Authored by Kyle Soska, Chief Investment Officer at Ramiel Capital

Translated and Edited by Felix, PANews

Unpacking Crypto Market Sentiment: What Ethena’s Data Reveals About Risk Appetite

With the cryptocurrency market enduring a prolonged “risk-off” period, Ramiel Capital’s CIO, Kyle Soska, has delved deep into market data, seeking crucial indicators of a potential shift. This comprehensive analysis explores the intricate market structure of perpetual futures and leverages insights from Ethena’s transparency dashboard to dissect prevailing market risk appetite.

Perpetual Futures: A Barometer for Crypto Risk

The cryptocurrency market has long been defined by its inherent volatility and traders’ propensity for high leverage. Among its many instruments, perpetual futures contracts have emerged as the dominant trading product, often seeing trading volumes soar to 5 to 20 times that of the underlying spot market. Given their central role in facilitating retail leverage, perpetual futures serve as a logical and potent barometer for gauging the broader crypto market’s risk appetite.

Ethena: Unlocking Insights into Derivatives

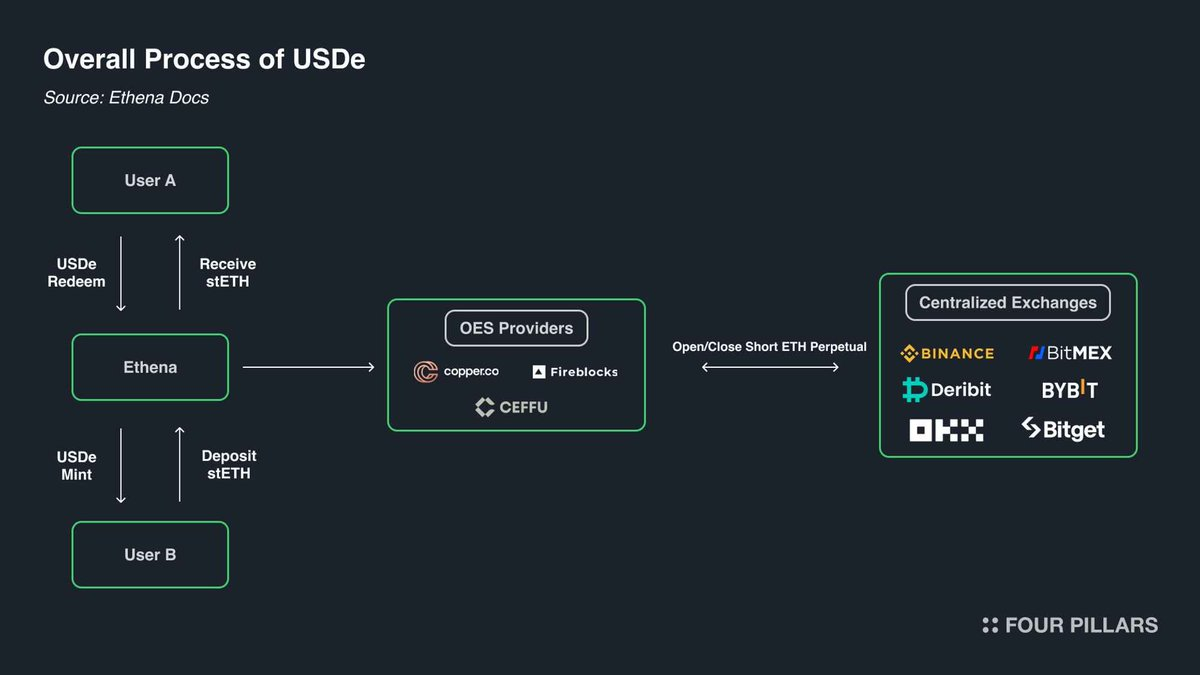

Ethena offers a uniquely transparent lens into the crypto derivatives landscape. As illustrated below, Ethena executes a sophisticated “crypto basis trade.” The mechanism is straightforward: when crypto traders establish long positions, Ethena steps in as the counterparty, taking an equivalent short position. Crucially, Ethena simultaneously purchases an equal amount of the underlying asset to perfectly hedge its short exposure.

Essentially, Ethena functions as a “leverage-as-a-service” provider. Traders seeking to capitalize on crypto’s upside, yet constrained by capital, can access funding from Ethena. In this symbiotic relationship, Ethena, possessing ample capital but a low-risk tolerance, lends this capital to traders through perpetual futures, with the cost structured around the “basis + funding rate.”

Understanding Perpetual Contract Dynamics

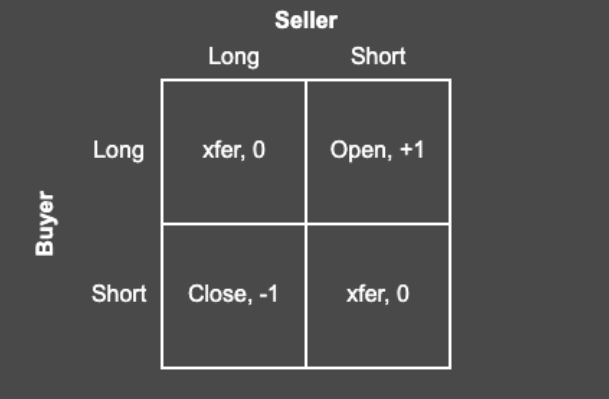

The fundamental architecture of perpetual futures dictates a precise 1:1 correspondence between every long and short position. Each open contract signifies a bilateral agreement, with exchanges playing a pivotal role in matching these contracts and ensuring both long and short holders are adequately collateralized. The following matrix outlines the four potential outcomes of contract matching facilitated by an exchange:

In any trade, there is always a buyer and a seller. When both parties to a contract are either simultaneously long or simultaneously short, the exchange merely transfers contract ownership, without altering the total number of outstanding contracts. However, when a buyer initiates a long position and a seller opens a short, a new contract is created, increasing the total open interest by one. Conversely, if a seller closes a long position and a buyer closes a short, the exchange effectively unwinds the contract, reducing the overall open interest by one.

The Four Pillars of Perpetual Contract Ownership

In a dynamic market, perpetual contracts are typically held by four distinct categories of participants:

- Directional Longs: These participants actively seek exposure to upward price movements, driven by their individual risk appetites and speculative convictions.

- Directional Shorts / Hedgers: This diverse group includes those anticipating price declines, as well as entities aiming to hedge existing asset holdings efficiently. This sub-category further divides into:

- Direct Asset Shorts / Hedges: Straightforward short positions or hedges against directly held assets.

- Structured Product Hedges: More complex strategies, often employed by venture capitalists (VCs) and token-compensated employees looking to hedge unlocking tokens at prevailing market prices. For illiquid altcoins, where direct hedging is unfeasible, firms like Cumberland, Wintermute, FalconX, Flowdesk, and Amber construct dynamically managed synthetic positions. These often involve shorting highly liquid assets like Bitcoin and Ethereum to offset exposure to less liquid markets such as Monad. Projects like Neutrl also offer such hedging as a yield-generating strategy.

- Basis Traders (e.g., Ethena): These are speculative short sellers who prioritize capturing yield from market imbalances rather than directional exposure. They strategically step in to meet excess long demand when it outstrips short supply, a common scenario in most market environments. Their positions are characterized by significant flexibility in scaling up or down.

- Perpetual Cross-Platform Arbitrageurs: These sophisticated players simultaneously hold long and short positions across different perpetual contract instruments. Their objective is to bridge minor price discrepancies between platforms, ensuring efficient market pricing within the bounds of trading fees. By design, their long positions are always perfectly matched by their short positions.

The Core Equation: Deconstructing Market Balance

Given the inherent 1:1 matching of long and short positions in every perpetual contract, we can establish a fundamental equilibrium:

Directional Longs + Arbitrage Longs = Directional Shorts + Basis Shorts + Arbitrage Shorts

Furthermore, by the very nature of perpetual arbitrage, we know that:

Arbitrage Longs = Arbitrage Shorts

By canceling out the arbitrage terms from the first equation, we arrive at a crucial insight:

Directional Longs = Directional Shorts + Basis Shorts

This simplified equation highlights Ethena’s significance: its reported basis short positions serve as a powerful proxy, offering unparalleled clarity into the dynamic interplay and net difference between directional long and short exposures in the market.

Ethena’s Balance Sheet: A Window into Market Shifts

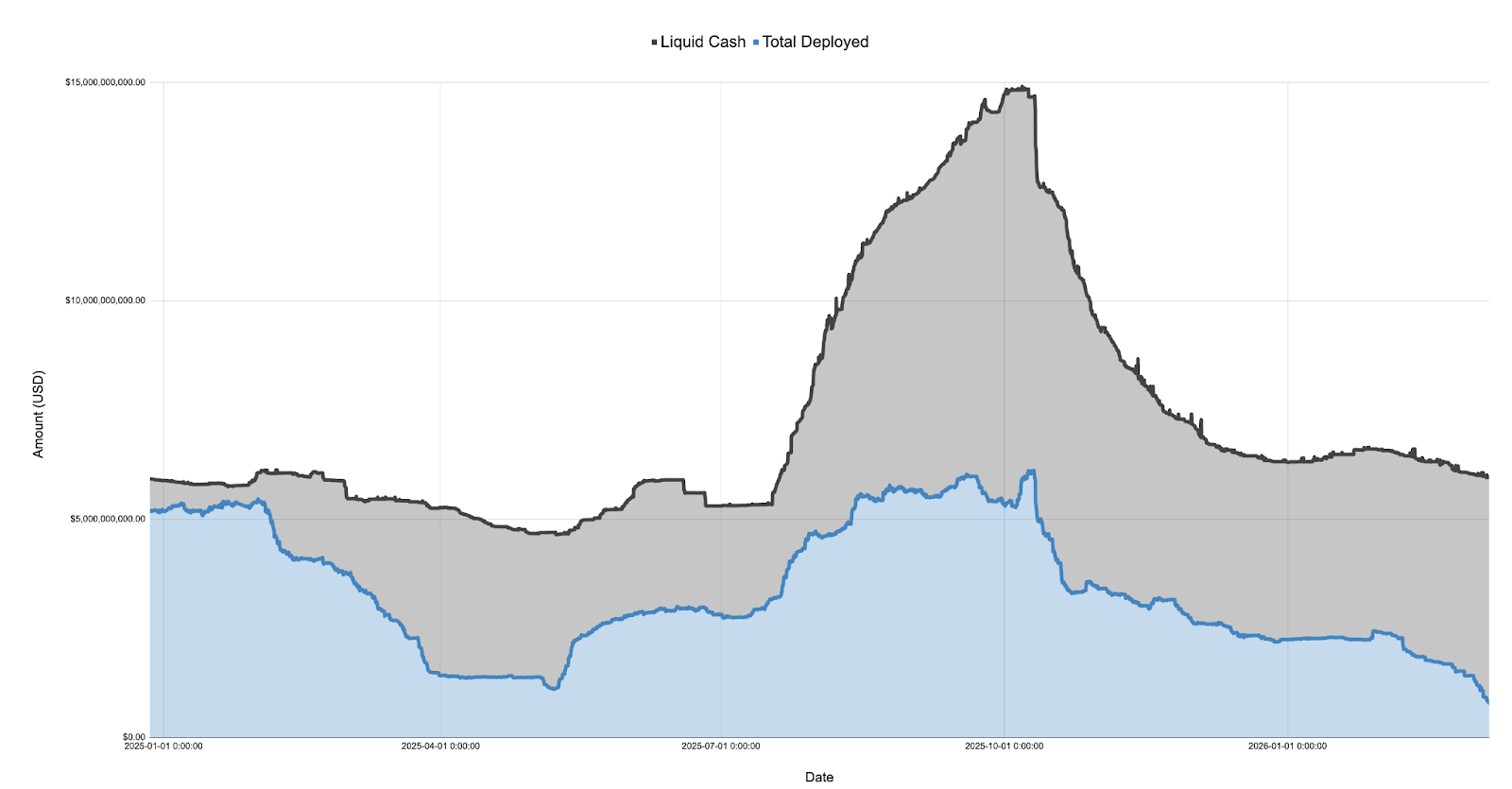

Ethena’s self-reported balance sheet, dissecting cash and deployed capital from December 27, 2024, to March 7, 2026, provides compelling evidence of market sentiment shifts:

Following the launch of the $TRUMP token in January 2025, the market experienced a dramatic shift towards risk aversion, a trend that persisted through April’s tariff discussions and the eventual “Liberation Day.” During this tumultuous period, Ethena’s deployed capital plummeted by over 75%, falling from more than $5 billion to a mere $1.108 billion.

It’s crucial to understand that Ethena’s deployed capital acts as a direct proxy for the market’s *excess* long demand. While Ethena is not the sole participant in basis trading, its substantial market presence—at times representing approximately 25% of Binance and Bybit’s activity—means it actively expands its book to fulfill any unmet long demand, provided it has surplus capital. This significant decline suggests that while overall long exposure demand might not have fallen by a full 75% in April 2025, the *excess* demand not absorbed by directional shorts certainly did.

Current Market Snapshot: A Historic Low in Net Long Demand

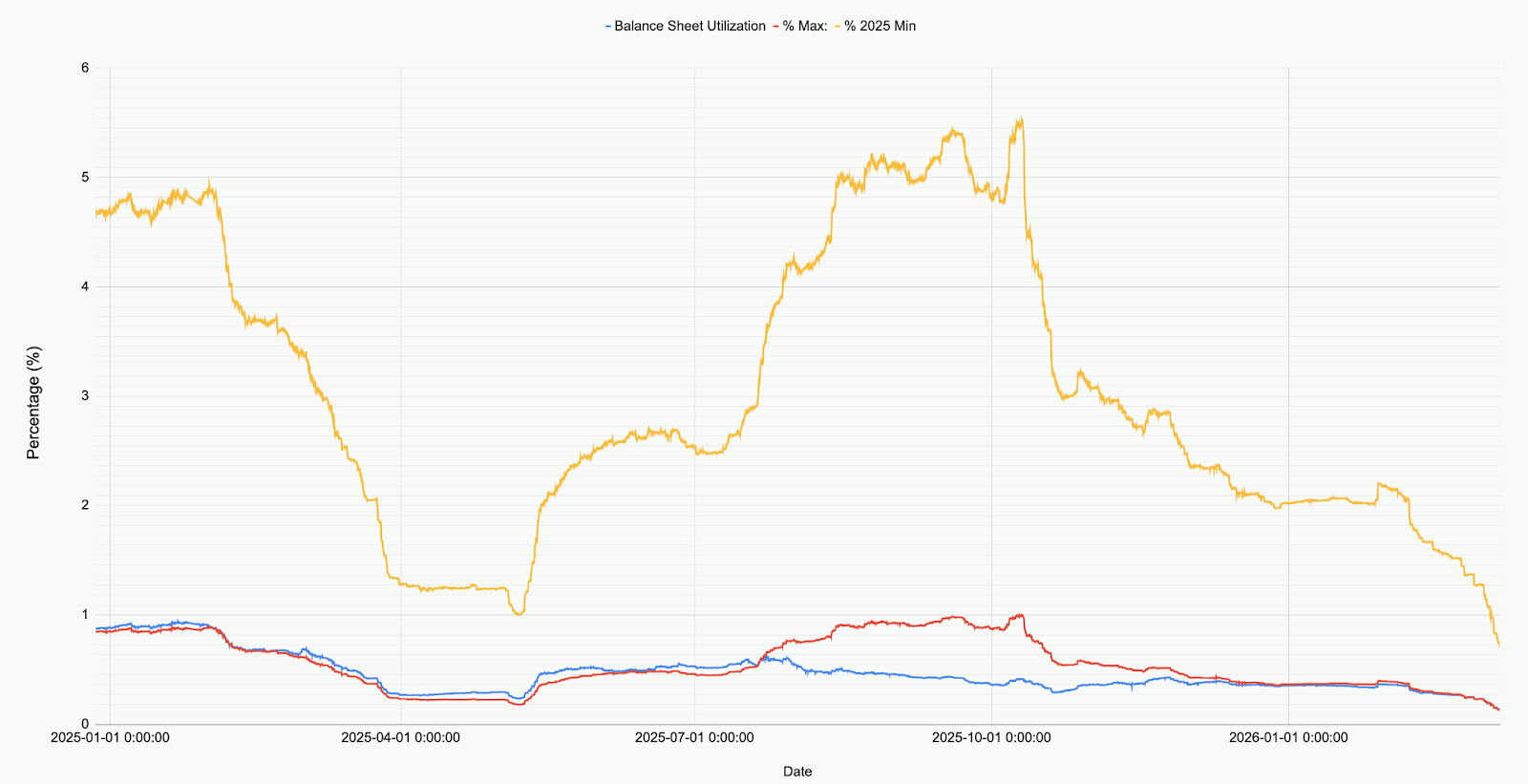

A closer look at Ethena’s balance sheet deployment, relative to its overall scale and historical highs and lows, paints a stark picture of current market sentiment:

Presently, Ethena’s total deployed capital across all supported markets (BTC, ETH, SOL, BNB, XRP, HYPE) stands at a modest $790 million ($791,241,545.6). This represents a mere 71% of its 2025 low and a striking 12.9% of its peak level recorded before October 10. This figure is not a critique of Ethena’s operations but rather a critical reflection of prevailing market conditions: net long demand has reached an unprecedented historical low.

Notably, Ethena’s deployed capital had surpassed $2 billion during the market downturn when Bitcoin’s price briefly dipped to $60,000. However, in the month since February 8, 2026, this deployed capital has witnessed an astonishing 60% collapse.

The Puzzling Contraction: Why Ethena’s Basis Positions Are Shrinking

Examining Ethena’s deployed capital alongside Bitcoin’s price trajectory since January reveals a significant divergence:

Following Bitcoin’s dip to $60,000, Ethena’s basis positions have contracted by over 60%, plummeting from more than $2 billion to less than $800 million. This sharp decline is particularly perplexing given the relatively stable market conditions observed during the same period. Several hypotheses attempt to explain this phenomenon:

- Unwinding of Unsustainable Trades: A gradual unwinding of basis trades initiated after the February crash, which, while initially profitable, became unsustainable as the basis moved into favorable negative territory, concurrently with negative funding rates.

- Increased Competition from Hedgers: Heightened competition from directional shorts and price-insensitive participants engaged in hedging activities, effectively squeezing out speculative basis traders like Ethena.

- Dwindling Leveraged Long Demand: A significant reduction in overall long demand specifically seeking leveraged exposure.

In my assessment, the observed contraction is predominantly a confluence of factors 1 and 2, with factor 3 playing a lesser role. As evidenced by the Coinglass data above, the overall open interest (OI) for Bitcoin and other major cryptocurrencies remained remarkably stable throughout Ethena’s unwinding phase. Concurrently, funding rates have lingered in negative territory for an extended period, with numerous altcoins like SOL registering accumulated negative funding rates across multiple exchanges. This pattern strongly suggests a surge in demand for directional shorting or sophisticated hedging strategies.

I contend that many smaller crypto firms and venture capitalists are currently navigating a period of significant stress. Consider the multitude of small-cap projects like Eigen, Grass, and Monad – each representing a complex ecosystem of dozens of VCs, a company with its treasury, and numerous employees. VCs are under pressure to mitigate losses and secure gains to meet their investment mandates, while companies are focused on safeguarding their cash flow and workforce. This environment fosters a “race to the bottom” where all parties strive to extract maximum value from finite resources, culminating in a highly concentrated trading strategy: shorting a diversified basket of related assets through actively managed structured products.

Evidence and Conclusion: An Unprecedented Market Balance

Further supporting this hypothesis, the day of Ethereum’s explosive rally saw numerous small and mid-cap crypto assets experience significant short-covering rallies, indicative of these underlying structured product hedges. The substantial squeeze out of speculative basis trades, as observed with Ethena, provides yet another layer of evidence.

Regardless of the precise causal mix, one fact remains unequivocally clear: for what appears to be the first time in its history, the cryptocurrency market is witnessing an almost perfect equilibrium between long and short positions. While there’s no inherent reason this couldn’t evolve into a new market normal, or that such a balance necessitates an immediate shift, it is a trend rarely sustained across other asset classes and traditional markets. This unprecedented equilibrium warrants close observation as the crypto landscape continues to evolve.

(This article is an authorized excerpt and reproduction from our partner PANews. Original Link)

Disclaimer: This article is provided for market information purposes only. All content and views are for reference and do not constitute investment advice, nor do they represent the opinions or positions of BlockBeats. Investors should exercise their own judgment and discretion in making investment decisions and trades. The author and BlockBeats shall not be held responsible for any direct or indirect losses incurred by investors as a result of their trading activities.