Compiled & Edited by: TechFlow

Key Insights from Tom Lee

Tom Lee, Co-founder and Head of Research at Fundstrat Global Advisors, also serves as Chairman of the Ethereum treasury company Bitmine Immersion. He is the Chief Investment Officer of Fundstrat Capital, which oversees the rapidly expanding Granny Shots ETF series, currently managing $4.7 billion in assets.

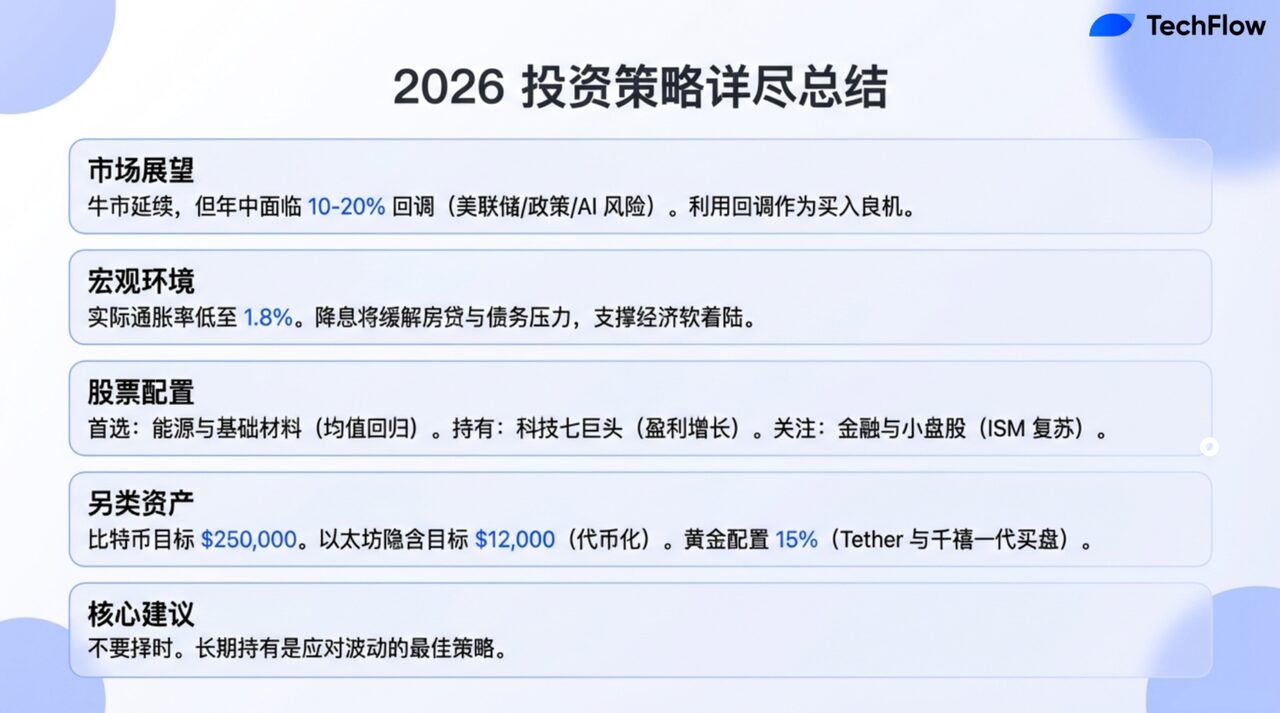

In a recent interview, Lee shared his compelling market outlook. He believes the decade-long bull market, which commenced in 2022, is still in its nascent stages. Despite anticipating a significant market correction this year—one that might feel reminiscent of a bear market—he projects a robust rebound in the stock market by 2026. Lee highlighted three pivotal shifts investors must navigate this year: new Federal Reserve policies, a more interventionist White House, and the ongoing re-evaluation of the artificial intelligence (AI) boom. While he remains optimistic about the “Magnificent Seven” U.S. stocks, he suggests that cyclical industries, energy, basic materials, financials, and small-cap stocks could offer more compelling investment opportunities.

The discussion also delved into gold, cryptocurrencies, and demographic trends. Lee views gold as currently undervalued, revealing that Tether might be one of the largest private buyers of gold today. He noted a generational shift, with millennials rediscovering gold’s value, while younger generations gravitate towards cryptocurrencies. Bitcoin, he asserts, remains “digital gold,” but Ethereum stands out as his top cryptocurrency pick. He analyzed how a deleveraging event last October caused cryptocurrencies to diverge from gold’s price trajectory. Lee predicts substantial gains for Bitcoin and Ethereum as banks and asset managers accelerate their adoption of blockchain technology.

Furthermore, Lee discussed Bitmine’s $200 million investment in MrBeast’s Beast Industries. He regards MrBeast as one of the most influential media assets of this generation, envisioning financial education and Ethereum as core components of future products, potentially reaching billions of users globally.

Highlights of Tom Lee’s Views

- Bitcoin is projected to reach a new all-time high of $250,000 this year.

- Tether has emerged as the largest private gold buyer.

- The upcoming market correction could be around 10%, but even a 10% pullback will feel like a bear market.

- Every market correction presents an excellent buying opportunity.

- Our top sectors for this year are energy and basic materials.

- The banking sector has begun embracing the efficiency gains offered by blockchain.

- Silver and copper are expected to perform well this year. Copper, as an industrial metal, correlates closely with the ISM Index; its rise should boost basic materials stocks.

- Looking back at 2026, it will be seen as a continuation of the bull market that began in 2022.

- Several critical market shifts are underway: new Federal Reserve leadership, a more interventionist White House, and the market’s ongoing attempt to value AI. These three factors combined could trigger a “bear market-like” correction.

- Last year, investors often overreacted to escalating tariff negotiations and uncertainties. This year, market responses are expected to be more rational, with reactions potentially halved.

- Federal Reserve rate cuts could significantly alleviate economic pressure for many Americans.

- Once the Fed chair changes or a few more rate cuts occur this year, it will be beneficial for the stock market.

- Oil prices might be soft or volatile in the short term, but the growth of data centers and the transition from alternative energy sources will drive future oil price increases, making energy stocks strong performers.

- Bitcoin is digital gold, but the demographics that believe in this theory do not overlap with traditional gold owners.

- The adoption curve for cryptocurrencies remains higher than for gold, as more people own gold than crypto.

- The most crucial advice I can offer investors is not to attempt market timing; true wealth is built by those who invest for the long term.

- Cryptocurrencies are being embraced by the younger generation—it has become an integral part of their lives.

2026 Market Outlook: A Bull Market with Corrections

Wilfred Frost: Welcome to the Master Investor podcast. I’m Wilfred Frost, and today’s guest is the highly esteemed Tom Lee. Tom is the Co-founder and Head of Research at Fundstrat Global Advisors, Chairman of the Ethereum asset management company Bitmine Immersion, and manages the Granny Shots ETF—a fund focused on technology and innovation investments. It’s a privilege to have you with us in London.

As we begin 2026, Tom, I understand you have a precise forecast for the year: an initial market surge, followed by a substantial correction, and then a strong rebound towards year-end. Does this accurately reflect your 2026 market outlook?

Tom Lee:

I believe that when we reflect on 2026, it will be seen as a continuation of the bull market that began in 2022, characterized by even greater economic resilience. However, the market faces several significant transitions, two of which are particularly critical. First, there’s new leadership at the Federal Reserve. Markets typically test the policies of a new Fed chair, and this process of identification, confirmation, and market reaction could trigger a correction. Second, the White House’s policy stance is a factor. In 2025, White House policies significantly impacted tech consulting and healthcare. In 2026, more industries, sectors, and even nations could become policy targets. This shift introduces greater uncertainty, as evidenced by the recent rise in gold prices, reflecting market concerns about risk. These two factors combined could lead to a market pullback.

Wilfred Frost: You’ve mentioned two factors. Are there any other potential influences?

Tom Lee:

Yes, there’s a third factor: the market is still attempting to assess the true value of artificial intelligence (AI). While we view AI as a powerful market driver, many questions remain regarding its long-term potential, energy demands, and data center capacity. Until these questions become clearer, the market may need other strong supporting narratives, such as the recent rebound in the ISM Manufacturing Index and the potential recovery of the housing market as interest rates decline. These shifts also introduce uncertainty. Therefore, I believe these three factors, in combination, could lead to a “bear market-like” correction.

Wilfred Frost: What magnitude of correction do you anticipate? A 20% peak-to-trough adjustment, or something smaller?

Tom Lee:

It could be around 10%. But even a 10% pullback can feel like a bear market. It might also reach 15% or 20%, which could bring the market back to its starting point for the year after a strong beginning. While we’ve had a very strong start to the year, I expect the market to experience an intra-year decline at some point, though I’m confident that the year’s overall performance will be very strong.

Wilfred Frost: When we spoke last August, you suggested we were at or near the beginning of a 10-year bull market. Do you still hold that view? In other words, once the market experiences this correction, would you consider it an excellent buying opportunity?

Tom Lee:

I’ve always maintained that every market pullback presents an excellent buying opportunity. Last year, due to tariff concerns, the market fell on April 7th, which proved to be one of the best times to buy stocks in the past five years. Many stocks went on to hit new all-time highs and saw a very strong rebound. So, I believe if the market does correct as we anticipate this year, it will be a very good opportunity to buy.

Drivers of the Long-Term Bull Market

Wilfred Frost: Last August, you highlighted three long-term drivers for a new 10-year bull market: a surge in the working-age population, the younger generation inheriting substantial wealth, and the U.S. central role in innovation, particularly AI and blockchain. Do you still feel confident in these three factors?

Tom Lee:

Yes, in fact, I think these factors are even clearer now.

Firstly, the U.S. indeed boasts a favorable demographic trend, contrasting sharply with many countries experiencing a decline in their working-age populations.

Secondly, regarding wealth inheritance, there’s growing discussion that Gen Z, millennials, and Gen Alpha will inherit significant wealth over their lifetimes. While this phenomenon may exacerbate wealth inequality, it also means there will be some very wealthy younger generations, while others will gradually accumulate personal wealth through their own efforts.

Concerning artificial intelligence, the evidence of our progression towards super-intelligence is mounting. Advances are incredibly rapid, especially in robotics and the integration of robotics with other technologies, all of which will continue to bolster the U.S. advantage. As for blockchain, its impact extends beyond companies like BlackRock and Robinhood. For instance, Jamie Dimon (JPMorgan Chase CEO) recently stated publicly that he believes blockchain can indeed solve many problems in financial services. I think the banking sector has begun to embrace the efficiency gains that blockchain offers.

Wilfred Frost: You remain a firm believer in the long-term bull market, expecting a recovery after any pullback. How can we better predict when this initial pullback might occur? I recently heard you on CNBC mention that markets often peak on good news, which sounds counterintuitive. Do we have such “good news” now that might indicate a short-term market peak?

Tom Lee:

That’s a tough question to answer, but currently, some signs are based on experience. Our institutional clients aren’t showing overly optimistic market positioning right now. And until both public and institutional investors have adjusted to a point where good news no longer drives the market higher, I believe the stock market still has room to rise. This is why the strong performance in the first week of January is a positive signal, and it looks like we might end the month with positive returns, indicating strong early-year market performance.

Margin debt is an indicator we monitor. We track NYSE margin debt, which is currently at an all-time high, but its year-over-year growth is only 39%. Typically, to reach a local market peak, margin debt needs to see annual growth of 60%. So, there’s still potential for further acceleration in leverage, which could then signal a local market top.

Macro: Trade Wars and the Federal Reserve

Wilfred Frost: Let’s discuss some macro factors. First, trade. I recall you mentioned last year that the impact of trade wars wasn’t as bad as anticipated. However, this past weekend brought more tariff threats, this time involving Greenland and targeting the UK and EU. It seems the UK might compromise, while the EU could retaliate. Does this concern you in the short term?

Tom Lee:

There is concern, but not excessively so. I think last year, investors often overreacted to escalating tariff negotiations and uncertainties, leading to significant market declines. However, this year, market responses might be more rational, with reactions potentially halved. Still, uncertainties persist, such as how the Supreme Court will rule on tariff issues. If the ruling goes against Trump, it could weaken the U.S. negotiating position, potentially prompting the White House to take more extreme measures, which could spark greater uncertainty. However, I recently read some news suggesting the Supreme Court might support Trump’s policies. So, the ultimate outcome remains uncertain.

Wilfred Frost: Another crucial macro issue is the Federal Reserve. When we spoke last August, your view was that Fed rate cuts are good for the market, but questioning the Fed’s independence is bad. However, I felt you didn’t particularly emphasize the severity of intervention back then. How do you view this issue today?

Tom Lee:

I think the situation remains similar. The Federal Reserve does face some implicit threats, including investigations by the Department of Justice. However, I believe there are still voices within the White House emphasizing not to completely undermine the Fed’s independence. Market history tells us that the Fed remains one of the most important institutions globally, and undermining its credibility and independence could lead to immense uncertainty.

We also know that current Fed Chair Powell’s term ends this year. So, the situation is somewhat of a “wait and see” as we anticipate a new Fed chair. Once a new chair is in place, I believe the White House might be satisfied. As for the next Fed chair, predictions are constantly shifting; it now appears Hasset’s chances are diminishing, while WH and Rick Reer’s possibilities are rising. Furthermore, there’s a general expectation that this year’s rate cuts might be more substantial than what economic data currently suggests.

Wilfred Frost: So, once the Fed chair changes or a few more rate cuts occur this year, will this ultimately be good for the stock market?

Tom Lee:

Yes, I believe it will be good for the stock market. Since 2022, inflation has been a central market concern, partly because the Fed has been battling inflation and aiming to maintain its credibility through tightening policies. However, based on economic data, I believe the actual inflation level is lower than the reported figures. For example, “true inflation” shows 1.8%, and median inflation is also 1.8%. The primary factor keeping inflation elevated is housing costs, but home prices are actually declining. And the calculation of housing costs in the Consumer Price Index (CPI) has a lag. Therefore, I believe the Fed has room to cut rates. If housing affordability becomes an issue, we need to address mortgage rates, and rate cuts can help alleviate this problem. Additionally, burdens like consumer installment debt can also be reduced through rate cuts. So, I believe Fed rate cuts could significantly alleviate economic pressure for many Americans.

Sector Allocation: Energy, Raw Materials, and Technology

Wilfred Frost: Let’s discuss how investors should approach sector allocation. Have the “Magnificent Seven” or “Mag 10” stocks become overvalued? Are they no longer suitable investment choices for 2026?

Tom Lee:

We still favor the “Magnificent Seven” because we are confident in their earnings growth. As long as these companies continue to grow, their performance should outperform the broader market. However, our top sectors for this year are energy and basic materials. We listed these two sectors as our preferred investment areas in early December last year. This is partly due to the investment logic of mean reversion—energy and basic materials have performed very poorly over the past five years, and historical data from the last 75 years indicates that such significant downturns often signal a turning point. Additionally, current geopolitical factors are favorable for both sectors.

I believe the ISM Index may break above 50 again this year, coupled with Fed rate cuts, which implies that industrial sectors, financials, and small-cap stocks could perform well. So, while we like the “Magnificent Seven,” cyclical sectors might be more interesting investment choices this year.

Wilfred Frost: Let’s start with the energy sector. I recall you’ve said you’re not optimistic about short-term oil prices, but you are bullish on energy stocks.

Tom Lee:

That’s correct. I understand that oil prices and energy stock performance are not always correlated. This is partly because energy stock prices reflect expectations for future oil prices. I believe short-term oil prices might be soft or volatile, but factors like the growth of data centers and the shift away from alternative energy sources will drive future oil price increases, allowing energy stocks to perform exceptionally well.

Wilfred Frost: Regarding the basic materials sector, particularly metals, their underlying commodity prices have seen incredible surges. Perhaps we can discuss this in conjunction with cryptocurrencies later.

If metal prices correct, will these stocks underperform? Does your forecast rely on stable prices for metals like gold, silver, and copper?

Tom Lee:

Yes, if gold, silver, and copper prices experience negative growth this year, then the investment thesis for basic materials might not hold. However, we believe that while gold has already seen significant gains, silver and copper could perform well this year. Copper, as an industrial metal, is closely correlated with the ISM Index. If copper prices rise, I believe it will drive the performance of basic materials stocks.

Wilfred Frost: The financial sector was an area you were very bullish on last August, and that prediction proved very accurate. These stocks have performed incredibly strongly; looking at their charts now, it’s almost hard to believe their gains. Are you still bullish on these stocks? Their price-to-book (P/B) ratios are no longer cheap.

Tom Lee:

Yes, they are indeed no longer cheap, but I believe the business models of these companies are being redefined in a positive way. Banks are investing heavily in technology and artificial intelligence (AI), making them major beneficiaries in the age of super-intelligence. Banks’ largest expense is employee compensation, and I believe in the future, banks can reduce their reliance on employees, which will boost their profit margins while reducing earnings volatility. I think banks will be revalued, more akin to tech companies. When I started researching banks in the 90s, they were typically valued at 1x P/B or 10x P/E, but now I believe they should command a market premium valuation.

Wilfred Frost: I’d like to delve deeper into tech stocks and AI-related stocks. You remain bullish on this sector, and your predictions over the past 15 years have been very accurate, but you mentioned that only 10% of AI stocks will be good investments over the next decade, which surprised me. Yet, you’re still optimistic about the field, correct?

Tom Lee:

Yes, I think this is a common phenomenon in any rapidly growing sector. For instance, looking back at the internet industry, if we consider the stock pool from 2000, 25 years ago, only 2% of companies ultimately survived. However, these 2% generated returns that far exceeded the losses from the other 98%, and overall performance still significantly outpaced the S&P 500. So, I believe that in the AI sector, while over 90% of stocks might ultimately underperform, the successful investments will compensate for, or even surpass, the other losses.

Today, publicly listed companies are often in more mature, later stages, but this seems to be changing. I think this is the first time we’re seeing more companies interested in going public, not just through IPOs, but also SPACs (Special Purpose Acquisition Companies). Furthermore, in alternative investment areas like venture capital, private equity, and private credit, investors (Limited Partners, LPs) haven’t received many distributions. Therefore, capital is shifting from alternative investments to public markets, driving more companies to go public. However, over the past 12 months, I’ve seen many publicly listed companies perform very strongly, so I believe there are still many opportunities in the market.

Wilfred Frost: Regarding hyperscale companies and mega-cap stocks, their valuations are quite interesting. In most cases, their valuations are justified due to their high growth rates. I was struck by a point you made in another podcast: that these companies might gradually evolve into something akin to consumer product companies, thereby earning premium valuations. This idea made me wonder if Warren Buffett noticed this earlier than us, as with Apple. Is this your view on these mega-cap companies? For example, even if Nvidia’s growth slows, its valuation might still remain stable?

Tom Lee:

Yes, listeners can recall the example of Apple. Since its IPO in the 80s, Apple analysts consistently argued it was a hardware company. For years, they believed Apple’s valuation shouldn’t exceed 10 times earnings. However, Apple gradually built a complete services ecosystem and user retention model, proving it was more than just a hardware company. I remember meeting institutional investors between 2015 and 2017 who still insisted Apple was a hardware company, and today Apple’s valuation has completely transformed.

I think people are now viewing Nvidia in a similar way, seeing it as a cyclical hardware company, and thus grudgingly assigning it a 26x P/E valuation. In reality, Nvidia is a company with high visibility into future earnings, yet its valuation is only half that of Costco. I believe these stocks have significant room to further increase their valuations.

Wilfred Frost: If the macroeconomic outlook is worse than expected, and the market experiences the correction you predict—for example, the S&P 500 falling 20%—will these stocks, like consumer product companies, see smaller declines, or will they still be considered high-volatility growth companies that fall more than the market?

Tom Lee:

That’s a good question. In a market correction, crowded trades are usually the first to be affected. (TechFlow Note: Crowded trades typically refer to certain assets or stocks heavily held by a large number of investors. This situation can make these assets more sensitive to market fluctuations, especially during a correction. When market sentiment turns pessimistic, investors tend to accelerate their unwinding of positions, exacerbating price declines for these assets.) So, the “Magnificent Seven,” being large holdings, might take a hit. But on the other hand, when investors get nervous, they might gravitate towards the “Magnificent Seven.” Therefore, I believe non-U.S. stocks might see larger declines in a correction, as they significantly outperformed U.S. stocks last year. If trade tensions escalate or the global economic outlook becomes uncertain, the pullback in non-U.S. stocks could be more pronounced.

ETF Products: Granny Shots

Wilfred Frost: Let’s discuss some of your recent successes, such as “Granny Shots,” which, as I mentioned in the introduction, is your ETF or series of ETFs. When we spoke last August, these ETFs managed between $2 billion and $2.5 billion, and now that has grown to $4.5 billion.

Tom Lee:

Yes, the total size has reached $4.7 billion, distributed across three ETF products. Granny GRNY is the largest. Granny J, launched last November, is a small-cap and mid-cap ETF, currently with approximately $355 million in assets. And the Granny ETF for income-oriented investors, the income-generating version, paid its first dividend last December. This usually drives asset growth because there’s a clear yield. The target yield is around 10%, and this product currently has about $55 million in assets.

Wilfred Frost: For the coming year, is now a good time to invest in small-cap or income-oriented products rather than traditional ones?

Tom Lee:

I’m not one to try to “time the market.” For example, last January, Mark Newton warned of a potential correction, and the market’s decline far exceeded expectations, reaching 20%. But we still advised investors to remain fully invested, and they ultimately recovered their losses by July.

I believe small and mid-cap stocks have been underperforming for a long time, and even if a correction occurs, it won’t change the fact that they could be entering a five-to-six-year cycle of strong performance. So, I would still choose to hold these stocks.

Of course, if the overall market falls, the Granny ETFs won’t go up. So, I think any investor buying these ETFs needs to recognize that. But these ETFs select the strongest companies related to the most important themes, so they should perform better during a market pullback and potentially stronger during a market recovery.

Gold and Cryptocurrency

Wilfred Frost: Let’s talk about gold first, and then cryptocurrencies. Why do you think gold performed so exceptionally well last year?

Tom Lee:

I believe gold’s excellent performance has some obvious and some less obvious reasons. The obvious reasons include: First, the current investment environment is characterized by more political and geopolitical uncertainty. Wars globally, and a U.S. president who, while performing well economically, has exacerbated global trade uncertainty and fragmentation. Second, global central banks generally adopted accommodative policies, and the U.S. finally began its easing cycle, including ending quantitative tightening (QT), all of which supported gold.

As for the less obvious reasons, first, Tether (the largest stablecoin provider in the U.S.) has become the largest private gold buyer. To my knowledge, each stablecoin unit of Tether is fully collateralized by U.S. Treasuries, but they generate yield from these assets and use the excess returns to purchase gold. I believe since last July, Tether has been one of the largest net buyers.

Wilfred Frost: When you say “believe,” is this based on concrete data? How significant are Tether’s purchases compared to the large volumes bought by various central banks recently?

Tom Lee:

Yes, we have indeed seen relevant data. I can’t specify the exact scale, but I believe only one central bank’s purchases might have exceeded Tether’s. If you simply observe Tether’s USDT issuance and gold prices since last July, they are highly correlated.

Another factor is a study we conducted in 2018, which found that investment preferences often span generations. For example, baby boomers liked gold, Gen X favored hedge funds, and now millennials, entering their prime earning years, are rediscovering an interest in gold, much like their grandparents. This has also led to a resurgence in gold demand.

Wilfred Frost: I’m a millennial, and I also liked gold, though I sold too early. Regarding gold, do you view it as the ultimate currency, or just a commodity like copper and silver, other industrial metals? This would change our perspective on last year’s returns. For example, JPMorgan and Nvidia both performed well, with stock gains around 20%. But if we view gold as the ultimate currency, then those might actually be down. What’s your take?

Tom Lee:

Yes, we at Fundstrat don’t explicitly recommend gold, but I think we probably should. You’ve described it accurately; gold doesn’t make sense if viewed as an industrial commodity metal, because last year, gold’s total industrial and retail jewelry sales were roughly $120 billion, while its network value reached $30 trillion. So, its price-to-sales ratio is unreasonable. And we know gold isn’t scarce, as there are vast gold resources underground, and all gold is extraterrestrial material—for example, SpaceX might discover a gold-bearing asteroid in the future, leading to a sudden massive increase in gold supply.

However, gold has served as a store of value for centuries. As you said, it acts as an alternative to the dollar. Therefore, we should perhaps view gold as a dollar alternative, and from this perspective, all other assets have depreciated relative to gold.

Wilfred Frost: If viewed from that perspective, do you think more people will adopt this view? What would be the implications?

Tom Lee:

Yes, I think it means gold should have a place in investment portfolios. I see figures like Ray Dalio recommending gold at up to 10%, and in this podcast, you mentioned it could be 15%. Assuming it’s 15%, most people’s portfolios have almost zero gold. So, today gold is still an under-allocated asset.

Wilfred Frost: Why didn’t cryptocurrencies perform as well as gold last year?

Tom Lee:

I think the reason is related to timing. Cryptocurrencies performed comparably to gold until October 10th last year. For example, Bitcoin was up 36% at that point, and Ethereum was up 45%, even surpassing silver’s performance. But on October 10th, cryptocurrencies experienced the largest deleveraging event in history, even bigger than the FTX event in November 2022. After that, Bitcoin’s value fell by over 35%, and Ethereum dropped by nearly 50%.

The cryptocurrency market experienced deleveraging, which disrupted market liquidity providers, and liquidity providers in the crypto market are essentially the equivalent of central banks. Therefore, about half of the market’s liquidity providers were eliminated in the October 10th event. Until cryptocurrencies gain widespread support from mainstream institutional investors, such internal deleveraging events will continue to have a significant impact on the market.

Wilfred Frost: Does this mean you acknowledge that Bitcoin is not digital gold?

Tom Lee:

Bitcoin is digital gold, but the demographics that believe in this theory do not overlap with traditional gold owners. Therefore, the adoption curve for cryptocurrencies remains higher than for gold, because more people own gold than crypto. The future adoption path for cryptocurrencies might be very winding, and I believe 2026 will be a very important test. If Bitcoin can reach a new all-time high, then we can be certain that the deleveraging event is behind us.

Wilfred Frost: Your target price for Bitcoin this year is $250,000, correct? What’s driving that prediction?

Tom Lee:

Yes, we believe Bitcoin will reach a new all-time high this year. I think the driving force is the increasing utility of cryptocurrencies. For example, banks are starting to recognize the value of blockchain technology; settlement and final clearing operate very efficiently on the blockchain. Furthermore, crypto banks like Tether demonstrate that blockchain-native banking is actually superior to traditional banking. For example, Tether’s profits are projected to reach nearly $20 billion in 2026, making it one of the top five most profitable banks globally. In terms of valuation, it might be second only to JPMorgan, or even double that of Goldman Sachs or Morgan Stanley.

Tether has only 300 full-time employees, while JPMorgan has 300,000. By using blockchain, Tether’s profits are almost on par with, or even exceed, most banks. At the same time, its M1 money supply accounts for less than 1%, and its balance sheet is very small, yet it remains one of the most profitable banks globally.

Wilfred Frost: Let’s talk about Ethereum again. You told us last August that you were bullish on both Bitcoin and Ethereum, but you believed Ethereum would perform stronger in the long run. Why did Ethereum fall so sharply in the last quarter of last year?

Tom Lee:

Ethereum is the second-largest blockchain network, and I believe it will always be more volatile than Bitcoin until its scale approaches Bitcoin’s. The cryptocurrency market often views Ethereum’s price as a ratio to Bitcoin’s price. If we simply consider the ETH to BTC ratio as the price benchmark for the crypto world, then Ethereum’s price ratio relative to Bitcoin is still below 2021 levels. And compared to four years ago, Ethereum has become a superior blockchain.

For example, tokenization, including dollar tokenization, is a major trend that Wall Street is betting on. Larry Fink called it the biggest innovation since double-entry bookkeeping. Vlad Tenev of Robinhood wants to tokenize everything. We’ve already seen not just dollars (stablecoins), but also credit funds being tokenized. JPMorgan is launching money market funds on Ethereum, and BlackRock has already tokenized credit funds on Ethereum. So, Ethereum is actually the blockchain that Wall Street is beginning to adopt. If Ethereum’s price ratio returns to its 2021 highs, and Bitcoin reaches $250,000, then Ethereum’s price could reach around $12,000. Currently, Ethereum’s price is approximately $3,000.

Bitmine Immersion and Mr. Beast Investment

Wilfred Frost: Last week, you announced a $200 million investment in Beast Industries, the company behind Mr. Beast. Mr. Beast is currently one of the world’s largest YouTube influencers. As I understand it, his influence in the media landscape is astonishing, correct?

Tom Lee:

Yes, I think most people on Wall Street don’t realize Mr. Beast’s influence, for several reasons. First, this is a private company, so his influence needs to be assessed through media data. Second, he is iconic among Gen Z, Gen Alpha, and millennials.

He currently has over a billion followers. The only person with more followers than him across platforms like TikTok, Instagram, and Meta is Cristiano Ronaldo. His YouTube videos accumulate more monthly watch time than Disney and Netflix combined. Each episode of Mr. Beast’s YouTube videos is watched by over 250 million viewers monthly, and he releases two episodes a month, which is equivalent to two Super Bowl viewings every month. Additionally, his Beast Games on Amazon Prime is the platform’s number one show, with viewership almost exceeding all movies.

Wilfred Frost: These figures are truly astonishing, but why haven’t companies like Disney, Amazon Prime, Comcast, or Netflix invested in Beast Industries, and instead, an Ethereum financial company made the investment?

Tom Lee:

Well, they are very selective about who can enter their capital structure. Mr. Beast himself (Jimmy Donaldson) is the largest shareholder, and other shareholders include Chamath Palihapitiya of Social Capital, with Bitmine being the largest corporate investor on their balance sheet. As you can imagine, many companies wanted to invest in Beast Industries, and we were fortunate to be invited to participate in their capital structure.

Wilfred Frost: At Bitmine’s annual shareholder meeting last week, you mentioned that Beast Industries would be launching financial products or services. Is this plan confirmed? Will you be involved?

Tom Lee:

Yes, CEO Jeff Henbold has mentioned future plans for Beast Financial Services. I believe Beast Industries might disclose more details in the coming weeks. They are indeed very clever and have productized Mr. Beast’s brand in multiple ways, such as launching Feastables chocolates, healthy lunches, beverages, and collaborations with other creators. So, for a business with a billion followers, further productization is a natural progression.

Wilfred Frost: Do you think this is a good thing for Ethereum? Is it possible that Mr. Beast, with his billion followers, could promote Ethereum in the future?

Tom Lee:

I think it’s very possible. Today, there’s a huge gap in financial literacy globally, especially among young people, because schools don’t really teach it. Financial literacy is extremely important, as we know many baby boomers and Gen X are under-saved for retirement, and Social Security cannot be fully relied upon. Therefore, financial education is one of the biggest gaps in current society.

Mr. Beast could very well become a leader in promoting financial education, which would bring immense benefits to society. This is one of the reasons we are interested in Beast Industries, as our corporate and social values align very closely with theirs. Mr. Beast represents kindness and integrity.

As for the future of finance, banks have now clearly stated that blockchain is the direction of financial development. For example, JPMorgan wants to build businesses on blockchain, and Jamie Dimon has said that blockchain is a better way to build banks. And today, the place where banks choose to build smart contracts is Ethereum. Therefore, if financial education is to be delivered to the masses, then Ethereum should have a place in it.

Wilfred Frost: Final question, I still feel that for a financial management company, such an investment seems somewhat tangential to its core business. You previously mentioned similar “moonshot investments” like Orbs. Does this mean you acknowledge this is a high-risk investment? Or do you believe it’s actually a strategic investment?

Tom Lee:

I understand that for those unfamiliar with our investment logic, this might appear entirely high-risk. But it actually makes sense. From its inception, Bitmine has clearly stated that approximately 5% of its balance sheet would be allocated to “moonshot investments.” With today’s asset size, this amounts to roughly $700 million in investment capacity, and currently, we’ve deployed about $220 million into these initiatives.

I believe Beast Industries is a very promising investment because it gives us exposure to the world’s largest content creator, potentially the “Mr. Beast” of our generation. He is unprecedented and may not be surpassed by anyone for a very long time. As a financial management company, our goal is not only to strengthen the Ethereum ecosystem but also to ensure its future sustainability. By establishing potential organic collaborations with Mr. Beast, I believe this will further solidify Ethereum’s future. Therefore, I view this as a very sound strategic move.

Final Advice for Investors

Wilfred Frost: Two final questions. First, what is your most important advice for stock market investors this year?

Tom Lee:

Yes, I believe the most important advice I can give investors is not to try to time the market, as that will become your enemy in future performance. Many investors always hope to buy at the market’s lowest point and sell at its highest. But historically, whether in stock markets or cryptocurrency markets, the people who truly make money are those who invest for the long term. Although I warn that 2026 might bring a lot of volatility, investors should view market pullbacks as buying opportunities, not exit opportunities. Too many people sell due to emotion and then miss the chance to buy back in, thereby losing the compounding benefits of their investments. I think that’s a very important distinction.

Wilfred Frost: My second question is, what is your long-term advice for cryptocurrency investors? I believe this might be related to the point you just made, but how do you think they should invest?

Tom Lee:

Yes, I believe many listeners remain skeptical of cryptocurrencies, or haven’t engaged with them at all, perhaps feeling they can’t truly understand them. We need to recognize that cryptocurrencies are being embraced by the younger generation—it has become an integral part of their lives because they are digital natives. In the future, the lines between services and money will blur. This is no different from 1995, when Bill Gates spoke about the internet on “The David Letterman Show.” At that time, David Letterman expressed extreme skepticism about the internet concept because he belonged to a generation that couldn’t easily grasp it. If Bill Gates had explained the future of the internet to a 20-year-old, that young person would have immediately understood, and today cryptocurrencies are experiencing a similar situation.

Wilfred Frost: So, how do you think people should invest in cryptocurrencies? You recommend Bitmine, but should they hold a basket of cryptocurrencies? Or should they invest in treasury companies? Or allocate Bitcoin and Ethereum in a 2:1 ratio?

Tom Lee:

I think a two-pronged strategy can be adopted. First, there’s a theory called the “Lindy Effect,” and I advise only buying cryptocurrencies that have existed for a longer period, such as Bitcoin and Ethereum. Second, I believe cryptocurrencies may become a “settlement layer” in the future, even if it’s invisible. Bitmine not only acts as a settlement layer for the industry; through the investments we make, we are actually becoming a financial services company. Therefore, investing in Bitmine is not just investing in Ethereum; you are also investing in a company that is driving the future of finance.

(The above content is an excerpt and reprint authorized by our partner PANews, Original Link | Source: TechFlow)

Disclaimer: This article is for market information purposes only. All content and views are for reference only and do not constitute investment advice. They do not represent the views and positions of this platform. Investors should make their own decisions and trades. The author and this platform will not bear any responsibility for direct or indirect losses incurred by investors’ transactions.