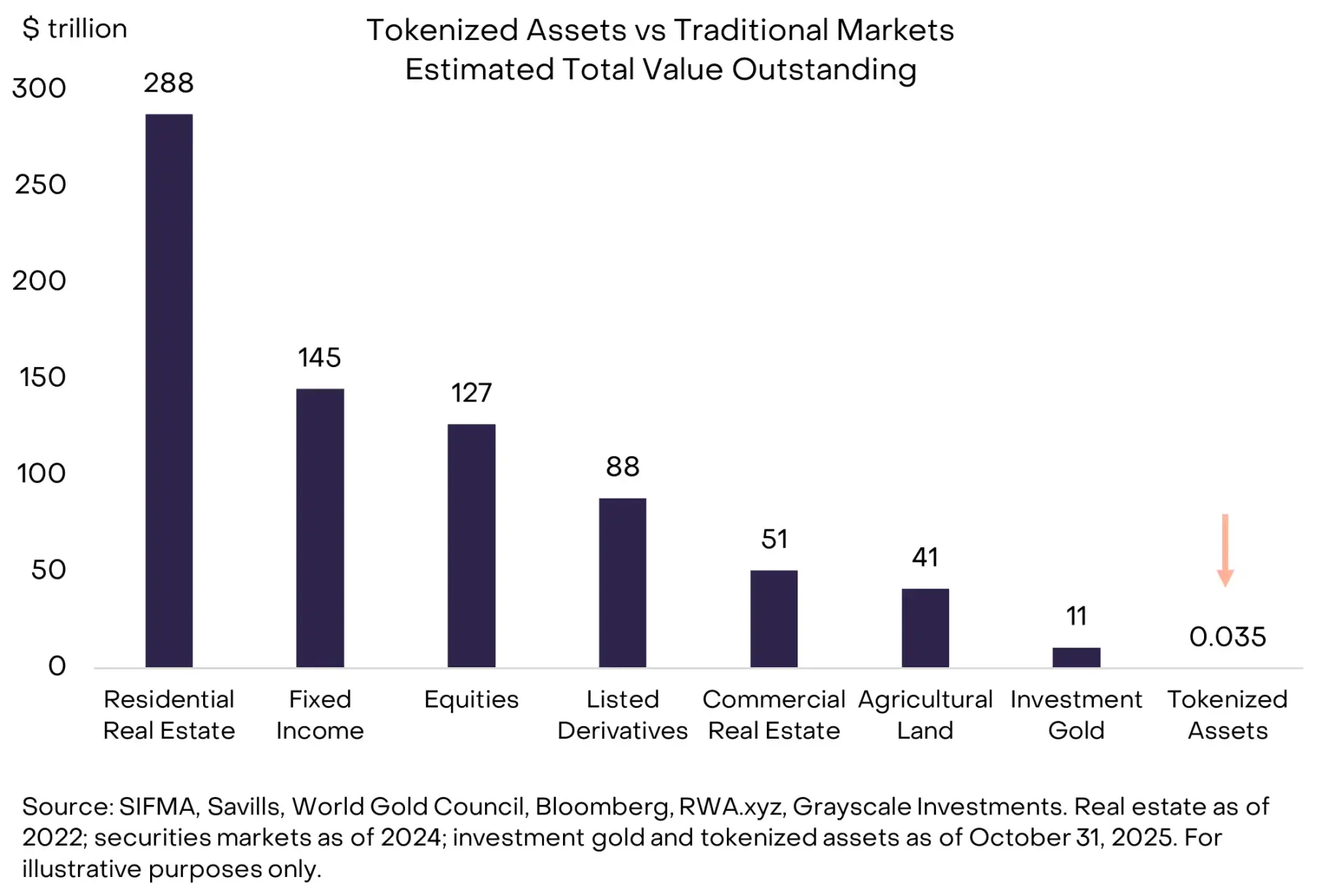

Currently, tokenized assets represent a minuscule fraction of the global financial landscape, accounting for only about 0.01% of the total market capitalization of global stocks and bonds. Grayscale anticipates that as blockchain technology matures and regulatory clarity improves, asset tokenization will experience exponential growth in the coming years.

We believe a roughly 1,000-fold expansion in tokenized asset scale by 2030 is not unimaginable. This growth is poised to generate substantial value for the blockchain networks that process tokenized asset transactions and for the various supporting applications built around them.

Leading public chains in the tokenization space currently include Ethereum (ETH), BNB Chain (BNB), and Solana (SOL), though this landscape may evolve. Among supporting applications, Chainlink (LINK) stands out with its unique and comprehensive software stack, offering a distinct competitive advantage.

Theme 5: Mainstream Blockchain Adoption Increases Demand for Privacy Solutions

Relevant Crypto Assets: ZEC, AZTEC, RAIL

Privacy is a fundamental pillar of any functional financial system. Most individuals expect their income, tax information, asset holdings, and spending habits to remain confidential, not publicly displayed on a ledger. However, most current blockchains are designed with transparency as a default. For public blockchains to achieve deeper integration into the financial system, they must be complemented by mature and robust privacy infrastructure—a need that becomes increasingly evident as regulation pushes for convergence between blockchain and traditional finance.

With investors increasingly prioritizing privacy, Zcash (ZEC) stands as a potential beneficiary. It is a decentralized digital currency, structurally similar to Bitcoin but with built-in privacy features, which saw significant appreciation in Q4 2025. Other notable projects include Aztec (a privacy-focused Ethereum Layer 2 network) and Railgun (privacy middleware for DeFi).

Furthermore, we may observe mainstream smart contract platforms more widely adopting “confidential transaction” mechanisms, such as Ethereum’s ERC-7984 standard and Solana’s Confidential Transfers token extension. The advancement of privacy tools may also necessitate simultaneous upgrades in identity verification and compliance infrastructure within the DeFi sector.

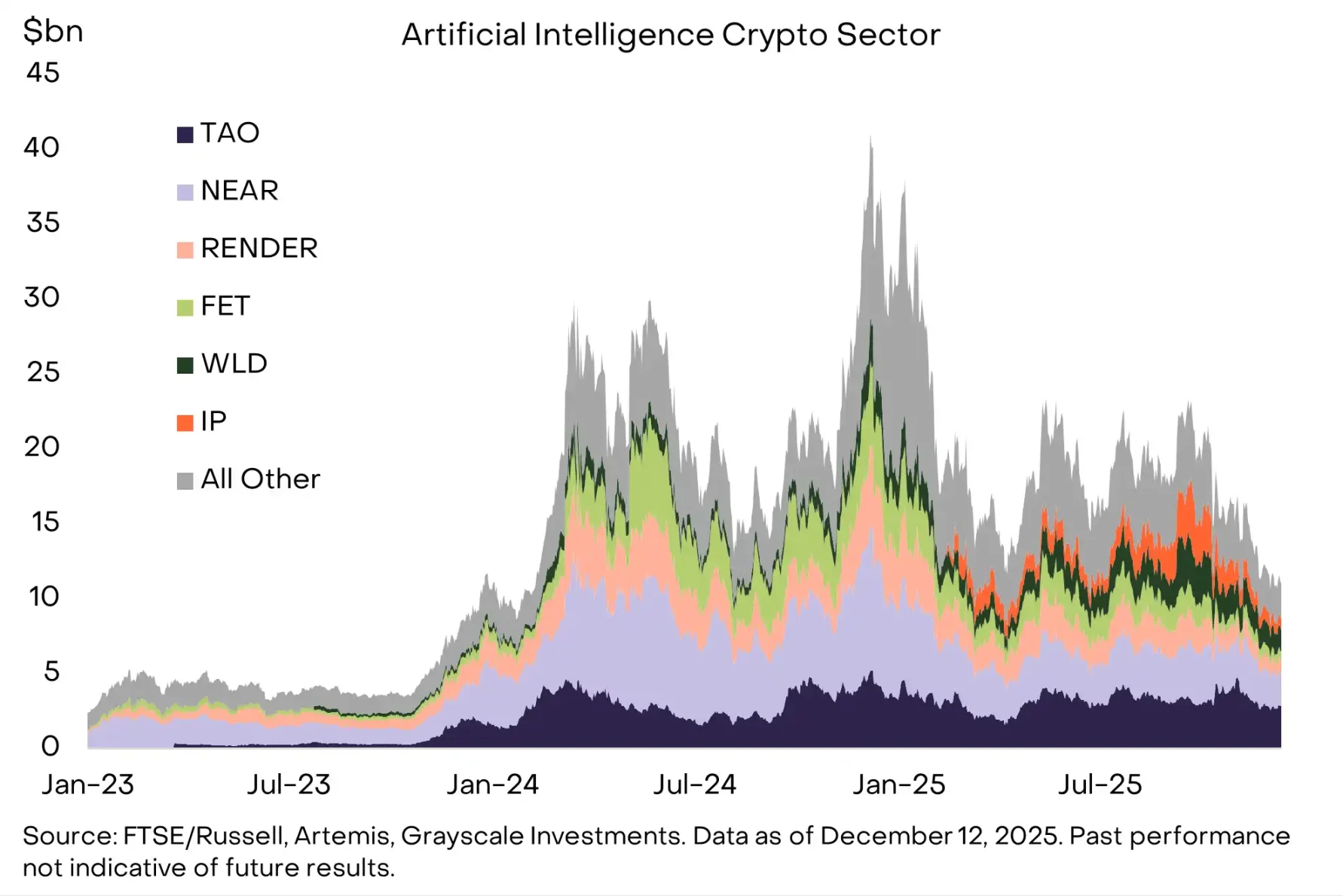

Theme 6: AI Centralization Spurs Demand for Blockchain-Based Solutions

Relevant Crypto Assets: TAO, IP, NEAR, WORLD

The inherent synergy between crypto technology and artificial intelligence has never been more apparent. As AI systems increasingly centralize within a few dominant companies, concerns regarding trust, bias, and ownership are mounting. Crypto technology, however, offers foundational primitives that directly address these risks.

For instance, decentralized AI development platforms like Bittensor aim to mitigate reliance on centralized AI; World’s verifiable “Proof of Personhood” seeks to distinguish real humans from intelligent agents amidst a flood of synthetic activity; and networks such as Story Protocol provide transparent on-chain traceability in an era where the provenance of digital content is increasingly obscure. Concurrently, tools like X402, an open layer for zero-fee stablecoin payments on Base and Solana, provide the low-cost, instant micropayment capabilities essential for economic interactions between agents or machines and humans.

Collectively, these elements form the nascent infrastructure of what is termed the “agent economy,” where identity, compute power, data, and payments must be verifiable, programmable, and censorship-resistant. While this ecosystem is still in its early, uneven stages of development, the intersection of crypto and AI represents one of the industry’s most imaginative long-term application frontiers. As AI becomes more decentralized, autonomous, and economically capable, protocols building genuine infrastructure in this space are poised to benefit significantly.

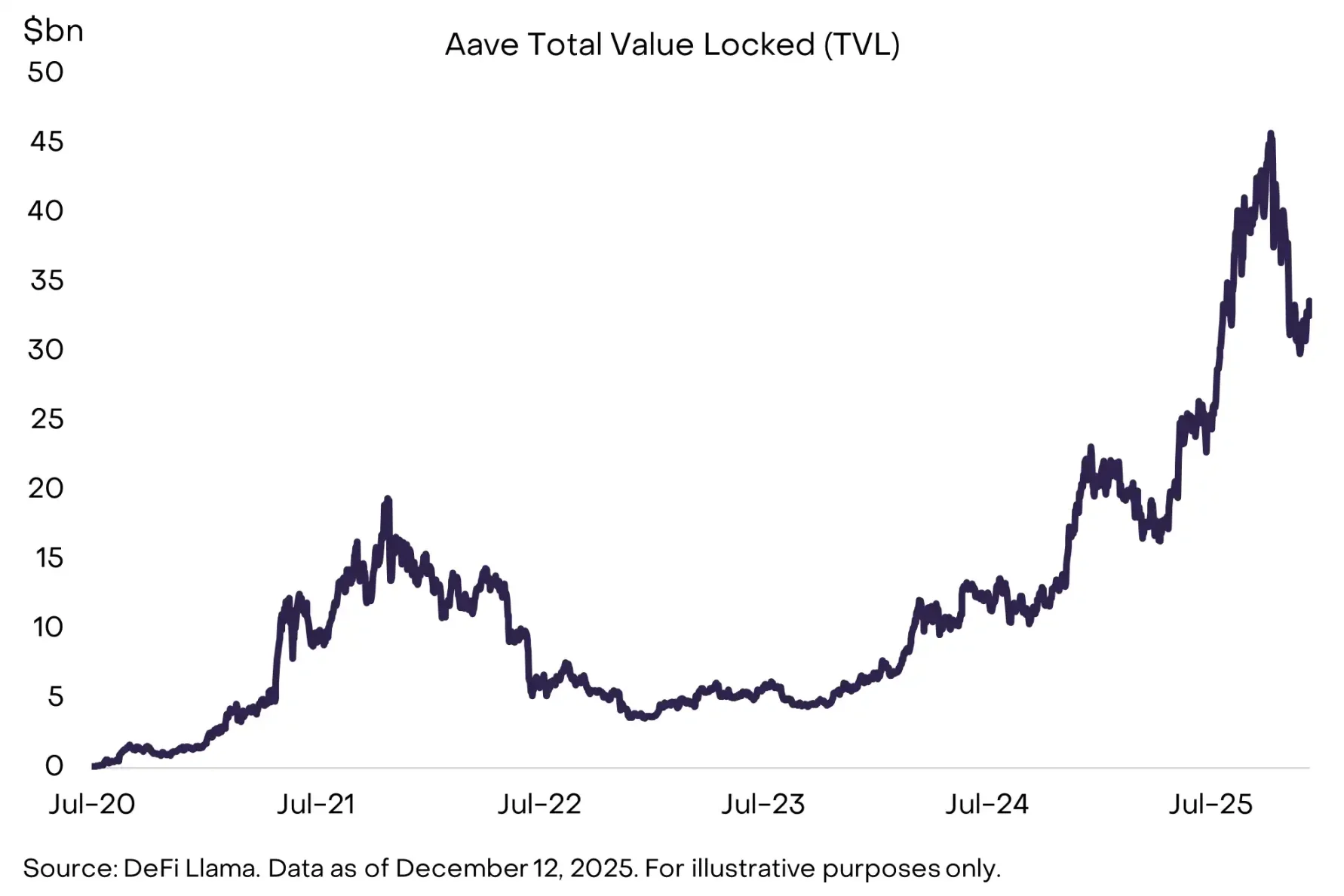

Theme 7: DeFi Accelerates, Led by Lending Protocols

Relevant Crypto Assets: AAVE, MORPHO, MAPLE, KMNO, UNI, AERO, RAY, JUP, HYPE, LINK

DeFi applications experienced significant acceleration in 2025, driven by both technological maturity and an improved regulatory environment. While stablecoins and tokenized assets represent prominent successes, the DeFi lending sector also saw substantial expansion, led by protocols such as Aave, Morpho, and Maple Finance.

Simultaneously, decentralized perpetual futures exchanges, such as Hyperliquid, have steadily approached or even surpassed some large centralized derivatives exchanges in metrics like open interest and daily trading volume. Looking ahead, with enhanced liquidity, increased cross-protocol interoperability, and stronger connections to real-world price systems, DeFi is progressively becoming a credible alternative for users seeking to conduct financial activities directly on-chain.

We anticipate increased collaboration between DeFi protocols and traditional fintech companies, leveraging the latter’s established infrastructure and user bases. This process will continue to benefit core DeFi protocols—including lending platforms (e.g., AAVE), decentralized exchanges (e.g., UNI, HYPE), and related infrastructure protocols (e.g., LINK)—as well as the public chain networks that host the majority of DeFi activity (e.g., ETH, SOL, BASE).

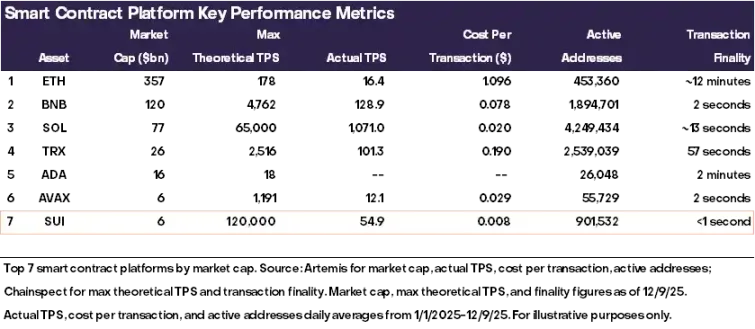

Theme 8: Mainstream Adoption Necessitates Next-Generation Infrastructure Upgrade

Relevant Crypto Assets: SUI, MON, NEAR, MEGA

A new generation of blockchains is continuously pushing technological boundaries. However, some investors argue that additional block space is unnecessary, as existing public chains have not yet reached full demand saturation. Solana once epitomized this skepticism: initially viewed as “excess block space” due to its high performance but limited usage, it later became one of the industry’s most successful examples following a wave of application adoption.

While not all high-performance public chains will replicate Solana’s trajectory, we believe a select few have breakthrough potential. Exceptional technology alone doesn’t guarantee adoption, but the architecture of these next-generation networks offers unique advantages for emerging applications such as AI micropayments, real-time gaming loops, high-frequency on-chain trading, and intent-based systems.

Within this cohort, we expect Sui to stand out, driven by its clear technological leadership and highly integrated development strategy. Other noteworthy projects include Monad (parallelized EVM architecture), MegaETH (an ultra-fast Ethereum Layer 2 network), and Near (an AI-focused blockchain making strides with its Intents product).

Theme 9: Increased Focus on Sustainable Revenue Models

Relevant Crypto Assets: SOL, ETH, BNB, HYPE, PUMP, TRX

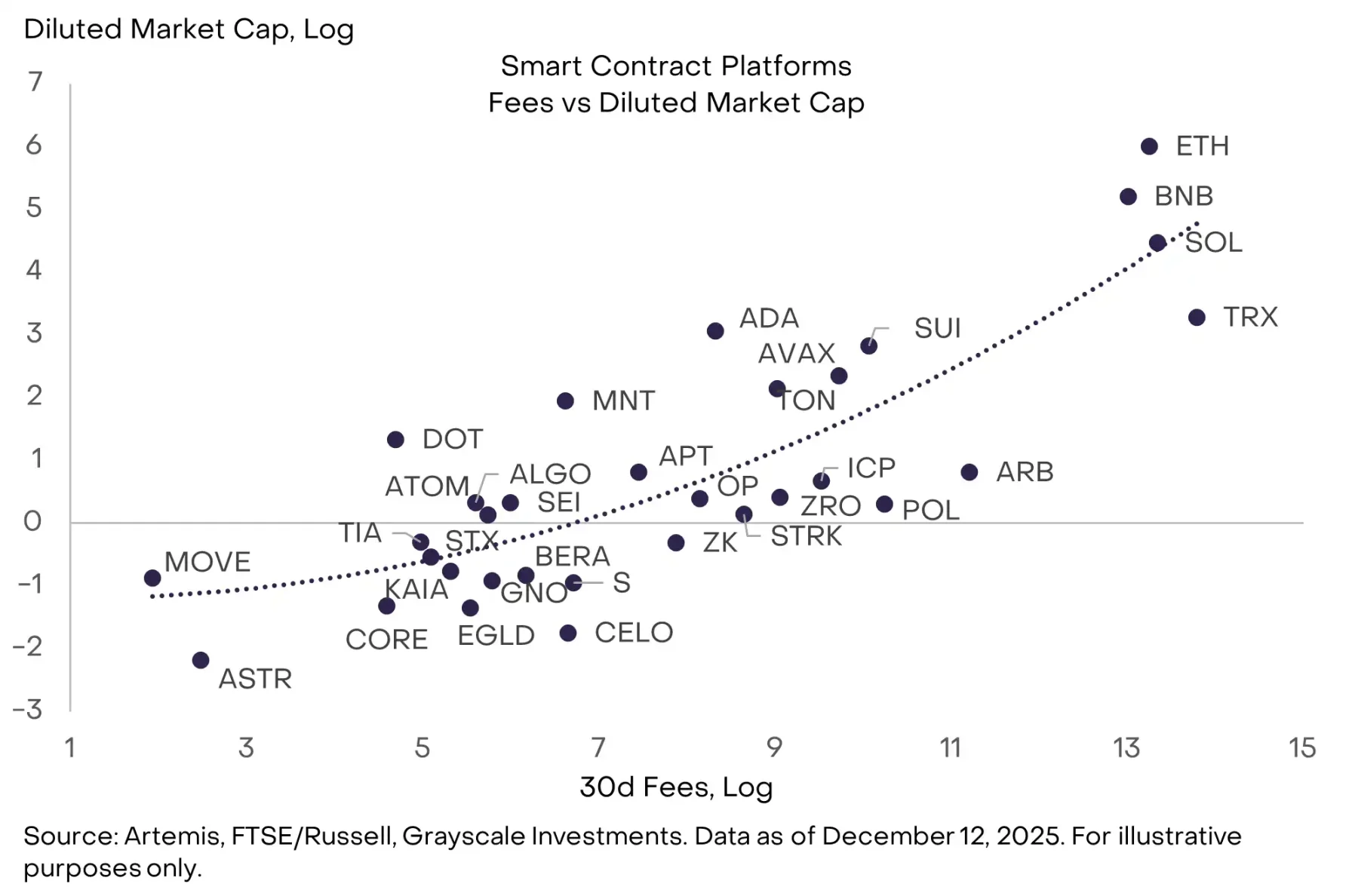

While blockchains are not traditional corporations, they possess quantifiable fundamental metrics: user count, transaction volume, fees, total value locked (TVL), developer ecosystem size, and application diversity. Among these, Grayscale considers transaction fees the most valuable single fundamental indicator. They are the most resistant to artificial manipulation, offer high comparability across different blockchains, and exhibit the strongest empirical fit.

From a traditional corporate finance perspective, transaction fees are analogous to “revenue.” For blockchain applications, it’s crucial to differentiate between protocol-layer fees/revenue and “supply-side” fees/revenue. As institutional investors systematically allocate to crypto assets, we anticipate a heightened focus on blockchains and applications (excluding Bitcoin) demonstrating high or clearly growing fee revenue levels.

Currently, smart contract platforms with relatively high fee revenues include TRX, SOL, ETH, and BNB. In the application layer, projects like HYPE and PUMP exhibit strong revenue performance.

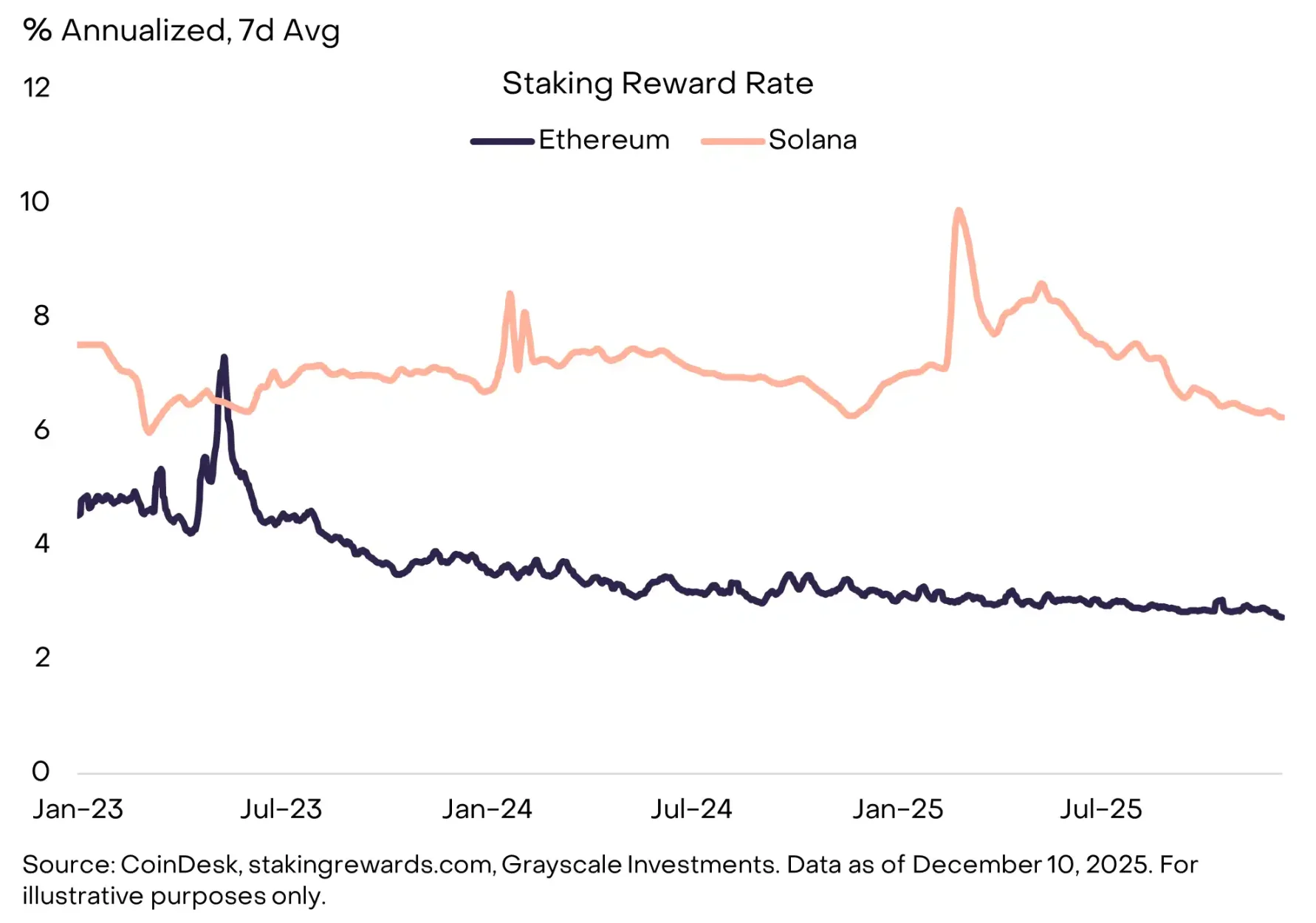

Theme 10: Investors Will “Default” to Staking for Yield

Relevant Crypto Assets: LDO, JTO

US policymakers implemented two critical adjustments to staking mechanisms in 2025, significantly expanding participation opportunities for token holders:

- The US Securities and Exchange Commission (SEC) explicitly clarified that liquid staking activities do not constitute securities transactions.

- The US Internal Revenue Service (IRS) and Treasury Department confirmed that investment trusts and Exchange Traded Products (ETPs) are permitted to stake digital assets.

Regulatory clarity surrounding liquid staking services is expected to directly benefit protocols like Lido and Jito—the leading liquid staking protocols by TVL in the Ethereum and Solana ecosystems, respectively. More broadly, the ability for crypto ETPs to participate in staking will likely establish “staking as the default holding method” for Proof-of-Stake (PoS) token investments. This will drive up overall staking ratios, potentially exerting some downward pressure on staking yields.

In an environment of widespread staking adoption, custodial staking via ETPs will offer investors a convenient way to earn staking yields, while on-chain, non-custodial liquid staking will retain unique advantages in composability within the DeFi ecosystem. We anticipate this dual-track structure will persist for a considerable period.

Red Herrings for 2026

While the aforementioned investment themes are poised to significantly impact the crypto market in 2026, two topics, despite generating considerable discussion, are unlikely to be substantial market drivers next year: the potential threat of quantum computing to cryptography and the evolution of Digital Asset Treasury Companies (DATs). Much will be written about these issues, but in our view, they will not be core variables determining the market’s trajectory.

Quantum Computing

Should quantum computing technology continue its advancements, most blockchains will eventually require upgrades to their cryptographic systems. Theoretically, sufficiently powerful quantum computers could derive private keys from public keys, enabling unauthorized digital signatures and asset transfers. Consequently, Bitcoin, most blockchains, and indeed the entire cryptography-dependent modern economy will need to transition to post-quantum cryptographic tools in the long term. However, experts generally agree that quantum computers capable of breaking Bitcoin’s cryptography are unlikely to emerge before 2030 at the earliest. We anticipate an acceleration of research and community preparedness around quantum risks in 2026, but this theme is unlikely to have a material short-term impact on prices.

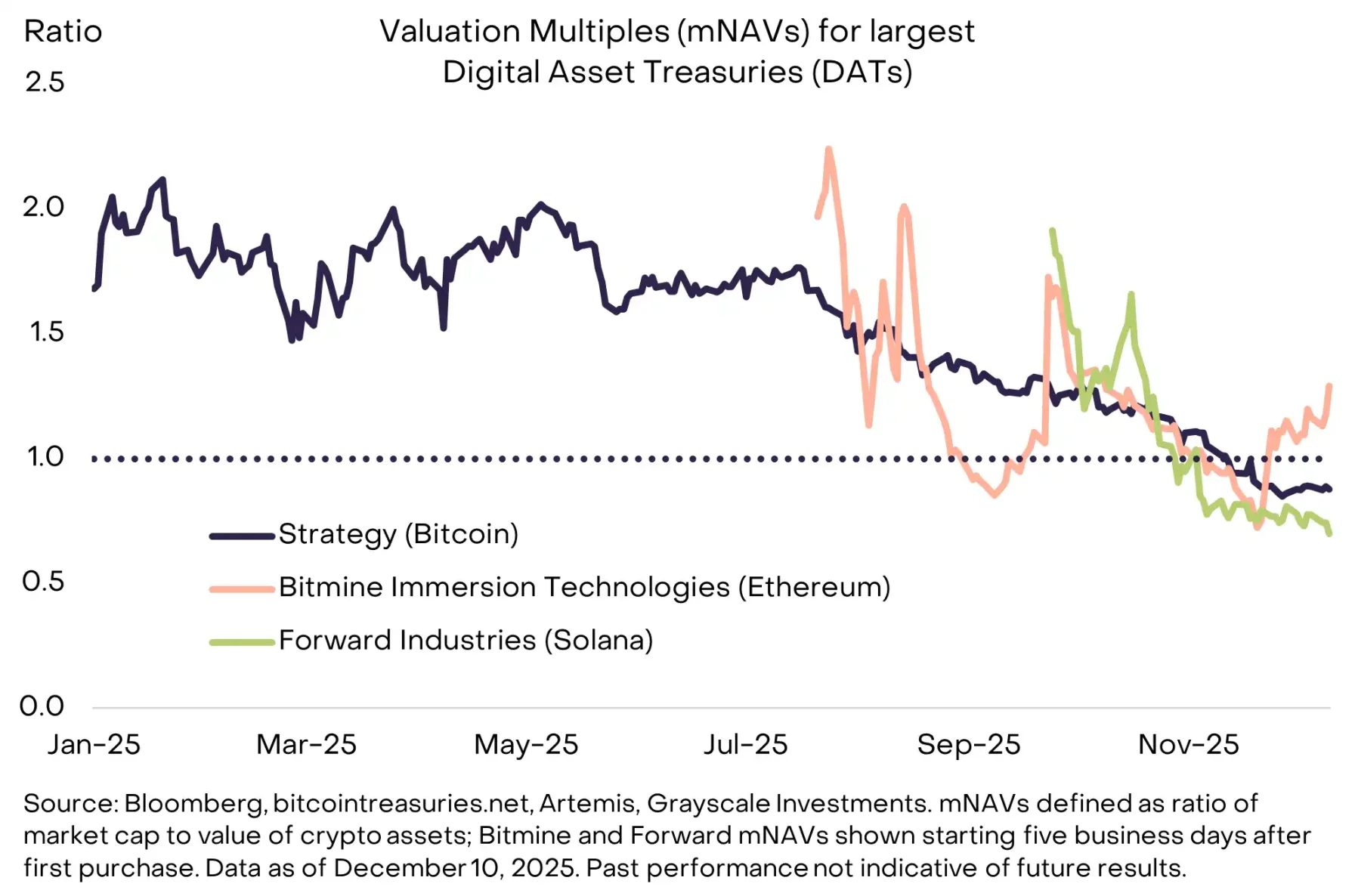

Digital Asset Treasury Companies (DATs)

The strategy of incorporating digital assets onto corporate balance sheets, pioneered by Michael Saylor, inspired dozens of imitators in 2025. By our estimates, DATs currently hold 3.7% of Bitcoin’s total supply, 4.6% of Ethereum’s, and 2.5% of Solana’s. However, since their peak in mid-2025, market demand for these instruments has cooled, with the largest DAT’s mNAV (market cap/net asset value) having reverted to near 1.0.

Crucially, most DATs have not employed excessive leverage (or any leverage at all), making forced asset sales during market downturns unlikely. The largest DAT by market cap, Strategy, recently established a USD reserve fund to ensure continued preferred stock dividend payments even if Bitcoin prices decline. We expect most DATs to behave more like closed-end funds: trading within a fluctuating range around net asset value, occasionally at a premium or discount, but rarely actively liquidating assets.

Overall, these instruments are likely to remain a long-term component of the crypto investment landscape. However, we do not foresee them becoming a major source of new token demand or significant selling pressure in 2026.

Conclusion

Grayscale maintains a positive outlook for digital assets in 2026, driven by the powerful synergy of sustained macro demand for alternative stores of value and continuous improvements in regulatory clarity. The year’s defining themes will likely be the deepening integration between blockchain finance and traditional finance, coupled with a steady influx of institutional capital. Tokens that achieve institutional adoption will typically exhibit clear application scenarios, sustainable revenue models, and access to compliant trading venues and application ecosystems. Investors can also expect the range of crypto assets investable via ETPs to expand further, with staking mechanisms becoming a default feature where conditions permit.

Concurrently, the twin forces of regulatory clarity and institutionalization will raise the bar for mainstream success. For instance, crypto projects seeking listing on regulated exchanges may face new registration and disclosure requirements. Institutional investors are also more likely to bypass crypto assets lacking clear use cases, even if those assets currently command relatively high market capitalizations. The GENIUS Act, for example, legally differentiates regulated payment stablecoins (which enjoy specific rights and obligations under US law) from other stablecoins (which do not). Similarly, we anticipate that the institutional era of crypto assets will further widen the gap between assets that can access compliant channels and institutional capital and those that cannot.

The crypto industry is entering an entirely new phase, and not every token will successfully navigate this transition from the old era to the new.