Author: Jae, PANews

DeFi’s Interest Rate Winter: A Structural Shift or Cyclical Downturn?

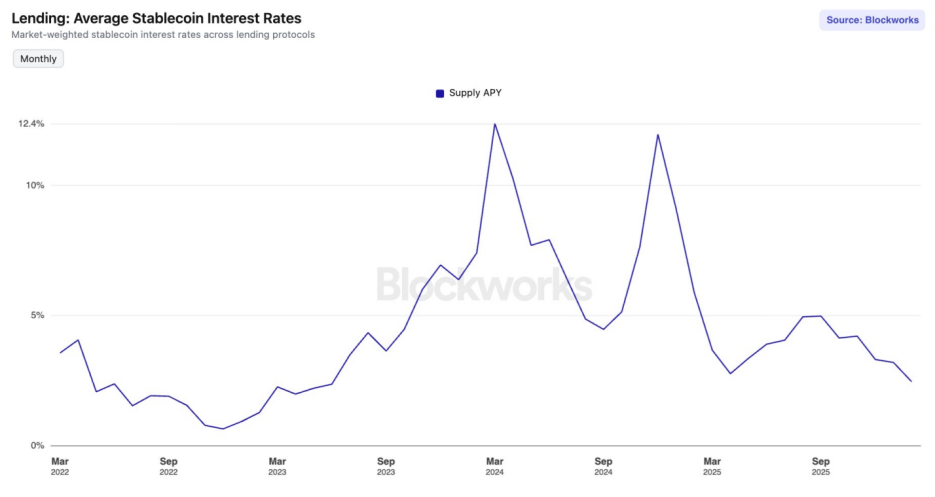

The subtle shifts in market indicators often herald the conclusion of a significant cycle. Since September 2023, the decentralized finance (DeFi) market has found itself in an “interest rate winter.” The average Annual Percentage Yield (APY) for major stablecoins across leading lending protocols has plummeted to its lowest point since June 2023. On Ethereum mainnet’s Aave V3, deposit rates for USDC and USDT have even dipped below 2%, a stark contrast to the U.S. 10-year Treasury yield, which has rebounded to 4.24%.

For seasoned DeFi participants who thrived during the “DeFi Summer” era of lucrative double-digit APYs, this isn’t merely a numerical decline; it echoes the somber tolling of a cycle’s end. The critical question now is: Are we witnessing a transient market fluctuation, or is the DeFi landscape undergoing a profound structural transformation?

Supply-Demand Imbalance: Liquidity Overload Drives Yield Collapse

Over the past six months, the interest rate curves within prominent lending protocols have exhibited a consistent downward trajectory, signaling a significant “supply exceeding demand” phenomenon that has triggered a widespread yield collapse.

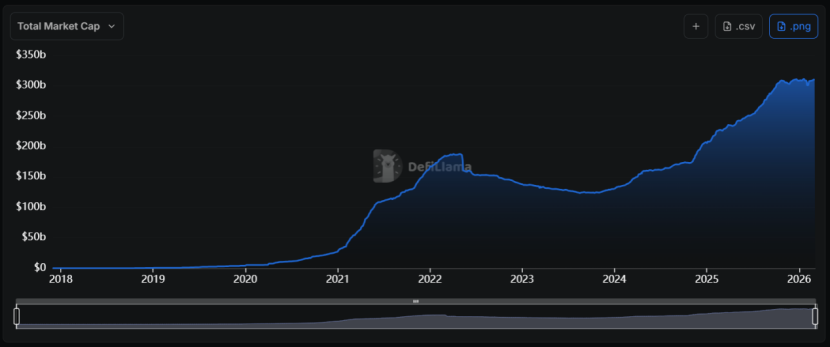

Interest rates fundamentally represent the price of capital, a price intrinsically determined by the available supply. Since the beginning of 2024, the stablecoin sector has experienced an unprecedented “expansion wave.” Its total market capitalization surged from under $130 billion to over $310 billion, boasting a remarkable compound annual growth rate of approximately 55%.

The core issue, however, lies in the fact that this dramatic surge in supply has not been matched by a proportional expansion in on-chain demand. When the market is saturated with a particular commodity—in this case, stablecoin liquidity—and demand simultaneously weakens, its price (the interest rate) is bound to fall. This is a foundational principle of economics, and DeFi markets are not immune.

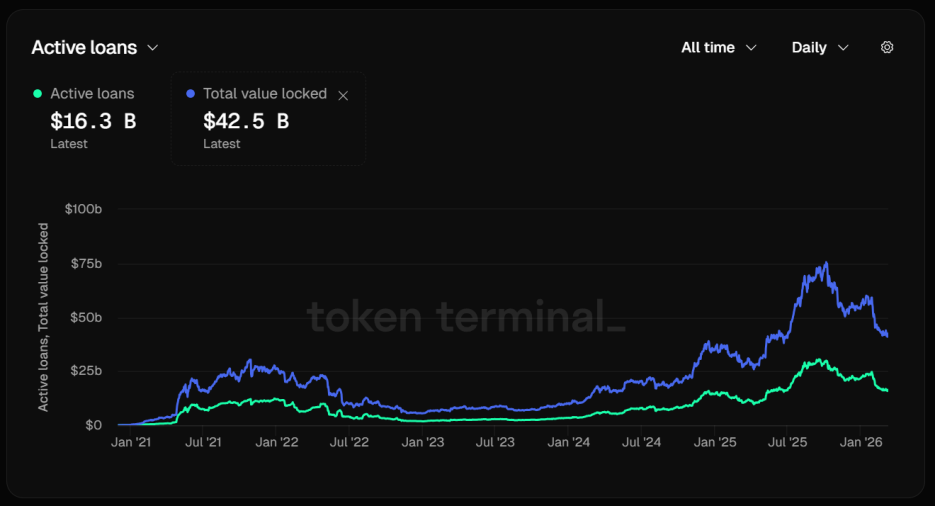

Consider Aave, a dominant force in the lending space. Its stablecoin utilization rate has witnessed a significant decline. As of March 12, Aave’s Total Value Locked (TVL) stood at an impressive $42.5 billion. Yet, a closer examination of its capital structure reveals a concerning detail: active loans amounted to only $16.3 billion. This means over 60% of deposited assets are lying idle, creating a severe supply-demand imbalance that has directly contributed to the rapid erosion of interest rates.

Essentially, funds are being deposited but not borrowed, leading to an acute stagnation of liquidity. Consequently, the protocol’s algorithms are compelled to automatically lower interest rate curves in an attempt to attract more borrowers.

Despite these efforts, the impact has been minimal. The benchmark rates for USDC and USDT on Aave V3’s Ethereum mainnet have already fallen below 2%, a stark and uncomfortable contrast to the double-digit returns that were commonplace during the bull market. The stablecoin market has effectively fallen into a “liquidity trap,” where an abundance of low-cost capital exists, but a scarcity of high-return investment opportunities causes these funds to accumulate passively within lending protocol pools.

Funding Rate Collapse & Deleveraging: The Cooling of Arbitrage and Circular Lending

Historically, the vibrancy of DeFi stablecoin interest rates was intrinsically linked to leverage. A slowdown in arbitrage activities within the perpetual futures market invariably leads to a rapid contraction in stablecoin borrowing demand, precipitating a sharp decline in interest rates.

During bull markets, heightened bullish sentiment often drives funding rates positive and high. This environment encourages arbitrageurs to execute Delta-neutral strategies—borrowing stablecoins to purchase spot assets while simultaneously shorting perpetual futures—to earn risk-free funding fees. In this mechanism, stablecoins serve as the essential fuel.

However, the derivatives market has recently exhibited a downturn. On major centralized exchanges (CEXs), Bitcoin (BTC) and Ethereum (ETH) funding rates have frequently registered negative or extremely low positive values. This trend suggests either a dominance of bearish sentiment or an extreme level of caution among bullish traders.

Both interpretations converge on the same conclusion: a significant lack of motivation for arbitrageurs. When annualized funding rates plummet, and factoring in borrowing costs and transaction fees, the net profits for arbitrageurs diminish substantially. This directly translates to a precipitous drop in their demand for stablecoin borrowing.

Another significant driver of stablecoin borrowing demand has been circular lending, a yield-enhancement strategy. A typical pathway involves depositing yield-bearing assets like sUSDe into Aave, borrowing stablecoins such as USDC, and then converting the borrowed USDC into more sUSDe for redeposit. This strategy was once highly lucrative, with USDe yields soaring to 30% while borrowing costs hovered around 10%, creating a substantial 20-percentage-point arbitrage spread.

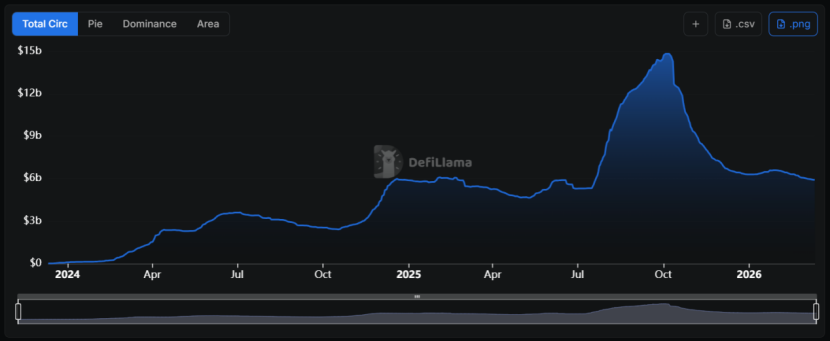

However, following the “1011” event, this interest rate spread experienced a disastrous narrowing. Concurrently, USDe encountered its “scalability” ceiling, with its market size declining sharply from nearly $15 billion to approximately $6 billion today.

USDe’s yield is heavily reliant on the volume of short positions in the market. Given the finite nature of Open Interest in the perpetual futures market, as USDe’s scale expands, the very short positions required for its hedging mechanism begin to depress overall market funding rates, thereby suppressing sUSDe’s yield. For everyday traders, a reduction in sUSDe’s yield translates to a narrower strategy spread. Their decreased appetite for leveraged positions further reduces the demand for stablecoin collateral.

This creates a self-reinforcing negative feedback loop: shrinking demand leads to lower interest rates, which in turn leads to further demand contraction.

Shifting Risk Appetite: The Flight to Certainty in Crypto

A broader decline in the crypto market’s overall risk appetite represents another crucial factor contributing to the downward pressure on stablecoin interest rates.

Over the past month, the Crypto Fear & Greed Index has repeatedly dipped into the “extreme fear” territory. Even with Bitcoin (BTC) prices holding above $70,000, there has been no sustained improvement in market sentiment.

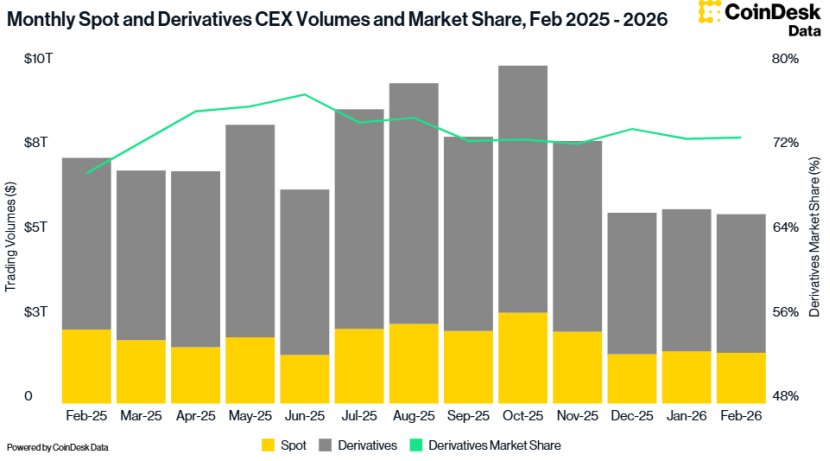

Data from CoinDesk further illustrates this trend, showing that total trading volume on centralized exchanges (CEXs) in February declined by 2.41% to $5.61 trillion—the lowest volume recorded since October 2024.

This discernible shift towards lower risk appetite is compelling investors to reallocate capital into segments offering greater certainty.

Since January 2024, the Federal Reserve’s effective federal funds rate has consistently remained above 3.6%. While market expectations lean towards a moderate path of future rate cuts, the current actual interest rate remains relatively elevated.

This prevailing macroeconomic environment exerts significant downward pressure on DeFi stablecoin interest rates. When the yield on risk-free U.S. Treasury bonds surpasses DeFi deposit rates, and without adequate risk premium compensation, rational investors are naturally inclined to withdraw funds from on-chain protocols or deploy them into Real World Asset (RWA)-backed protocols.

However, not all protocols are contracting in this “interest rate winter.” Sky (formerly MakerDAO) has strategically constructed a unique “yield moat.” Unlike Aave, which primarily relies on on-chain lending demand, Sky generates yield from a substantial $1.5 billion portfolio of mature RWA assets. These assets, including U.S. Treasury bonds and AAA-rated corporate debt, are insulated from crypto market volatility, providing a stable foundation of underlying cash flow.

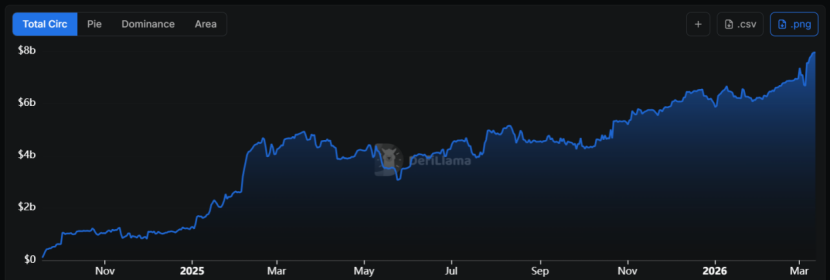

This innovative model, which leverages RWA as underlying collateral, has propelled the monthly supply of USDS to grow by 68% annually, with its market capitalization approaching $8 billion.

Currently, the sUSDS interest rate remains steadfast at around 3.75%, effectively establishing a “de facto floor” for on-chain yields. Furthermore, within USDC and USDT-related vaults, deposit rates can exceed 5%.

This positions Sky to act as a “benchmark interest rate platform.” In comparison, the rates offered for similar assets on Aave appear significantly less competitive. Thus, Sky is evolving beyond a mere stablecoin protocol into a sophisticated “fixed-income asset management” protocol. It adeptly utilizes its extensive RWA portfolio to hedge against the inherent downside risks of the crypto market, enabling it to source yield externally from traditional financial markets when internal DeFi demand is lacking.

For investors, a crucial lesson in this cycle will be to scrutinize the underlying asset logic behind yields—differentiating between dividends from government bonds and volatility premiums from futures markets. Investment strategies must shift from simply “chasing APY” to actively “seeking differentiated risk exposure.”

The “interest rate winter” is not solely a product of cyclical fluctuations; it is also a necessary, albeit painful, phase of “bubble dehydration” for DeFi. Perhaps, much like the downturn of 2023 laid the groundwork for the prosperity of 2024, this current bottoming out of interest rates is DeFi’s way of accumulating energy for its next significant leap.

(The above content is an excerpt and reproduction authorized by partner PANews. Original Link)

Disclaimer: This article is for market information purposes only. All content and views are for reference only and do not constitute investment advice, nor do they represent the views and positions of BlockTempo. Investors should make their own decisions and trades. The author and BlockTempo will not be liable for any direct or indirect losses incurred by investors as a result of their trading.