Unraveling the “10 AM Dump”: Is Quantitative Trading a Market Manipulator or a Misunderstood Force?

In the volatile world of cryptocurrency, where market anxieties often amplify rumors, conspiracy theories frequently gain more traction than factual explanations. As Bitcoin wrestled persistently below the $70,000 mark and peculiar selling pressure consistently emerged around 10 AM ET on US stock trading days, investors began to suspect a hidden hand manipulating the market.

A curious phenomenon unfolded: the precise, almost clockwork-like “10 AM dump” seemed to vanish as quantitative trading giant Jane Street became embroiled in legal disputes related to Terraform Labs and faced accusations of market manipulation. This New York-based firm, renowned for its discreet, high-frequency algorithmic strategies, also happens to be a key Authorized Participant (AP) for leading Bitcoin spot ETFs like BlackRock and Fidelity.

On social media, Jane Street quickly became the primary suspect, accused of orchestrating daily price drops through its algorithms. However, a deeper investigation by PANews reveals that while Jane Street became a convenient scapegoat for market anxiety—a powerful, mysterious “villain” onto whom fears could be projected—it may not be the true architect of Bitcoin’s price movements.

Social Media Ignites Accusations: Jane Street as the “10 AM Dump” Mastermind

The narrative began with a simple observation. Starting in late 2023, astute traders noticed a consistent pattern: roughly 30 minutes after the US stock market opened, around 10 AM ET, Bitcoin spot ETFs would frequently experience a significant wave of selling pressure. This recurring event was quickly dubbed the “10 AM dump strategy.”

This wasn’t just a typical market pullback. The concentrated selling would rapidly deplete liquidity, triggering a cascade of liquidations for leveraged long positions. Prices would plummet to intraday lows in a panic, only to gradually stabilize later. This uncanny consistency pointed many towards algorithmic trading as the culprit.

Industry observers, including Milk Road, suggested the underlying logic: **exploit thin liquidity at the US market open to trigger a price crash, thereby lowering the cost for subsequent accumulation.** This tactic, akin to “marking the close” or “wash trading down” in traditional finance, aims to profit from structural market vulnerabilities.

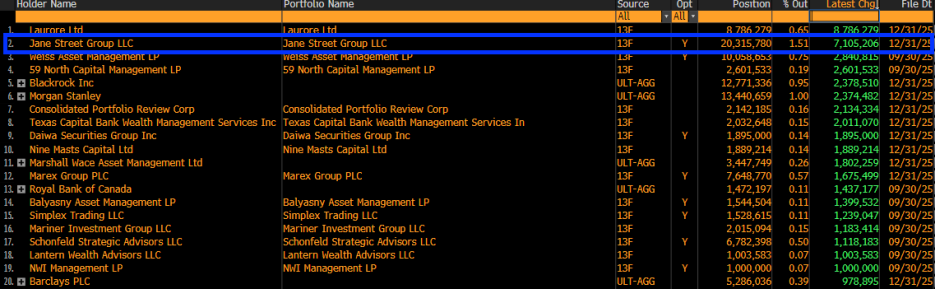

The conspiracy theory gained significant traction in early 2024 when Jane Street’s 13F filing revealed a substantial increase in its holdings of BlackRock’s spot Bitcoin ETF (IBIT) in Q4 2023. The firm had added over 7.1 million shares, bringing its total to 20.315 million shares, valued at approximately $790 million.

The data ignited a firestorm on social media: if Jane Street was accumulating Bitcoin on such a large scale, wouldn’t a 10 AM dump serve perfectly to depress prices and reduce their entry costs?

The logical chain seemed clear: **Motive (accumulation) + Means (algorithms) = Culprit (Jane Street).**

However, Louis LaValle, CEO of Frontier Investments, quickly tempered these assumptions, stating that interpreting 13F disclosures purely as “long accumulation” fundamentally misunderstands the market-making business model. As a major market maker and AP for IBIT, Jane Street’s ETF holdings are more likely to be part of a delta-neutral strategy, used to balance options positions or execute hedging, rather than a speculative directional bet.

Regulatory Spotlight and the Vanishing Strategy

While the 13F data might have been a misinterpretation, subsequent events lent a surprising twist to the debate. In February 2024, Todd Snyder, liquidator for Terraform Labs, filed a lawsuit accusing Jane Street of insider trading and market manipulation. The suit alleged that Jane Street used privileged communication with a Terraform insider to precisely exit positions just hours before the Terra ecosystem collapsed in May 2022.

Almost concurrently, Jane Street faced accusations from the Securities and Exchange Board of India (SEBI) for manipulating the BANKNIFTY index, leading to a proposed $550 million fine. The sudden glare of legal scrutiny on Jane Street coincided with an unexpected development: the regular 10 AM selling pressure on Bitcoin ETFs significantly eased, or even disappeared altogether.

This timing is difficult to dismiss as mere coincidence. PANews posits that in financial engineering, a trading strategy’s profitability (Alpha) rapidly erodes once it becomes widely recognized or subjected to regulatory scrutiny. Heightened regulatory risk compels algorithmic strategies to shift from aggressive profit-seeking to compliance and risk aversion, potentially leading to the dismantling of specific market patterns.

The disappearance of the “10 AM dump” suggests its prior existence and a strong correlation with regulatory pressure. However, it doesn’t definitively prove it was Jane Street’s exclusive strategy. What is certain is this: **when regulators scrutinize the internal operations of market makers, trading activities operating in regulatory grey areas are often curtailed due to compliance pressures.**

Why the “10 AM Dump” Contradicts Market-Making Logic

Despite public inclination to blame single entities for price declines, the conspiracy theory accusing Jane Street of deliberately suppressing Bitcoin prices largely fails under expert scrutiny.

Keone Hon, co-founder of Monad and a former quant at Jump Trading, along with Julio Moreno, research director at CryptoQuant, offered compelling technical rebuttals.

Hon highlighted that simply shorting IBIT cannot unilaterally depress Bitcoin’s spot price. While IBIT’s trading price is pegged to Bitcoin, it remains a secondary market stock. Should IBIT trade at a significant discount, Authorized Participants (APs) and arbitragers would swiftly intervene, buying the undervalued ETF shares and redeeming Bitcoin in the primary market to close the price gap. **This robust arbitrage mechanism ensures IBIT cannot diverge significantly from the spot price.**

Moreno further emphasized that Jane Street’s operations are consistent with any “delta-neutral” fund. As Xin Song, CEO of leading crypto market maker GSR Markets, once told PANews, **”Truly large market makers don’t bet on direction.”**

Indeed, for market makers like Jane Street, taking directional risk is inherently dangerous. Their goal is a balanced state of “zero net exposure.” When Jane Street acts as an AP, providing liquidity for IBIT, they manage constantly shifting inventory risk. If clients buy large quantities of IBIT, Jane Street, as the seller, holds a short position. To hedge this, they typically buy an equivalent amount of Bitcoin in the spot or futures market—a process known as “dynamic hedging.”

Under this model, Jane Street’s profits stem not from price appreciation or depreciation, but from:

- Bid-Ask Spreads: Earning revenue by buying at a slightly lower price and selling at a slightly higher price.

- Funding Rate Arbitrage: Locking in risk-free basis trade profits by simultaneously buying the ETF spot and selling futures contracts on exchanges like CME.

While these strategies involve substantial selling, they are always balanced by equivalent buying, rendering their net impact on market prices theoretically neutral. Macro analyst Alex Krüger further countered the claim with data, showing that since January 1st, IBIT’s cumulative return between 10 AM and 10:30 AM ET was a positive 0.9%.

PANews suggests that from a quantitative perspective, the “10 AM dump” was more likely a result of **large-scale hedging demand triggered by the inherent volatility of the US stock market open.** Given that IBIT’s liquidity is still stabilizing in the initial minutes of trading, such hedging operations could be amplified, mistakenly appearing as deliberate price manipulation.

Furthermore, firms like Jane Street manage enormous balance sheets. If their alleged manipulation caused Bitcoin’s price to collapse, their multi-billion dollar holdings in related assets and derivatives would face immense liquidity and counterparty risks, a scenario antithetical to their risk-averse strategies.

Structural Challenges: Bitcoin Spot ETF Price Discovery

While technical arguments largely debunk the conspiracy theory, ProCap CIO Jeff Park highlights a deeper issue: **the existing Authorized Participant (AP) mechanism within Bitcoin spot ETFs.**

APs wield significant influence due to their unique legal standing. Under SEC regulations, institutions like Jane Street enjoy privileges unavailable to ordinary traders:

- Short Selling Exemptions: APs are often exempt from standard securities short-selling restrictions when performing market-making duties. This allows them to sell ETF shares without physically borrowing the underlying asset, hedging instead through Bitcoin futures rather than direct spot purchases.

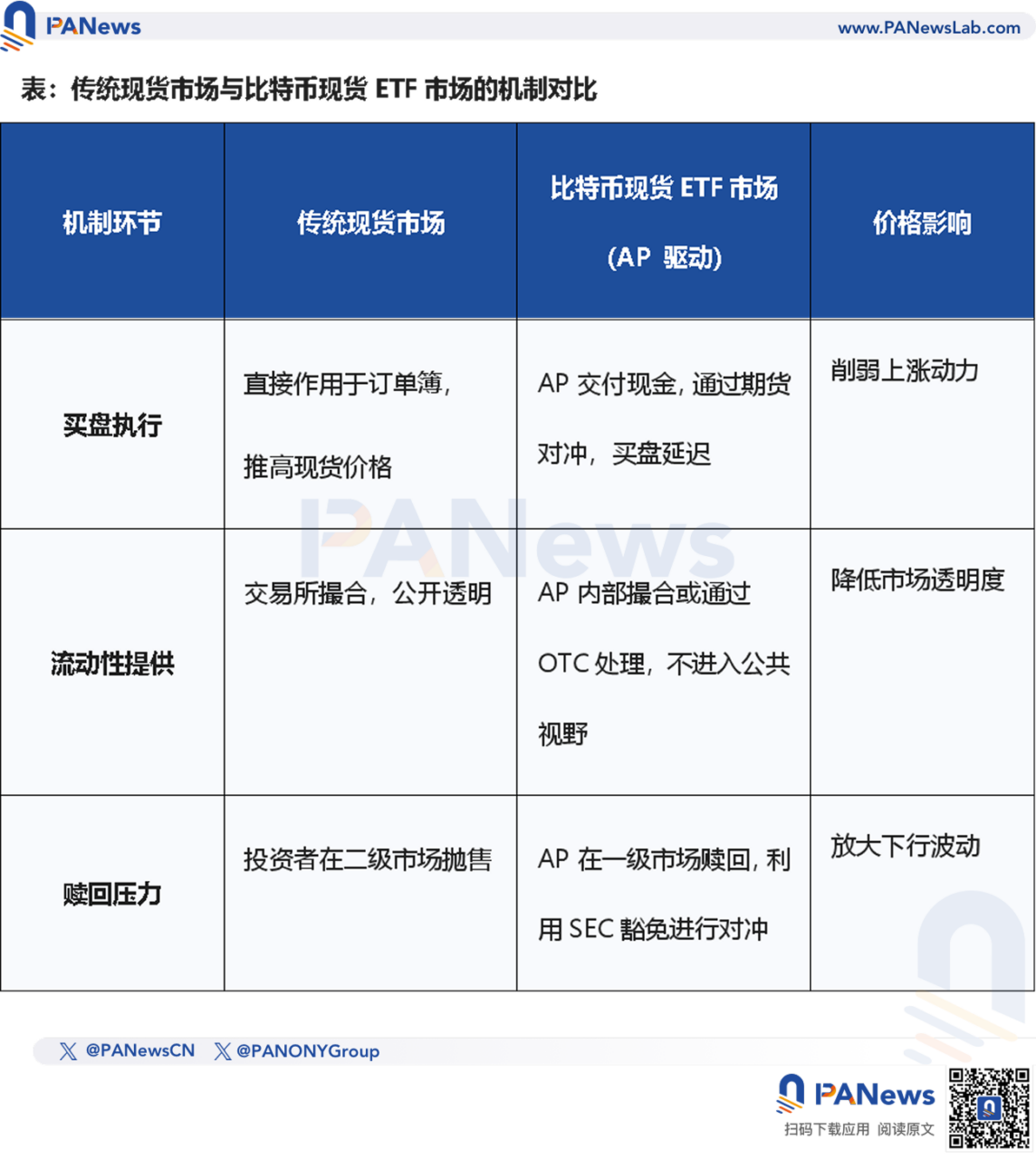

- Cash Creation/Redemption Model: Most current Bitcoin spot ETFs employ a “cash create/redeem” model, differing significantly from the “in-kind” or “physical” model used by traditional ETFs like gold.

Park argues that this AP mechanism could be undermining the price discovery function of the Bitcoin spot market. The “cash” model itself presents a fundamental challenge: Bitcoin held by APs remains “locked” in custodians’ cold wallets for extremely short periods. PANews believes that while this “locked state” reduces circulating supply, it also severs the direct link between ETF demand and the spot market.

Ideally, ETF demand should directly translate into spot market buying. However, the APs act as intermediaries, often hedging their risks via futures contracts rather than directly purchasing spot Bitcoin. **The consequence is that despite net capital inflows into the ETF, genuine buying pressure in the spot market may not be synchronously reflected.**

PANews concludes that when APs like Jane Street use short-selling exemptions to hedge through futures, they are essentially **”synthesizing” Bitcoin demand.** This means ETF capital inflows might not translate equivalently into upward momentum for the spot price, thus creating an objective “soft suppression” on prices.

This structural mismatch creates a paradox: **the larger the ETF grows, the more Bitcoin’s price discovery power becomes concentrated in the hands of a few APs. Jane Street, notably, is a central node in this power structure.**

Quantitative Industry: Market Evolution or an Invisible Ceiling?

“Quants never die, and market declines never stop.” This sentiment, suggesting quantitative trading suppresses market growth, is pervasive on social media. It’s a view that often reflects the emotional frustration of traditional investors.

This brings a profound question to the forefront: **Is quantitative investment the natural evolution of market “industrial civilization,” or an “invisible suppressor” of healthy market growth?**

Today, programmatic trading (encompassing high-frequency trading, algorithmic execution, and quantitative hedging) accounts for over 70% of the US stock market. In contrast, the nascent A-share market has seen its quantitative penetration surge from 5% to 25%-30% over the past decade.

Despite the growing dominance of quantitative trading and the increasing returns of top firms, the S&P 500 index has soared by 260% over the last decade, while China’s CSI 300 index has risen by approximately 60%.

This data suggests that **the expansion of quantitative institutions and robust market growth are not mutually exclusive.**

Rather than suppressing market uptrends, quantitative trading has profoundly altered the speed and dynamics of wealth distribution. In US equities, it has driven an industrial transformation; in A-shares, it might still be in a painful growth phase; and in crypto, quantitative giants are actively reshaping pricing power through structural tools like the ETF AP mechanism.

The perceived “suppression” is, in essence, the powerlessness felt by traditional investment methods when confronted with high-frequency algorithms and complex financial engineering. Quantitative trading is not a fleeting trend; it is an intrinsic part of the market’s ongoing evolution.

For crypto investors, instead of searching for a “villain,” a more productive approach is to understand the evolving mechanics of the ETF ecosystem. Grasping the operational logic of this “Wall Street money-making machine” is an essential lesson for every participant.

Conspiracy theories often spread faster than the truth because they offer simple, direct, and emotionally resonant explanations. However, the true market is far more complex and, often, far less dramatic. The real challenge may not be a single institution, but rather our collective tendency to overlook intricate mechanisms and crave simplistic answers.