The cryptocurrency sector finds itself in a trough of sentiment, overshadowed by the surging tide of AI innovation. Venture capitalists are pivoting, and many founders are contemplating a shift towards AI. This begs a crucial question: Is the crypto industry still a worthwhile endeavor? A recent data-driven analysis by Decentralised.co, dissecting protocol revenues, suggests a significant recalibration. It argues that crypto asset valuations are returning to rationality, signaling the end of an era marked by exorbitant premiums for infrastructure tokens. For founders, this means moving beyond empty narratives to construct business models grounded in tangible revenue and defensible moats, while imbuing tokens with genuine utility and rights.

Paradoxically, while the crypto market’s “Fear and Greed Index” hovers at historic lows, its underlying profitability has reached unprecedented levels. Since 2018, crypto-native protocols have collectively generated an astounding $74.8 billion in fees, according to DeFiLlama. Nearly half of this sum—$31.4 billion—was accrued within a mere 18-month span from January 2024 to June 2025.

Despite experiencing some of its most lucrative quarters in the past eight years, why does the industry remain gripped by such profound fear? The answer lies in a visible contraction. Over the last two months alone, twelve projects—including Entropy Protocol, Milkyway Protocol, Nifty Gateway, Rodeo, Forgotten Runiverse, Slingshot, Polynomial, Zerelend, Grix Finance, Parsec Finance, Angle Protocol, and Step Finance—have shuttered their operations. These were products meticulously crafted by passionate founders, some having operated for years. Adding to the unease, major players like OKX, Mantra, Polygon Labs, Gemini, and Binance have announced significant layoffs.

Conference attendance is dwindling, venture capital is increasingly flowing into AI, and developers are migrating en masse. This pervasive sense of gloom is palpable, encapsulated by the prevailing sentiment: “If you’re still in crypto, pivot to AI.”

But is this truly the path forward?

This question has been at the forefront of our analysis in recent weeks. Historically, nascent technologies are initially afforded a premium valuation, fueled by their novelty and grand potential. Consider the 19th century, when nearly 6% of the UK’s GDP was invested in railway stocks. Fast forward to 2026, and the capital expenditure of cloud service giants is projected to constitute 2% of US GDP. However, reality invariably sets in, and technological trends revert to more rational valuations. The ultimate test for any industry is its ability to demonstrate enduring value once this initial speculative fervor subsides.

This article delves into the historical trajectory of cryptocurrency revenue, examines the user stickiness inherent in the generated funds, and scrutinizes the true nature of competitive moats within the industry.

Unpacking the Revenue Streams

From its inception, the crypto industry has been a fertile ground for revenue generation. Centralized exchanges like Bitmex, Binance, and Coinbase quickly became highly profitable ventures. These entities, however, were privately owned, their revenues opaque. The advent of DeFi-native infrastructure, such as decentralized exchanges (Uniswap) and lending platforms (Aave), transformed this landscape, offering unprecedented transparency by making protocol revenues publicly accessible.

Initially, there was a strong expectation that the trading valuations of tokens would directly mirror the economic activity facilitated by these underlying infrastructures.

By 2022, Decentralized Exchanges (DEXs) commanded a significant 28.4% of total crypto revenue, generating $2.27 billion. The lending sector exhibited a similar trend of high concentration, with Aave and Compound alone capturing 82% of all lending fees. While clear leaders emerged, optimism also surrounded burgeoning protocols striving for market share.

The sheer novelty of the underlying technology was sufficient to drive substantial valuations.

The expansion of crypto into the consumer realm closely followed. NFTs, or non-fungible tokens, embodied a promising vision of embedding cultural value directly onto the blockchain. High-profile figures famously adopted PFP (profile picture) NFTs on platforms like X, fostering widespread belief in their potential for mass adoption. OpenSea, a leading NFT marketplace, generated an impressive $1.55 billion in revenue, capturing 71.7% of the entire NFT market. In retrospect, its $13 billion valuation seemed less outlandish, given its potential to evolve into a lasting monopoly.

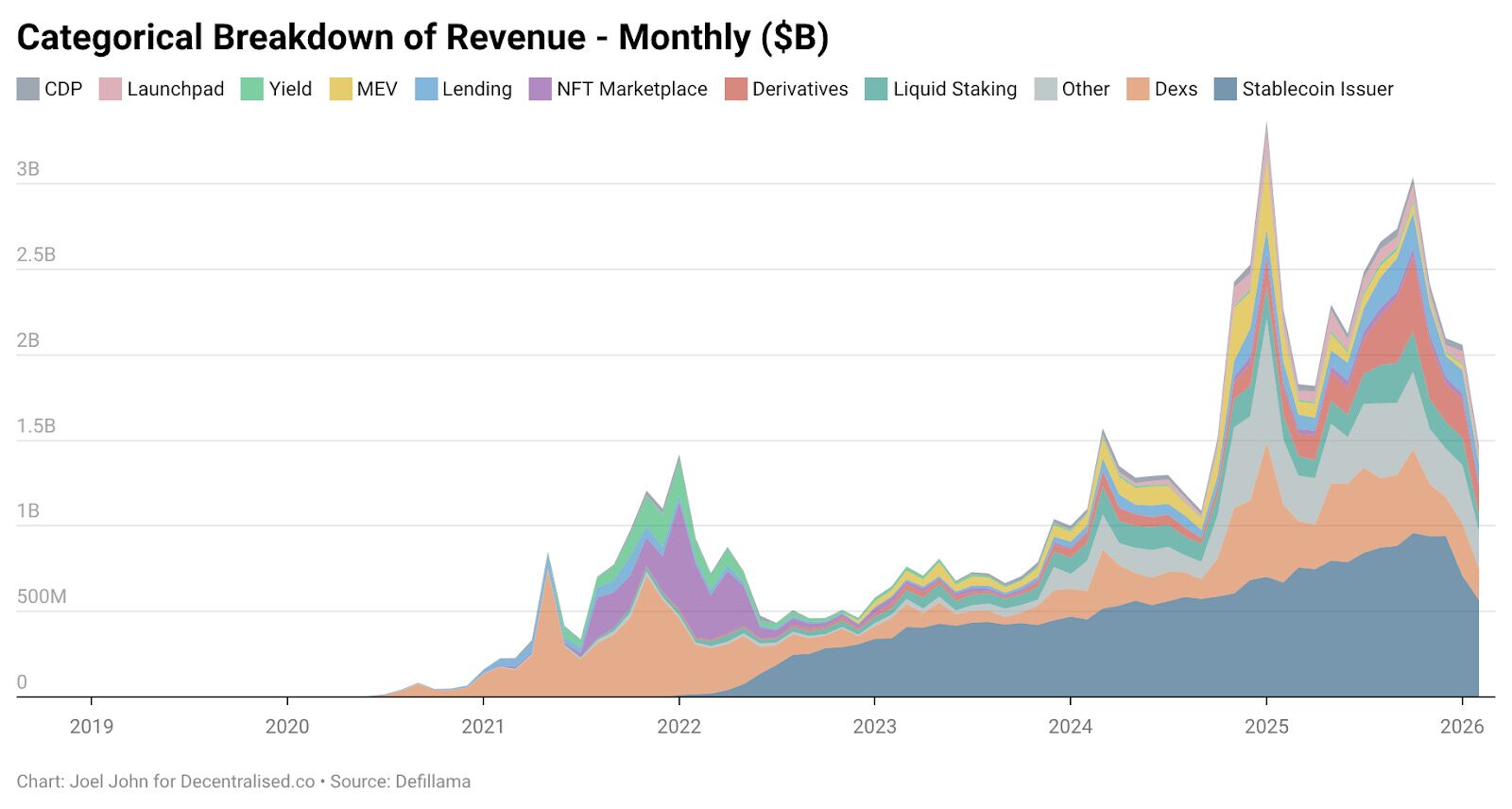

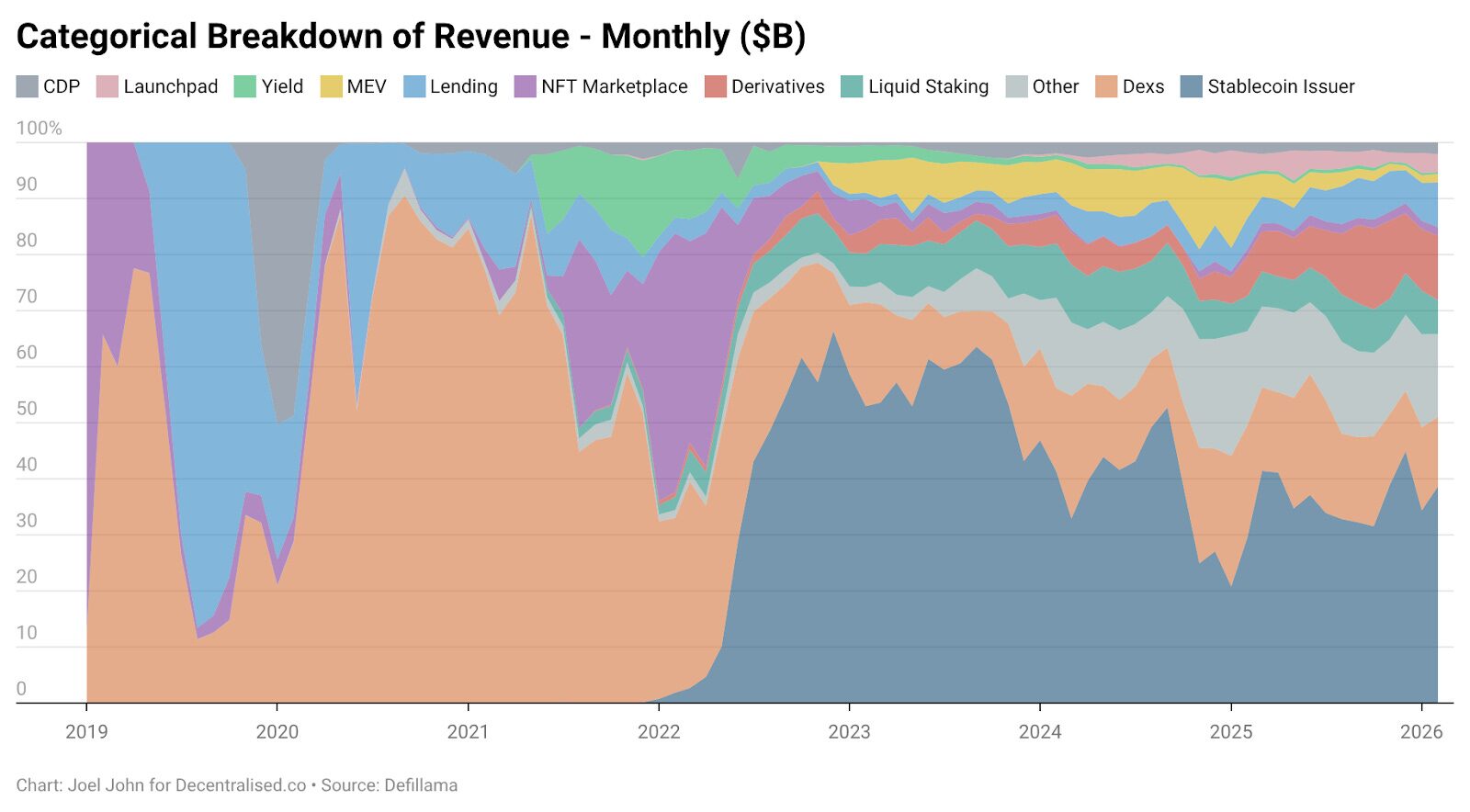

However, market dynamics had a different trajectory. By 2025, NFTs accounted for less than 1% of total crypto revenue. The industry experienced its “Beanie Baby moment,” albeit without any tangible collectibles left behind. Meanwhile, despite rapid development, DEXs struggled to sustain valuation growth. Last year, DEXs generated $5.03 billion in fees, and lending platforms added $1.65 billion. Combined, these two sectors now represent 22.9% of total fees, a notable decrease from 33.1% in 2022.

As their share of the broader economic pie diminished, so too did their valuations.

So, which sectors have truly flourished? How have crypto-native business models evolved since 2022?

The following chart offers crucial insights.

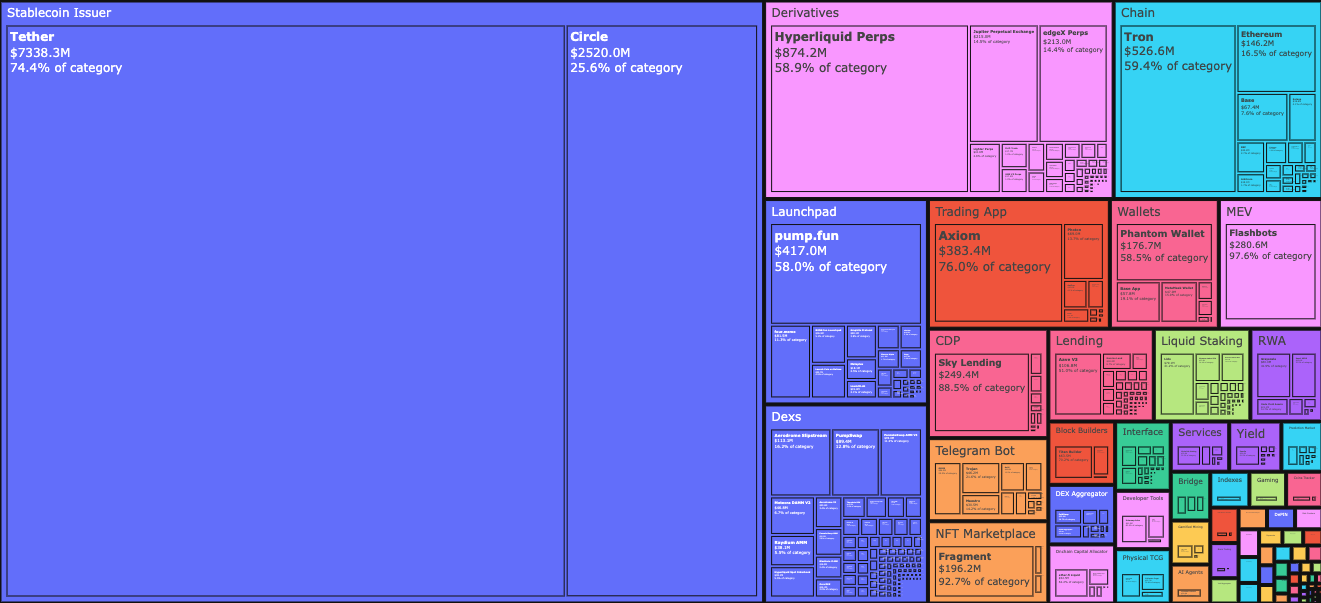

By January 2026, stablecoin issuers Tether and Circle commanded an astonishing 34.3% of all fees generated across the industry. To put this in perspective, for every dollar earned within the crypto ecosystem, $0.34 flowed directly to these two companies. Fueled by US Treasury bills, their combined revenue surged from $4.95 billion in January 2023 to $9.89 billion by 2025—a growth rate typically seen in startups, not established financial products operating at a banking scale. Notably, Tether’s revenue alone is nearly triple that of Circle.

Their meteoric rise can be attributed to two pivotal factors:

- Demand: Nations in the Global South consistently require robust tools to hedge against local inflation and facilitate the free movement of capital. Digital US dollars effectively fill this void, offering a stability and liquidity that local currencies often cannot match. This capital outflow is a fundamental economic driver.

- Cost Structure: Blockchain technology inherently absorbs the operational costs associated with running a stablecoin business. Unlike traditional banks or fintech firms, Tether and Circle are not burdened with the extensive overhead of hiring staff proportional to the scale of their on-chain stablecoin issuance. The marginal cost of minting an additional billion dollars on-chain or facilitating the transfer of another hundred billion dollars between addresses is virtually zero.

These two forces intertwine to create a powerful dynamic. On the demand side, citizens are actively “voting with their money,” driving stablecoin issuance to address real-world financial needs. Concurrently, the flattened cost curve makes stablecoin issuance one of the most capital-efficient operations in financial history.

The stablecoin business necessitates robust moats built on liquidity, compliance, and the Lindy effect—the principle that the future life expectancy of some non-perishable things, like technology or ideas, is proportional to their current age. Few issuers have demonstrated the resilience to navigate multiple market cycles. Tether and Circle collectively capture nearly 99% of all stablecoin issuance revenue. Their dominance stems from a crucial first-mover advantage. The network effects derived from integration across numerous exchanges bestow upon them a “legitimacy” that pure technological superiority alone cannot achieve.

Tether, for instance, initially launched as a sidechain on the Omni platform. Despite being slow and cumbersome, its accessibility through commonly used OTC desks and exchanges provided a powerful distribution moat, not a technological one. This type of moat proves particularly challenging for crypto-native founders to replicate solely through code.

Stablecoins, therefore, are a prime example of assets benefiting from the Lindy effect.

It wasn’t long before another category of cryptocurrencies began to capitalize on a similar distribution advantage.

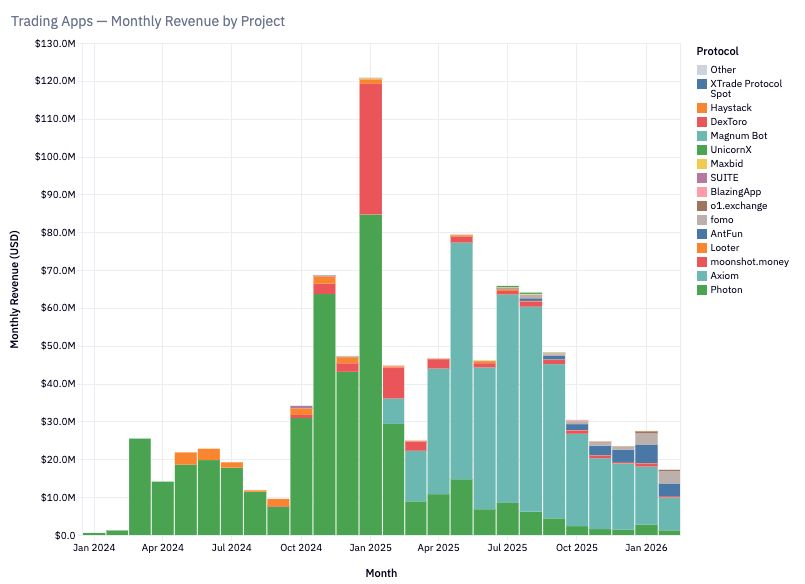

We’ve previously explored the concept of “cryptocurrency as a trading economy” in articles like “Money Movements” and last year’s “Everything is a Market.” What was not fully anticipated then was the explosive growth of trading products built around Telegram bots and intuitive trading interfaces.

These two niche areas alone generated $575 million in fees by January 2025. This rapid expansion is easily understood when considering consumer demand: meme coin trading and perpetual contracts offer users the allure of swift profits. The pursuit of quick returns drives a willingness to pay significant fees. Consequently, this category surged from just 1% of total revenue in 2022 to slightly over 15% by 2025.

Products such as TryFomo and Moonshot have generated millions in revenue by keenly focusing on the end-user experience. These offerings are not inherently complex from a technical standpoint. Instead, their strength lies in their ability to aggregate underlying crypto-native components and package them into a superior user interface. With the maturation of developer tools like Privy, builders are no longer burdened with incentivizing liquidity or cumbersome wallet management.

The native functionalities that captivated us in 2022 have now reached a state of robust maturity. Applications like BullX and Photon are prime examples of products built atop these foundational capabilities. This sector alone generated approximately $1.93 billion in trading fees between January 2024 and February 2026.

However, meme assets possess a critical flaw: they are functionally thin and inherently cyclical. Does this sound familiar? It should, as NFTs and Web3 games experienced similar cycles of explosive growth followed by eventual corrections. This cyclical nature is both a characteristic and a challenge for the crypto industry, a theme we will revisit. For now, let’s pinpoint where the revenue is truly flowing.

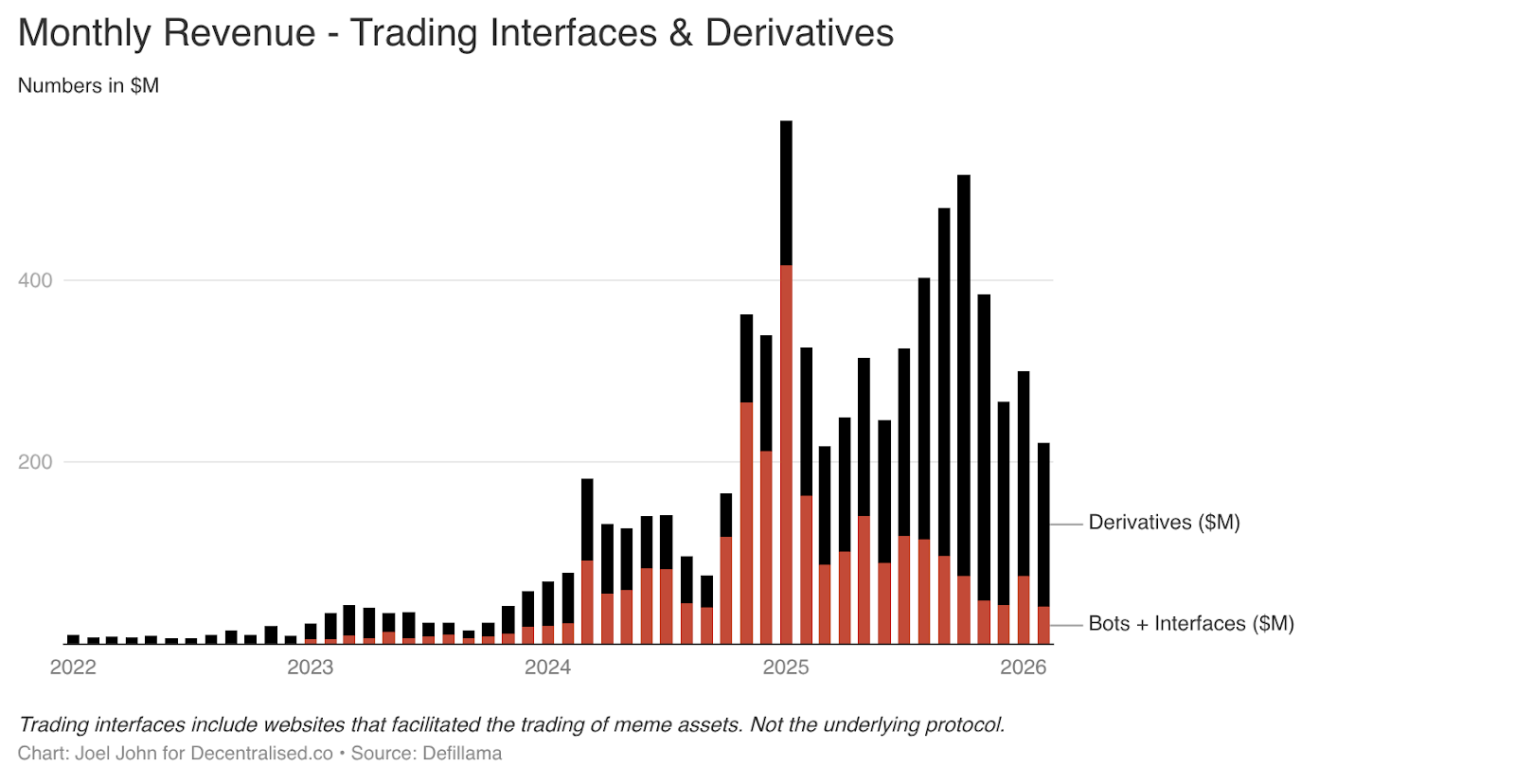

Perpetual futures exchanges, alongside the nascent prediction markets, represent a more enduring pathway. While platforms like PumpFun democratized asset issuance through meme coins, the underlying game often proved inequitable.

Eventually, the market came to terms with the ephemeral nature of meme coins. The dream of striking it rich by holding a token named “ShibaInuYouShouldShareThisNewsletter” faded. Users, it turns out, don’t want to manage arbitrary token portfolios; they want to manage risk. Perpetual exchanges perfectly address this demand.

These platforms allow for highly leveraged trading of major digital assets like Bitcoin, Solana, or Ethereum. This attracted both market makers and traders seeking decentralized alternatives to centralized venues. The core offering of this category is liquidity. Hyperliquid, for instance, has achieved dominance by offering order book depth comparable to centralized exchanges. Without such parity, there would be little incentive for users to migrate. Over the past three years, Hyperliquid and Jupiter have captured the lion’s share of fees in this category.

Perpetual futures exchanges and trading platforms have effectively demystified cryptocurrency. They unequivocally demonstrate that the true path to profitability lies in extracting small fees from high-frequency trading. These “meme trading platforms” and perpetual exchanges act as dopamine machines, packaging and selling risk in an accessible format.

One of these will likely evolve into a fundamental financial technology, enabling global 24/7 trading of commodities, stocks, and digital assets, even on weekends. Blockchain-native applications are effectively replicating a core function long provided by traditional platforms like Robinhood and Binance: the conduit for speculative capital.

The Protocol Predicament

Have you noticed the absence of discussion regarding the underlying protocols—the foundational layers that record all network transactions? Their narrative is distinct, yet equally critical. These protocols have become casualties of the “novelty premium,” a valuation driver that is now rapidly diminishing.

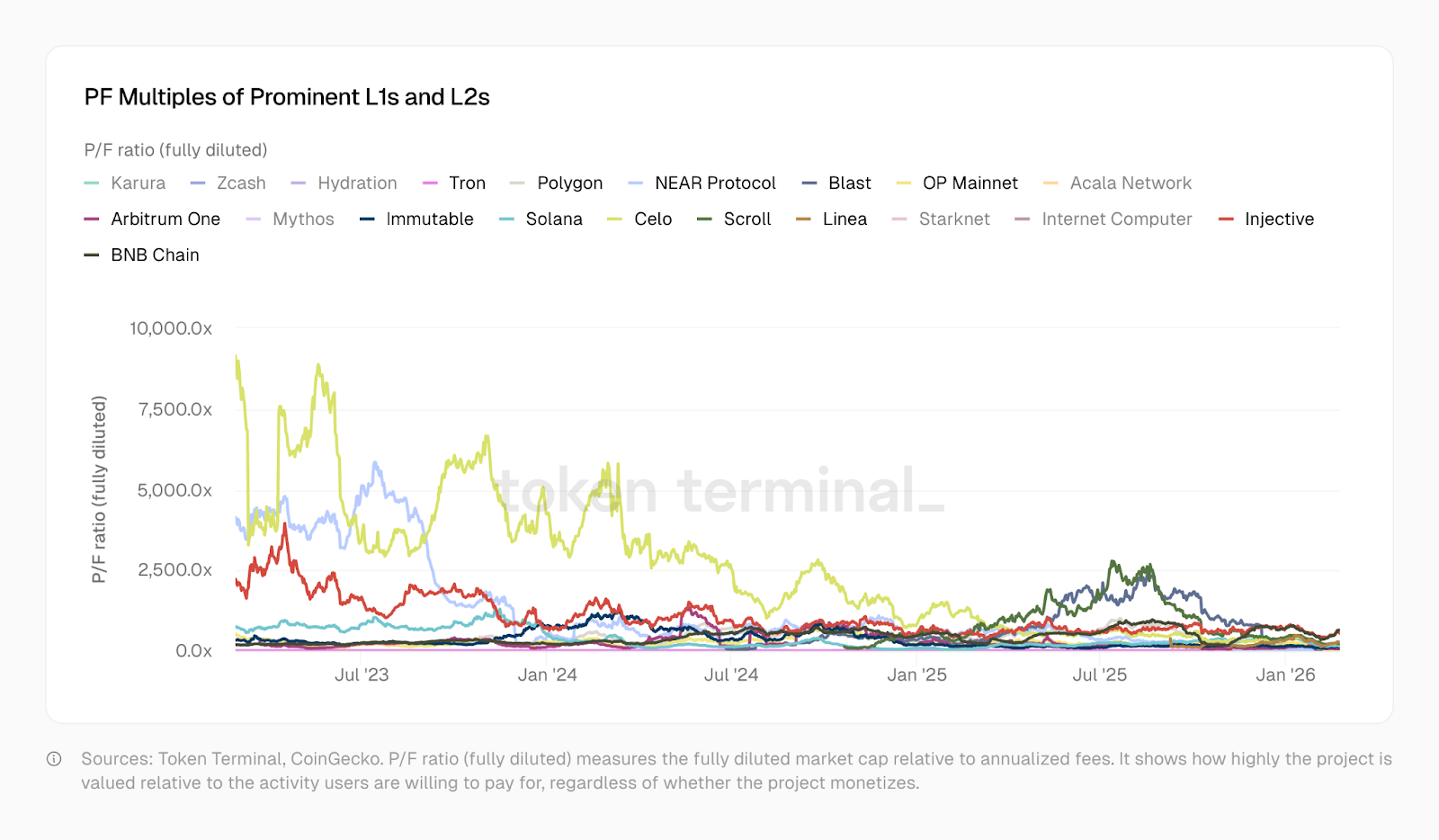

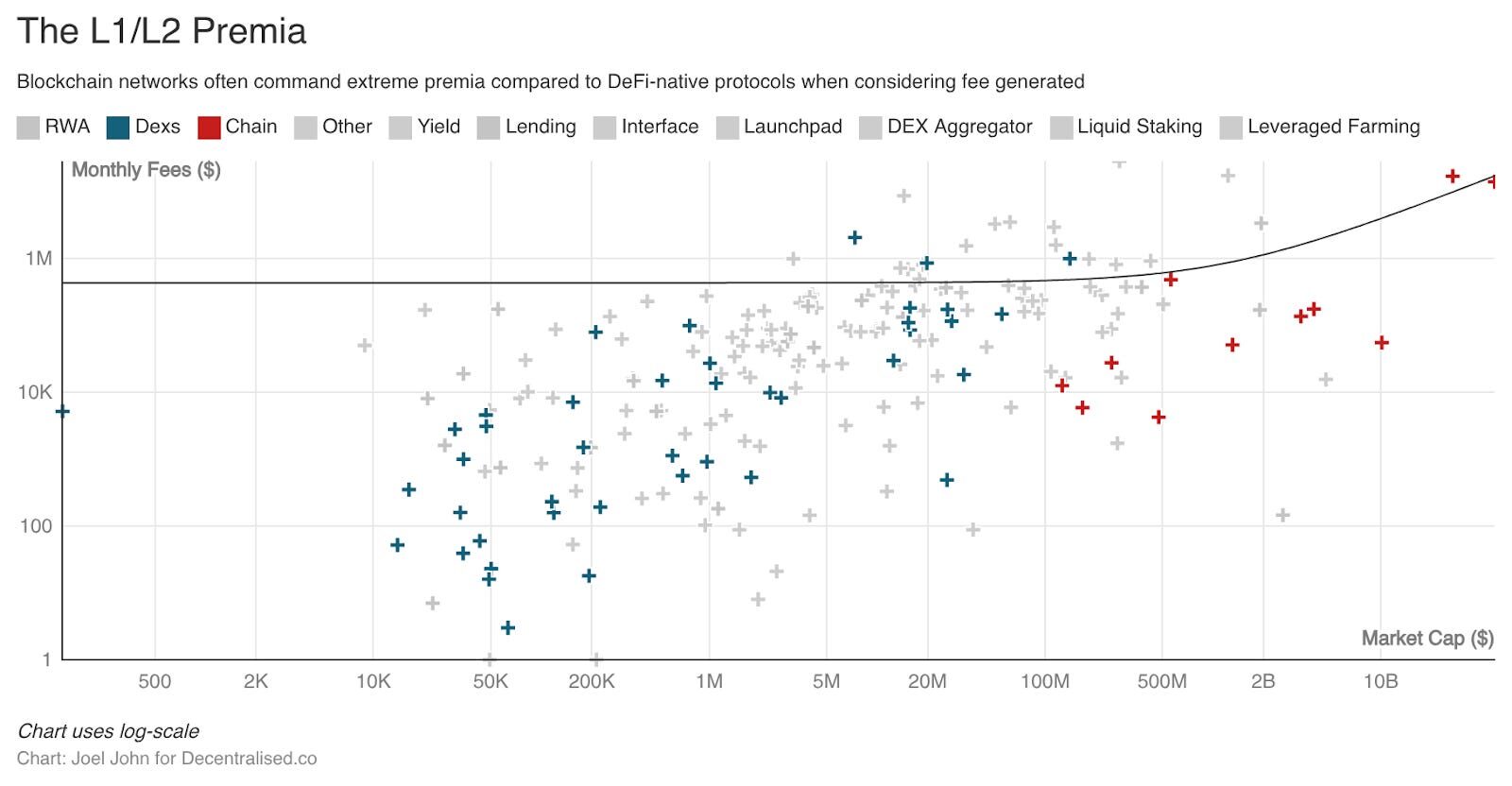

In January 2023, the Price-to-Fees (PF) ratio for Optimism stood at a staggering 465x, Solana at 706x, and Arbitrum and BNB around 206x. Today, these figures have sharply contracted: Solana is at 138x, Arbitrum at 62x, and OP at 37x. Polygon’s valuation, at 20x, now more closely resembles that of a traditional fintech company. Tron, which underpins a vast stablecoin ecosystem, trades at a PF of 10.2x. This significant re-rating has occurred despite Optimism, Solana, Arbitrum, and Polygon each developing more sophisticated products, attracting more users, improving liquidity, and supporting more complex financial application suites built on their foundations.

The dramatic reduction in their PF ratios serves as a stark reflection of the market’s revised perception.

Historically, Layer 1 (L1) and Layer 2 (L2) protocols commanded extremely high premiums compared to standalone infrastructure or projects. Had this premium been strategically invested, it could have catalyzed the creation of entirely new economic systems, funding developers to build applications with genuine utility for everyday users beyond the crypto niche. Instead, the open-source nature of these products and the ease of tokenization led to a proliferation of fifty identical product copies across thirty networks, fundamentally undermining composability.

Paradoxically, this fragmentation was deemed acceptable, given the existence of cross-chain bridges, messaging protocols, and myriad other fund transfer mechanisms. Yet, the value of these very mechanisms is now in steady decline.

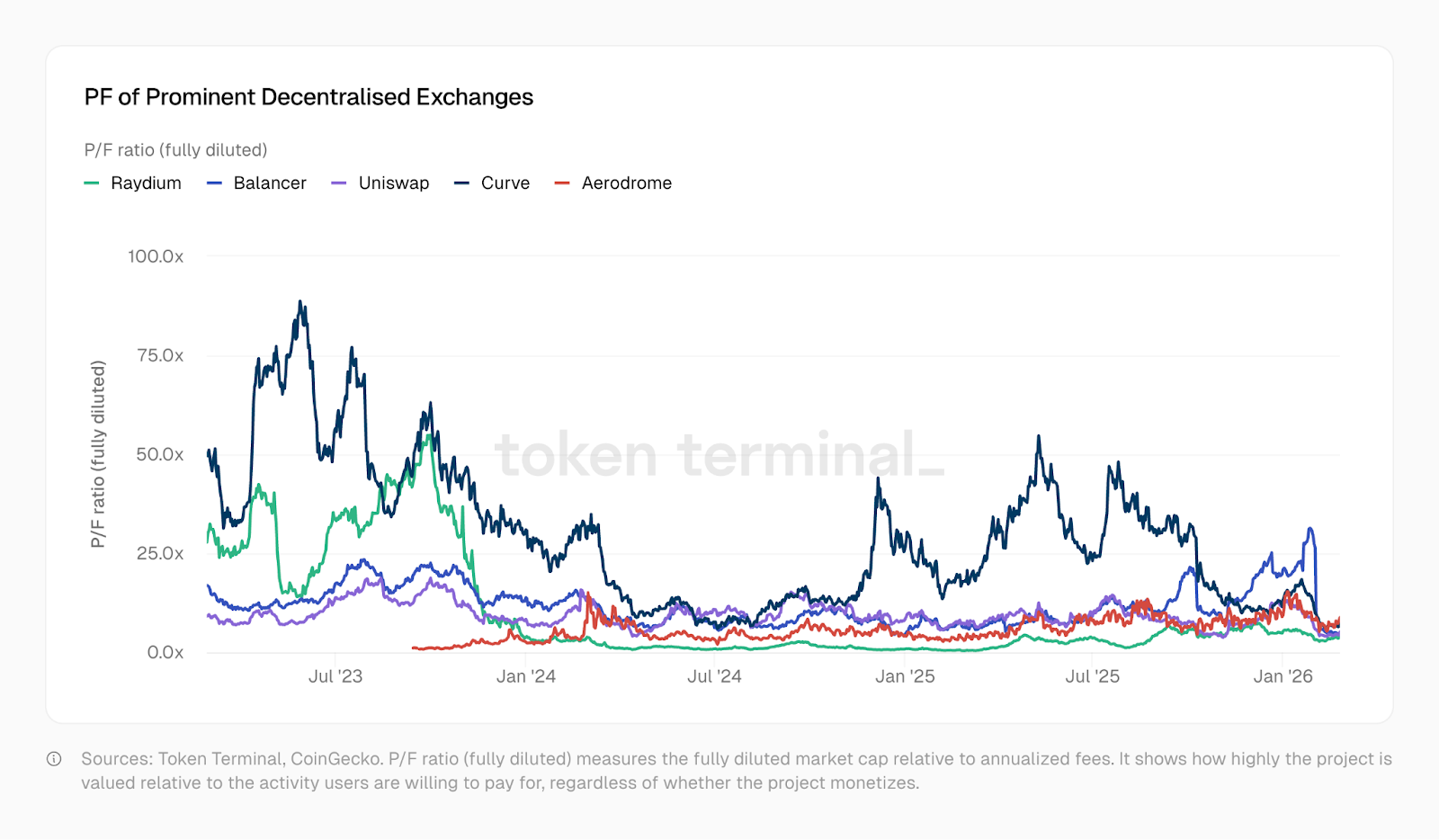

Consider the trajectory of foundational DeFi projects. An overwhelming array of investor choices, coupled with a lack of true innovation, has led to a precipitous drop in valuations, even for projects that demonstrably drive economic activity. These markets are highly fragmented, offering investors a multitude of options. The initial allure of “decentralized” or “blockchain-based” solutions has long faded. Projects like Kamino, Euler, Fluid, Meteora, and PumpSwap have emerged, yet their Price-to-Fees ratios remain below the levels seen in 2022 protocols. As illustrated by the TokenTerminal chart below, DEX Price-to-Fees multiples saw a significant decline between 2023 and 2025, with some exchanges now trading at multiples as low as 1.

In essence, the market is valuing these projects at less than the fees they are projected to generate in the coming year. This presents a curious paradox: while the valuations of underlying protocols—be they DeFi primitives or L1s themselves—are in decline, the applications built atop these very protocols are generating higher revenues in shorter timeframes.

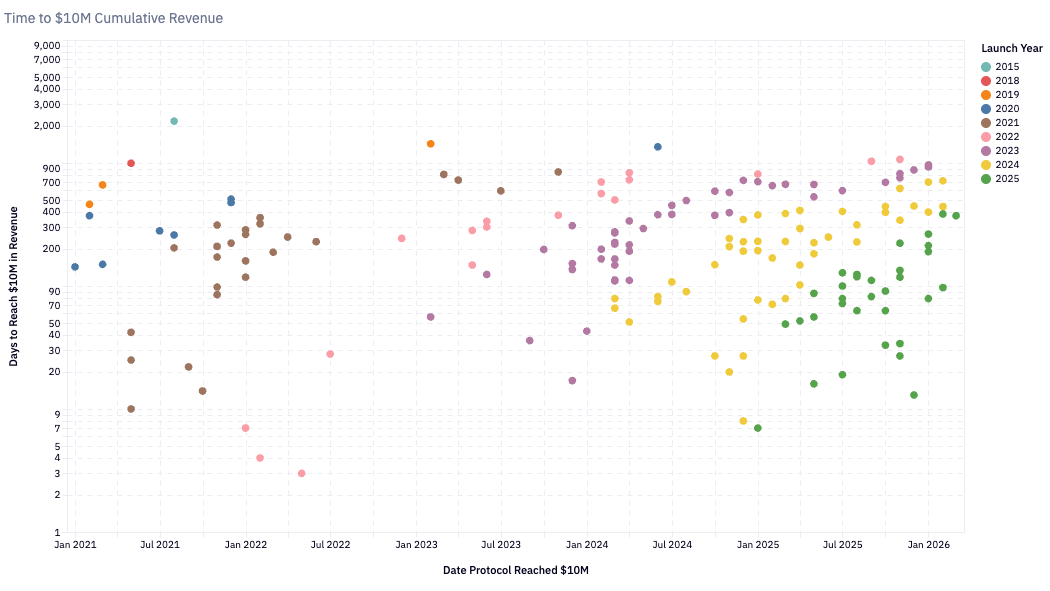

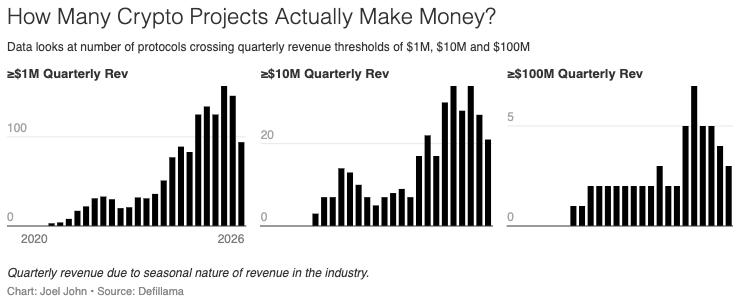

Since early 2020, the number of teams generating over a million dollars in quarterly revenue has consistently grown, now exceeding one hundred. In 2020, protocols that achieved $10 million in annual revenue within 24 months were considered rapid growth stories. By 2024, the timeline for protocols to reach this milestone has dramatically compressed to approximately six months. Pump.Fun, launched in early 2024, set a new record for accelerated growth, hitting $10 million in revenue in just about two months.

This accelerated growth reflects both the maturation of underlying infrastructure—faster chains and lower transaction costs—and the expanding pool of on-chain capital seeking both yield and entertainment. For developers and founders, these facts are critical to consider:

- Today, nearly 900 revenue-generating protocols exist within the crypto market.

- While each protocol vies for a diminishing median share of revenue, the broader trend indicates a growing number of teams successfully generating income. For context, the count of revenue-generating protocols has surged nearly eightfold, from 116 to 889.

- The median monthly revenue has, however, declined to a modest $13,000.

Blockchain-native enterprises typically possess three distinct forms of competitive moats, each evident when examining their revenue models:

- First-Mover Advantage: The network effects secured by early pioneers like Tether and Circle are exceptionally difficult to replicate. Despite continuous new entrants, these entities have endured multiple market cycles, solidifying a powerful duopoly. Notably, these businesses remain largely untokenized and are highly financialized. Tether, as a centralized entity, derives the majority of its revenue from US Treasury bills.

- Liquidity Moat: In an industry where capital is inherently utilitarian, protocols like Aave have demonstrated an ability to maintain deep liquidity across various market cycles. Hyperliquid appears to be achieving similar success, though it is still early to draw definitive conclusions. These protocols are incentivized to return value to liquidity providers and often adjust their tokenomics to emphasize governance functions.

- Distribution Moat: Cyclical consumer applications, such as meme coin trading platforms, thrive on the speed of capital rotation and immediate consumer demand. Web3 games and NFTs serve as excellent examples. The advent of AI-powered productivity means lean, agile teams can now launch consumer-facing products at an accelerated pace. The core advantage here boils down to the ability to effectively onboard and retain the maximum number of users during periods of market exuberance.

While products built on distribution moats can be immensely valuable, they often represent exceptions rather than the norm. Traditionally, a startup’s value often stems from the replicability of its success; Y Combinator’s model, for instance, benefits from the “Lindy effect” of proven ideas. However, the crypto landscape evolves at such a rapid pace that this Lindy-effect-based replication of experience is challenging. This partly explains why founders rarely replicate their consumer-facing successes across different crypto ventures. The cyclical factors that initially propelled a business to scale might simply not be reproducible.

This does not imply that founders should shy away from these opportunities. Niche segments, such as prediction markets or data providers for agent-economy products, can generate substantial short-term cash flow. However, it is crucial to recognize these as high-volatility, ephemeral plays that may not endure. A common pitfall for such products is the blind pursuit of venture capital or the entanglement with a token launched long after the foundational “meta” or core narrative that gave the product life has faded.

So, what truly confers value upon tokenized enterprises? Are their current valuations justifiable?

The data provides some illuminating clues.

Re-evaluating Governance and Value

In 1999, many technology companies commanded Price-to-Sales (P/S) ratios of 10x to 20x, with content delivery network Akamai reaching an astonishing 7434x. By 2004, Akamai’s P/S had plummeted to 8x. Across the board, numerous companies saw their P/S ratios collapse from 30x-50x to below 10x. The dot-com bubble’s burst obliterated trillions in speculative value. Yet, many ultimately survived because their underlying businesses possessed genuine utility. Amazon, for example, saw its stock price fall 94% from the bubble’s peak, only to emerge as one of the most valuable companies in history.

The crypto industry is currently undergoing a similar, yet even more rapid, market capitalization contraction. In 2020, when DeFi was still in its experimental infancy, the total annual revenue generated by the crypto sector was a modest $21 million. At that time, the average P/S ratio for all tracked protocols soared to an incredible 40,400x—a valuation driven purely by speculative visions of “what crypto could be.” By 2021, with the arrival of “DeFi Summer” and protocols generating actual earnings, the P/S ratio plummeted to 338x. Today, with annualized revenue at $18 billion, the average P/S ratio stands at approximately 170x. This dramatic compression from 40,400x to 170x has occurred in just five years.

However, a critical distinction remains. When Visa trades at an 18x P/S ratio, its shareholders benefit from dividends and share buybacks, possess legal ownership of company earnings, and hold corporate governance rights under securities law. In contrast, when Aave trades at a 4x P/S ratio, its token holders primarily hold governance rights, yet until very recently, lacked direct economic claims to the protocol’s earnings. Hyperliquid’s use of its aid fund for buybacks positions HYPE holders as one of the closest approximations to equity holders within DeFi. Aave itself recently approved a $50 million annual buyback program in 2025, signaling a shift.

While significant, these initiatives remain exceptions. Across the broader market, most protocols still lack robust mechanisms to return value directly to token holders. Despite seemingly low P/S multiples, the rights afforded to token holders are generally weaker than those in traditional markets. These multiples are only sustainable because the crypto industry generates revenue with a scale and efficiency unparalleled by conventional businesses.

The protocols contributing to crypto’s lower P/S ratios are not sprawling organizations with thousands of employees. Instead, they are lean teams operating global financial infrastructure with near-zero marginal costs and no physical offices. This raises critical questions: How minimal can these operational costs truly become? And to what extent can token holders trust these teams to responsibly utilize protocol revenues?

A granular breakdown by sector offers a clearer market perspective. Aave, the largest lending protocol in DeFi, trades at a P/S ratio of approximately 4x. Hyperliquid, which commands roughly 80% of the decentralized perpetual futures market, has a P/S ratio of about 7x. These are not speculative “bubble” multiples; arguably, they are even lower than their closest traditional finance counterparts. Coinbase, the sole publicly traded major crypto exchange, has a P/S ratio of around 9x. The CME Group, the world’s largest derivatives exchange, trades at about 16x P/S. Visa, a payments infrastructure giant, hovers around 15x P/S.

Crypto analyst Will Clemente once posited in a podcast that cryptocurrency represents capitalism in its purest form. Indeed, no other industry boasts successful enterprises achieving an estimated profit per employee as high as Tether’s potential $100 million. For context, Nvidia’s revenue per employee is $5.2 million, Apple’s is $2.4 million, and Google’s is $2 million. With just 125 employees and an estimated annual revenue of $12.5 billion, Tether’s scale suggests an unprecedented profit per employee in corporate history.

While the overall P/S ratio of 170x might appear astronomical, the market is not acting irrationally when it comes to genuinely revenue-generating protocols. Their pricing is often on par with, or even below, that of traditional financial infrastructure.

This naturally leads to the fundamental question: What is the true purpose of a token? In many contexts, tokens have proven to be potent tools for coordinating capital and aligning diverse stakeholders towards a shared vision. The crypto landscape is now characterized by entrenched duopolies. Traditionally, founders would raise debt (collateralized by equity) or equity to capitalize financial products. However, projects like Hyperliquid, Uniswap, Jupiter, and Blur have demonstrated that token incentives can effectively draw capital into new products. When tokens are coupled with governance rights, these stakeholders can contribute even more significantly. In this light, tokens may evolve to serve two primary functions:

- To coordinate capital and resources from aligned participants.

- To empower these participants with the ability to govern the underlying protocol.

The token itself, in isolation, is losing inherent value—even traditional stocks are now being tokenized. These digital instruments must confer a claim on economic activity and the power to direct governance. Many Layer 1 and Layer 2 tokens struggle to achieve both. With teams and VCs often holding the majority of tokens, retail holders are frequently left in a state of uncertainty, offering little incentive for ordinary investors to engage with newly listed digital assets.

Currently, attempts to redefine token utility are diverging. MetaDAO, for instance, offers holders full refunds if the team makes misrepresentations—a model yet to be adopted by larger protocols. The core challenge in cryptocurrency remains the limited rights traditionally afforded to token holders. Protocols are now actively grappling with the enduring question: Why should anyone hold these assets? Future analyses will delve deeper into the intricate relationship between holder rights and valuation.

The Crossroads: A Path Forward

Over the past two decades, global capital markets have become increasingly interconnected, a trend largely facilitated by technological advancements. We can now seamlessly trade commodities, international indices, digital assets, and soon, even computational resources like GPUs. Blockchain technology has been instrumental in enabling these markets to operate globally and around the clock. The ongoing shift by major exchanges like Nasdaq and the New York Stock Exchange towards 24/7 trading models stands as a testament to technology’s transformative power.

We inhabit a profoundly financialized world, where, ironically, news of conflict often prompts a rush to find the most opportune prediction markets for speculation. For founders, this reality necessitates a fundamental re-evaluation of what they build and how. If the data presented in this article offers any overarching insight, it is that all blockchain products ultimately generate profit through one of two core principles:

- By extracting small commissions from high-frequency transactions, or

- By charging larger commissions on transactions where verifiability and trust minimization are paramount.

The competitive advantage, therefore, lies either in transactional speed or in verifiable transparency.

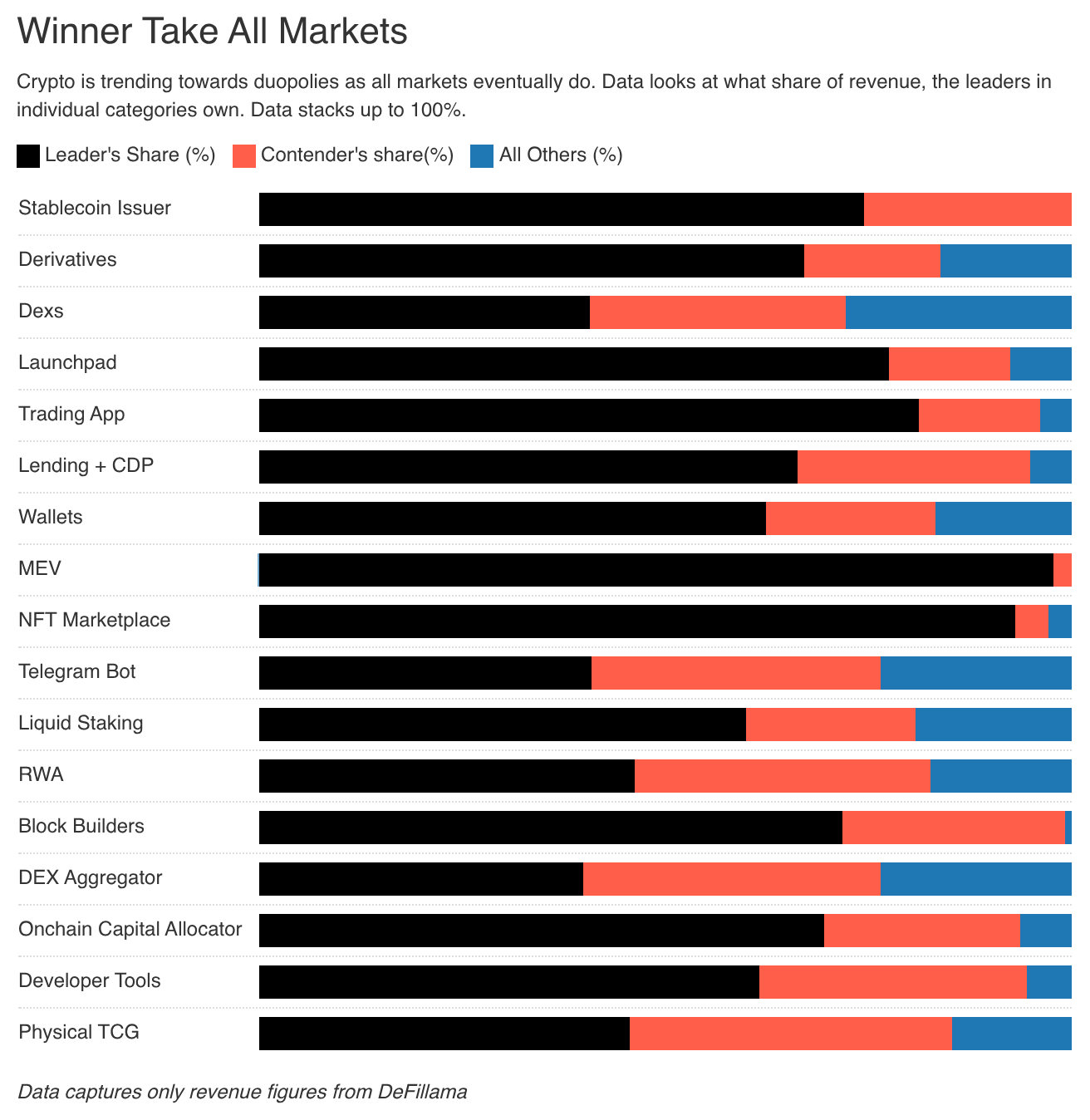

The profit motive remains the purest driving force for participants in capital markets. It is a widely accepted axiom that markets ultimately gravitate towards extreme efficiency. This trend is vividly illustrated by industry leaders; as observed in our charts, multiple market segments see 70% of their share concentrated in the hands of just two key players. This represents a harsh reality for all stakeholders and a fundamental aspect of market operation. For founders, it signifies that capital once flowing into their tokens is now being reallocated towards assets offering either higher volatility or superior capital returns.

Long-term capital does exist and may even command a premium, but only if it genuinely recognizes the intrinsic value of the underlying business. Investors in Google and Amazon are not compelled to rush for the exits because the core operations of these companies are inherently valuable and robust.

In an era where the value proposition of software itself is being scrutinized, blockchain-native applications must innovate to demonstrate tangible value. While token restructuring or even the on-chain trading of startup equity are possibilities, the challenge extends beyond mere tokenomics; it is fundamentally a business model problem. The vast majority of long-tail blockchain applications—encompassing Web3 social, identity, and gaming products—struggle to achieve scale or meaningfully differentiate themselves from traditional counterparts. These experiments are not without merit, but the industry has yet to effectively monetize them.

The era of simply building cryptocurrency infrastructure is behind us. Moving forward, blockchain will seamlessly integrate with the internet. Just as we no longer speak of “online” businesses because existence is inherently networked, or identify solely as “mobile app developers” because development itself is ubiquitous, so too will blockchain become an invisible, integral layer.

Long live the blockchain enthusiasts! We are, at our core, ledger maximalists, perpetually contemplating the optimal utilization of these transformative ledgers.