A little over a year ago, the prospect of transforming into a Crypto Reserve Company (DAT) seemed like an effortless path for many enterprises aiming to inflate their stock valuations. The allure was so potent that some Microsoft shareholders even advocated for their board to explore integrating Bitcoin into the company’s balance sheet, citing the success of MicroStrategy, the preeminent publicly traded Bitcoin DAT.

This era was characterized by a powerful “financial flywheel.” The strategy was simple yet effective: acquire substantial quantities of Bitcoin, Ethereum, or Solana (SOL), witness the company’s stock price surge beyond the intrinsic value of these digital assets, then issue additional shares at a premium. The proceeds from these sales were then reinvested into purchasing more cryptocurrency, perpetuating a cycle that seemed almost infallible. Investors, eager for indirect exposure, were willing to pay a hefty premium – often more than two dollars for what amounted to one dollar’s worth of Bitcoin. Those indeed were extraordinary times.

However, even the most ingenious strategies and self-sustaining flywheels are subject to the test of time.

The Unraveling of the “Financial Flywheel”

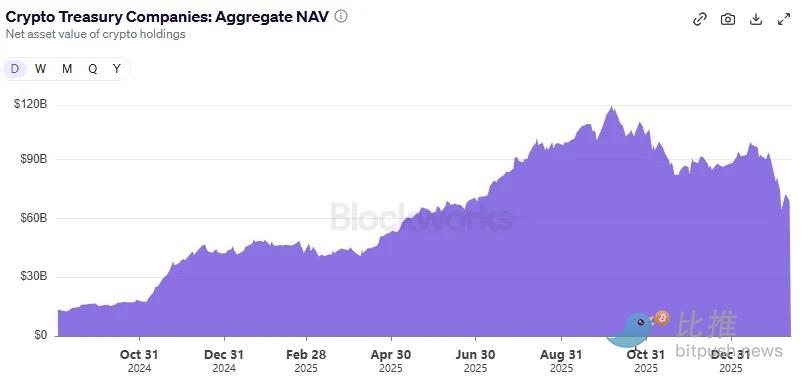

Today, the landscape has dramatically shifted. With the total cryptocurrency market capitalization plummeting over 45% in the last four months, the market capitalization to net asset value (mNAV) ratios for most of these “wrapper” companies have dipped below 1. This signifies a stark reality: the market now values these DAT companies less than the underlying crypto assets they hold. This fundamental shift has effectively broken the once-robust financial flywheel.

A DAT is more than just a passive holder of digital assets; it’s an operating entity with ongoing expenses, including operational costs, financing charges, and legal fees. During the mNAV premium era, DATs could comfortably fund their crypto acquisitions and operational overhead by issuing new equity or securing debt. In the current mNAV discount environment, this model is unsustainable, leading to the collapse of the very mechanism that once fueled their growth.

This analysis will delve into the profound implications of a persistent mNAV discount for DATs and explore their prospects for survival in an unforgiving crypto bear market.

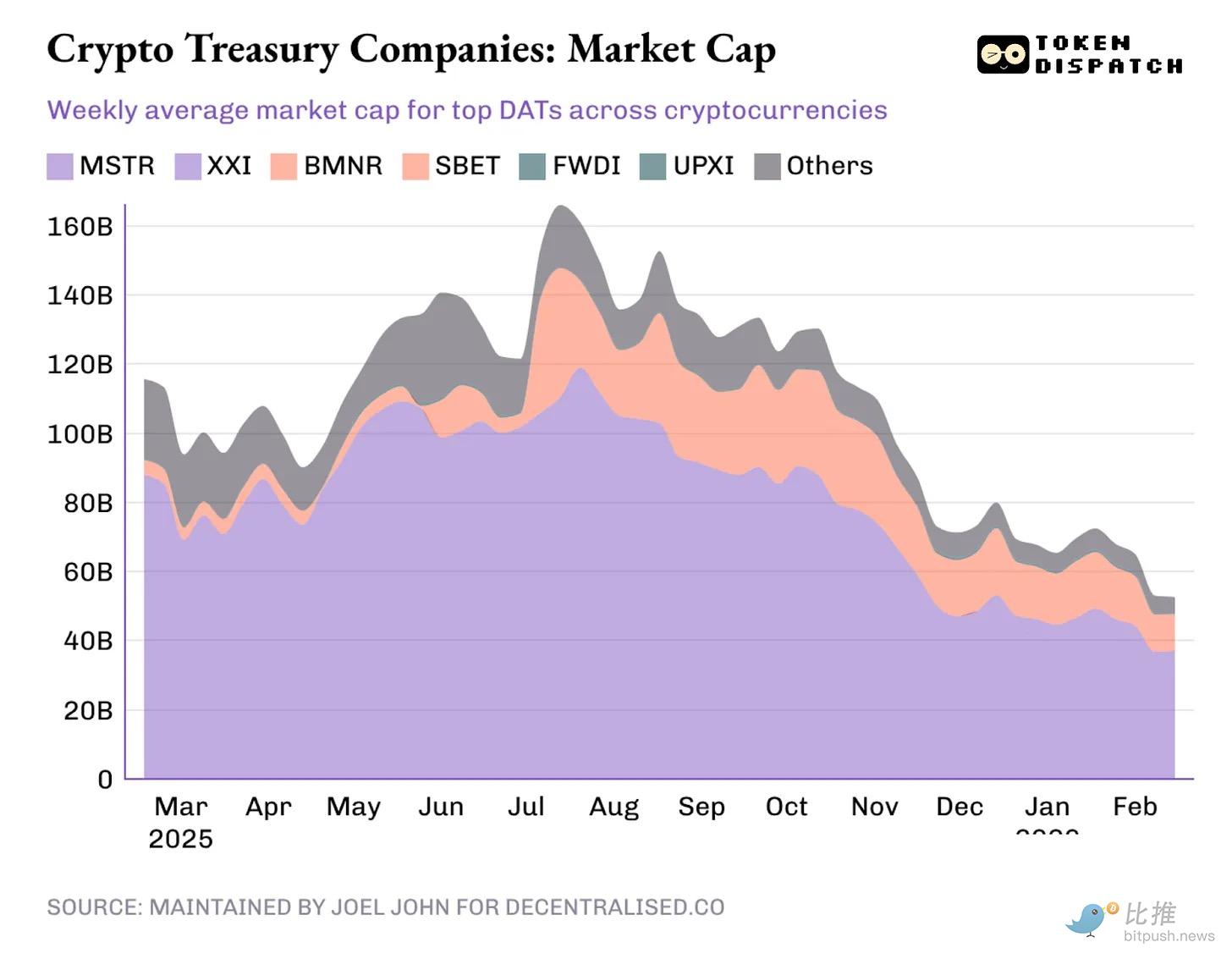

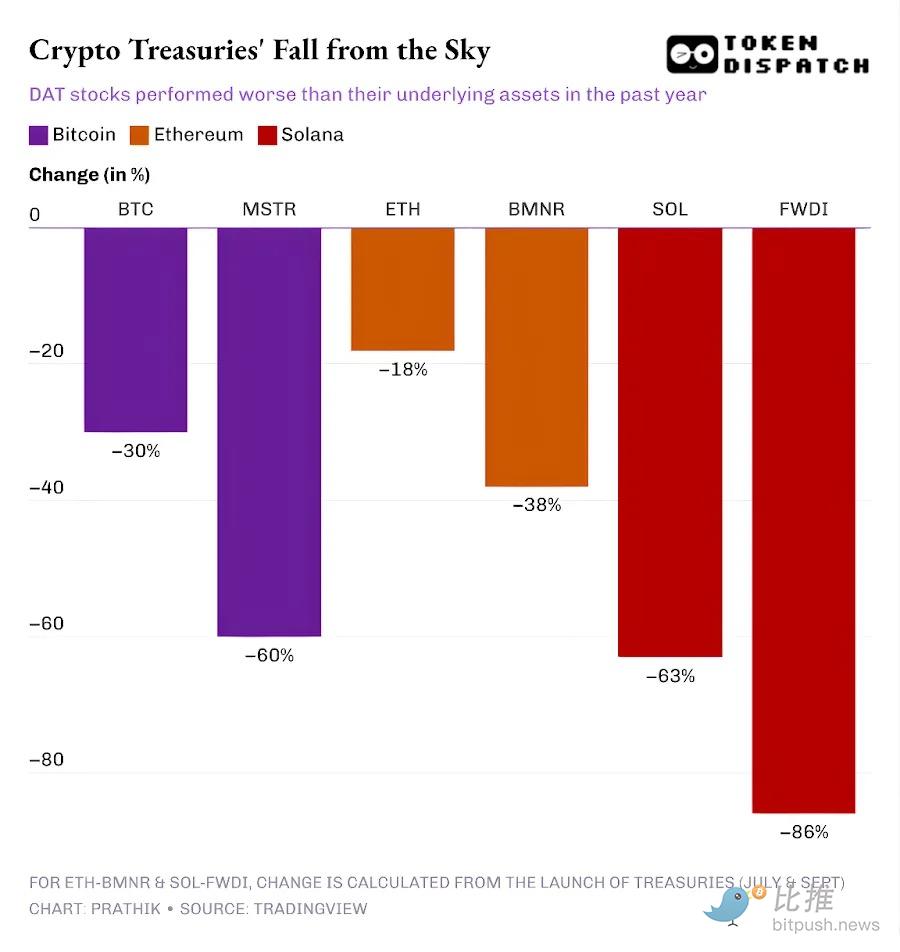

Between 2024 and 2025, a frenzy of over 30 companies vied to reposition themselves as DATs, amassing reserves in Bitcoin, Ethereum, SOL, and even meme coins. At its zenith on October 7, 2025, these DATs collectively held $118 billion in cryptocurrencies, boasting a combined market capitalization exceeding $160 billion. Fast forward to today, their crypto holdings have shrunk to $68 billion, and their aggregated market cap, now trading at a discount, barely surpasses $50 billion.

The prosperity of these entities was predicated on a singular ability: to package digital assets and craft a compelling narrative that elevated the perceived value of the “package” above its underlying components. This differential became known as the “premium.”

The premium itself became the core product. When a stock traded at 1.5 times its mNAV, a DAT could issue $1 worth of shares, acquire $1.5 worth of crypto exposure, and present this as a “value-accretive” transaction. Investors were willing to pay this premium, driven by the conviction that the DAT would continue to issue shares at an elevated price, using the proceeds to accumulate more crypto, thereby increasing the per-share crypto asset value over time.

The inherent flaw, however, is that premiums are not eternal. The moment the market ceases to pay extra for this “wrapper,” the “sell stock to buy crypto” flywheel grinds to a halt.

When a stock no longer commands a 1.5x multiple of its asset value, each newly issued share yields less cryptocurrency. The once-favorable premium transforms into a detrimental discount. Over the past year, the stock prices of leading Bitcoin, Ethereum, and SOL DATs have experienced declines even steeper than the cryptocurrencies themselves.

Once the premium vanishes, investors are left questioning the rationale for paying a premium for indirect exposure when they can acquire cryptocurrencies directly and more affordably through decentralized or centralized exchanges, or via exchange-traded funds. Bloomberg’s Matt Levine aptly posed a critical question: If a DAT trades below its net asset value, why wouldn’t shareholders compel the company to liquidate its crypto reserves or initiate share buybacks?

Many DATs, including industry stalwart MicroStrategy, attempt to reassure investors that they will weather the bear market, anticipating a return to the premium era. However, a more pressing concern emerges: without the ability to raise additional capital in the foreseeable future, how will these DATs cover their operational expenses, salaries, and other financial obligations?

Case Studies in Survival: MicroStrategy vs. Emerging DATs

MicroStrategy stands as a notable exception, primarily for two reasons:

- The company reportedly holds $2.25 billion in reserves, sufficient to cover its dividend and interest obligations for approximately 2.5 years. This resilience is partly due to its diversified funding strategy, which now includes preferred instruments requiring substantial dividend payments, moving beyond sole reliance on zero-coupon convertible bonds.

- Crucially, MicroStrategy maintains an operational business intelligence segment, however modest, that generates recurring revenue. In Q4 2025, the company reported $123 million in total revenue and $81 million in gross profit. While its net profit can fluctuate significantly due to quarterly mark-to-market adjustments in crypto asset prices, this business intelligence division represents the company’s only tangible source of cash flow.

Despite these advantages, MicroStrategy’s strategy is not immune. The market can still penalize its stock – as observed over the past year – potentially eroding its capacity to raise capital efficiently. While MicroStrategy may navigate the crypto bear market, newer DATs lacking substantial reserves or robust operating businesses to offset inevitable expenses will undoubtedly face immense pressure.

This divergence is even more pronounced among Ethereum DATs. Bitmine Immersion, the largest Ethereum-based DAT, relies on a marginal operating business to bolster its Ethereum reserves. For the quarter ending November 30, 2025, BMNR reported total revenue of $2.293 million from consulting, leasing, and staking. Despite holding $10.56 billion in digital assets and $887.7 million in cash equivalents, BMNR’s operations resulted in a net negative cash flow of $228 million, with all cash needs met through new share issuances.

Last year, BMNR found capital raising relatively easy as its stock traded at an mNAV premium for most of the year. However, over the past six months, the mNAV has contracted from 1.5 to approximately 1. Issuing more shares at a discount in such an environment would dilute the per-share Ethereum value, making it less appealing to investors than direct market purchases. This dynamic likely influenced BitMine’s recent announcement to invest $200 million in Beast Industries, a private company owned by YouTuber “MrBeast,” with plans to “explore collaboration on DeFi initiatives.”

Ethereum and SOL DATs might highlight staking revenue, an advantage Bitcoin DATs lack, as a buffer during market downturns. However, this doesn’t fully address their cash flow obligations. While staking rewards accrue in crypto, they cannot be directly used to cover fiat expenses like salaries, audit fees, listing costs, or interest payments unless converted. Companies must either generate sufficient fiat revenue or liquidate/re-hypothecate reserve assets to meet these needs.

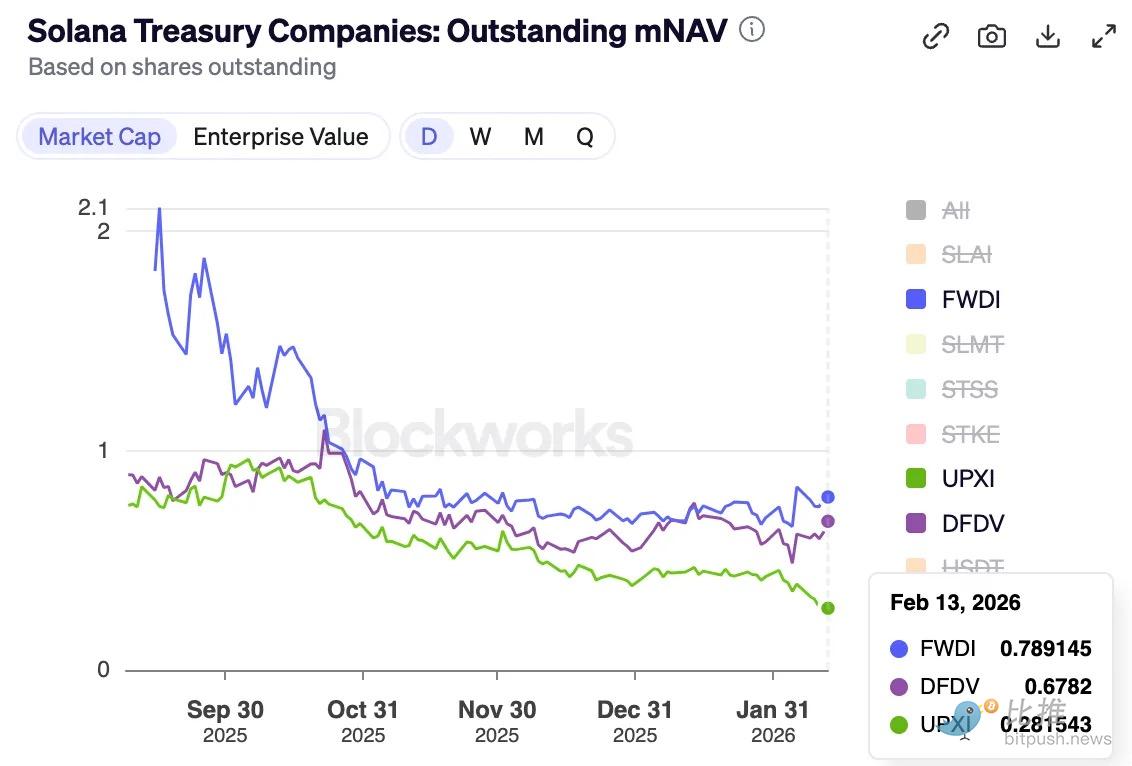

This challenge is evident in Forward Industries (FWDI), the largest SOL-holding DAT. FWDI reported a net loss of $586 million in Q4 2025, despite generating $17.381 million in staking and related revenue. While management asserts that existing cash and working capital are sufficient until at least February 2027, the company’s aggressive capital-raising strategy—including at-the-market equity offerings, buybacks, and a tokenization experiment—may falter if the mNAV premium remains elusive for an extended period.

The Path Forward: Redefining Survival for DATs

The DAT boom of the past year was fundamentally driven by the rapid accumulation of assets and the ability to raise capital through premium share issuances. As long as the “wrapper” traded at a premium, DATs could convert expensive equity into greater per-share crypto holdings, branding it as “beta.” Investors, in turn, often overlooked the inherent risks, focusing solely on asset price movements.

However, premiums are fleeting. The cyclical nature of the crypto market can swiftly transform them into discounts. This issue was first highlighted shortly after the October 10 liquidation event last year, when the initial decline in premiums was observed.

This ongoing bear market will force DATs to critically re-evaluate their very existence if their “package” no longer commands a premium. A viable solution lies in enhancing operational efficiency and complementing the DAT strategy with businesses that generate positive cash flow or substantial surplus reserves. When the DAT narrative loses its appeal in a bear market, a conventional, financially sound corporate narrative becomes paramount for survival.

As detailed in “MicroStrategy & Marathon: Faith & Power,” MicroStrategy’s enduring resilience through multiple crypto cycles stems from its operational strengths. Conversely, a new generation of DATs, including BitMine, Forward Industries, SharpLink, and Upexi, lack this foundational strength. Their current reliance on staking yields and nascent operating businesses may prove insufficient under sustained market pressure, necessitating a re-evaluation of their strategies to cover real-world financial obligations.

A compelling example of adaptation comes from ETHZilla, an Ethereum reserve company that recently sold approximately $115 million worth of Ethereum to acquire two jet engines. The company subsequently leased these engines to a major airline and engaged Aero Engine Solutions for monthly management. This strategic pivot highlights an innovative approach to generating tangible, fiat-based revenue.

Moving forward, the focus will not solely be on digital asset accumulation strategies but also on the underlying conditions that ensure their survival. In this evolving DAT cycle, only those companies adept at managing dilution, debt, fixed obligations, and trading liquidity will successfully navigate the downturn and emerge resilient.