Author: Fenrir, CryptoCity

US Regulators Affirm ‘Tech-Neutral’ Stance for Tokenized Securities: Same Capital Rules Apply

In a significant development for the evolving landscape of digital finance, the U.S. Federal Reserve (Fed), in collaboration with the Federal Deposit Insurance Corporation (FDIC) and the Office of the Comptroller of the Currency (OCC), has issued new guidance for the banking sector. This guidance, presented as a Frequently Asked Questions (FAQ) document, clarifies the regulatory capital treatment for tokenized securities, explicitly stating that banks holding or processing these digital assets must adhere to the identical capital requirements as their traditional counterparts.

The core principle underpinning this directive is “technology neutrality.” Regulators emphasize that the method of issuance or trading for a security—whether it leverages blockchain or distributed ledger technology (DLT)—typically does not alter its fundamental capital regulatory treatment. The crucial factors remain the asset’s inherent legal rights and risk structure. If these align with traditional securities, then the capital requirements should remain consistent.

This approach signals a clear regulatory philosophy: the legal characteristics and risk profile of a financial asset are paramount in determining capital rules, not the technological platform or format through which it is issued.

Consistency in Capital Rules: Blockchain Format Irrelevant for Regulatory Requirements

Capital adequacy is a cornerstone of the banking regulatory framework, ensuring institutions maintain sufficient high-quality capital and liquid assets to absorb potential losses and market volatility. The recent clarification underscores that if a security is already recognized as a qualified financial asset, its tokenized form will not introduce new capital calculation methodologies.

For instance, a tokenized bond or stock held on a bank’s balance sheet will be subject to the exact same capital treatment as its non-tokenized version. This eliminates potential regulatory arbitrage or additional burdens simply due to the asset’s digital format.

Furthermore, the guidance confirms that tokenized securities, provided they meet existing legal and risk management criteria, are eligible for use as financial collateral. Banks utilizing these assets for collateral purposes must apply the same haircut percentages and risk management standards as they would for traditional securities.

A key highlight of the regulatory statement is its explicit declaration that the specific type of blockchain—whether a permissioned (private) or permissionless (public) network—has no bearing on the capital treatment. This further reinforces the technology-neutral stance, focusing on the asset’s substance over its technological wrapper.

The Rise of Tokenized Assets and Accelerating Regulatory Clarity

The financial industry has witnessed a burgeoning trend of converting traditional assets like stocks, bonds, and real estate into digital tokens on blockchain networks. This transformation aims to unlock greater transaction efficiency, enhance market liquidity, and reduce operational costs.

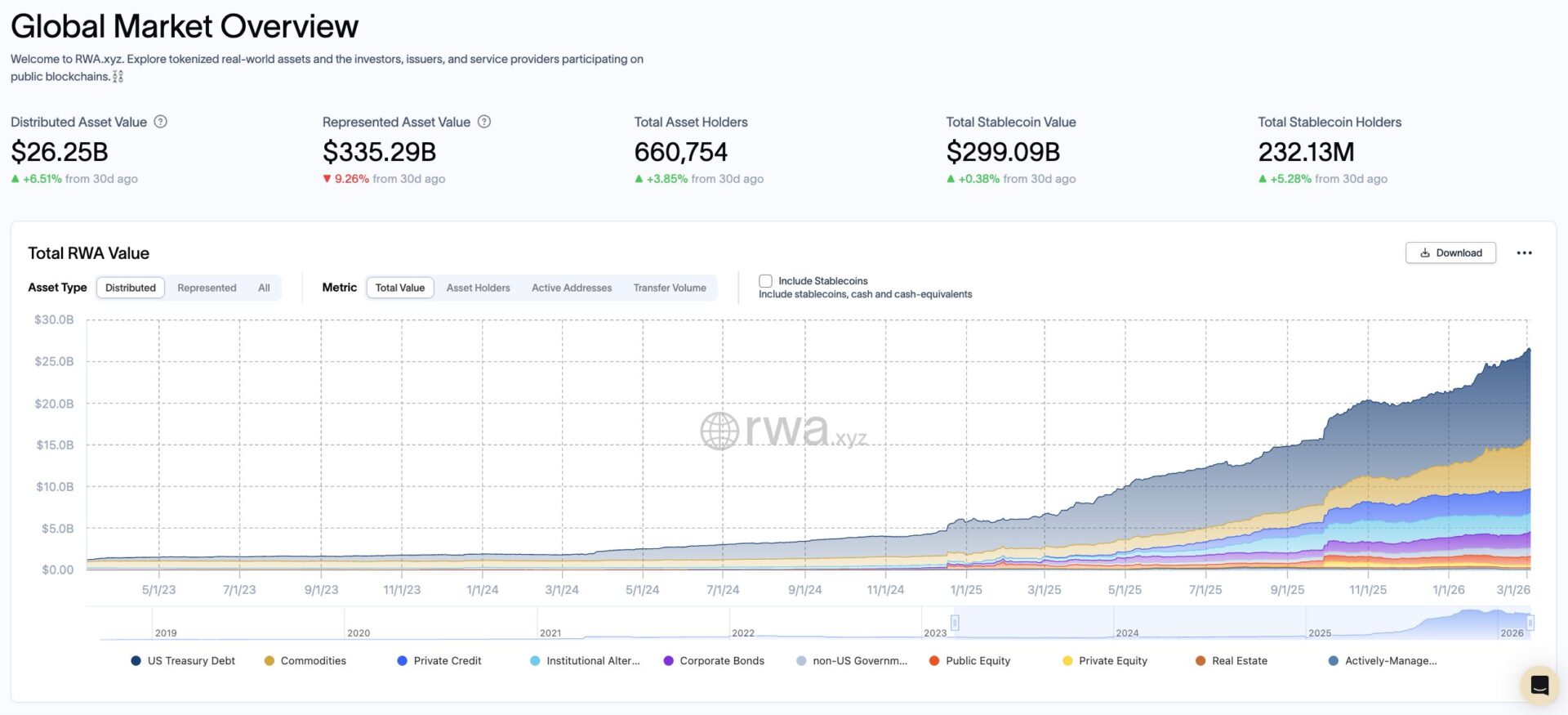

According to data from market research firm RWA.xyz, the global market for tokenized Real-World Assets (RWA) currently stands at approximately $26.25 billion. Tokenized U.S. Treasury products represent the largest segment of this market, while the tokenized stock market, valued at around $1.1 billion, is still in its nascent stages of development.

Financial professionals widely acknowledge the significant efficiency gains offered by tokenized securities, including 24/7 trading capabilities, instant settlement, and potentially lower transaction fees. Several trading platforms and FinTech companies in the European market have already launched tokenized stock products, enabling investors to trade tracking assets of traditional listed company shares via blockchain technology.

However, the integration of tokenized securities into the traditional financial ecosystem necessitates clear legal and regulatory alignment. The U.S. Securities and Exchange Commission (SEC) previously affirmed that tokenized securities fall under federal securities laws, mandating adherence to the same registration, disclosure, and investor protection requirements.

U.S. SEC Clarifies “Tokenized Securities” Regulations, Fully Included Under Securities Law Jurisdiction

A Maturing Regulatory Stance for Digital Assets

This joint statement from the Federal Reserve and other banking regulators serves as a pivotal indicator of the accelerating convergence between the traditional banking system and blockchain-based finance. For years, U.S. banking regulators maintained a cautious approach toward crypto assets and blockchain technology, leading to considerable uncertainty for financial institutions exploring related ventures.

As interest in tokenized assets continues to surge among financial institutions, regulators are progressively clarifying how existing financial statutes apply to blockchain-enabled assets. The fundamental importance of this capital rules clarification lies in its confirmation that tokenized securities will not incur additional capital burdens or face stricter regulatory scrutiny merely because of their technological format.

Market observers underscore the immense significance of this capital rules clarity for the banking sector. Capital adequacy ratios are a primary constraint influencing all bank business decisions. A well-defined regulatory framework empowers banks to more accurately assess the risks and costs associated with tokenized securities-related operations, fostering greater participation and innovation.

Tokenized securities are increasingly recognized as a crucial bridge connecting conventional finance with nascent blockchain markets. The future promises evolving collaboration models between banks, asset management firms, and crypto financial platforms, driven by the continuous refinement of relevant regulatory policies.

(The above content is an authorized excerpt and reproduction from our partner “CryptoCity”, original link.)

Disclaimer: This article is for market information purposes only. All content and views are for reference only, do not constitute investment advice, and do not represent the views and positions of BlockCast. Investors should make their own decisions and transactions. The author and BlockCast will not assume any responsibility for direct or indirect losses incurred by investors’ transactions.