Author: Nancy, PANews

Backpack’s TGE Sparks “Witch Hunt” Outcry, Leaving Community Trust Shaken

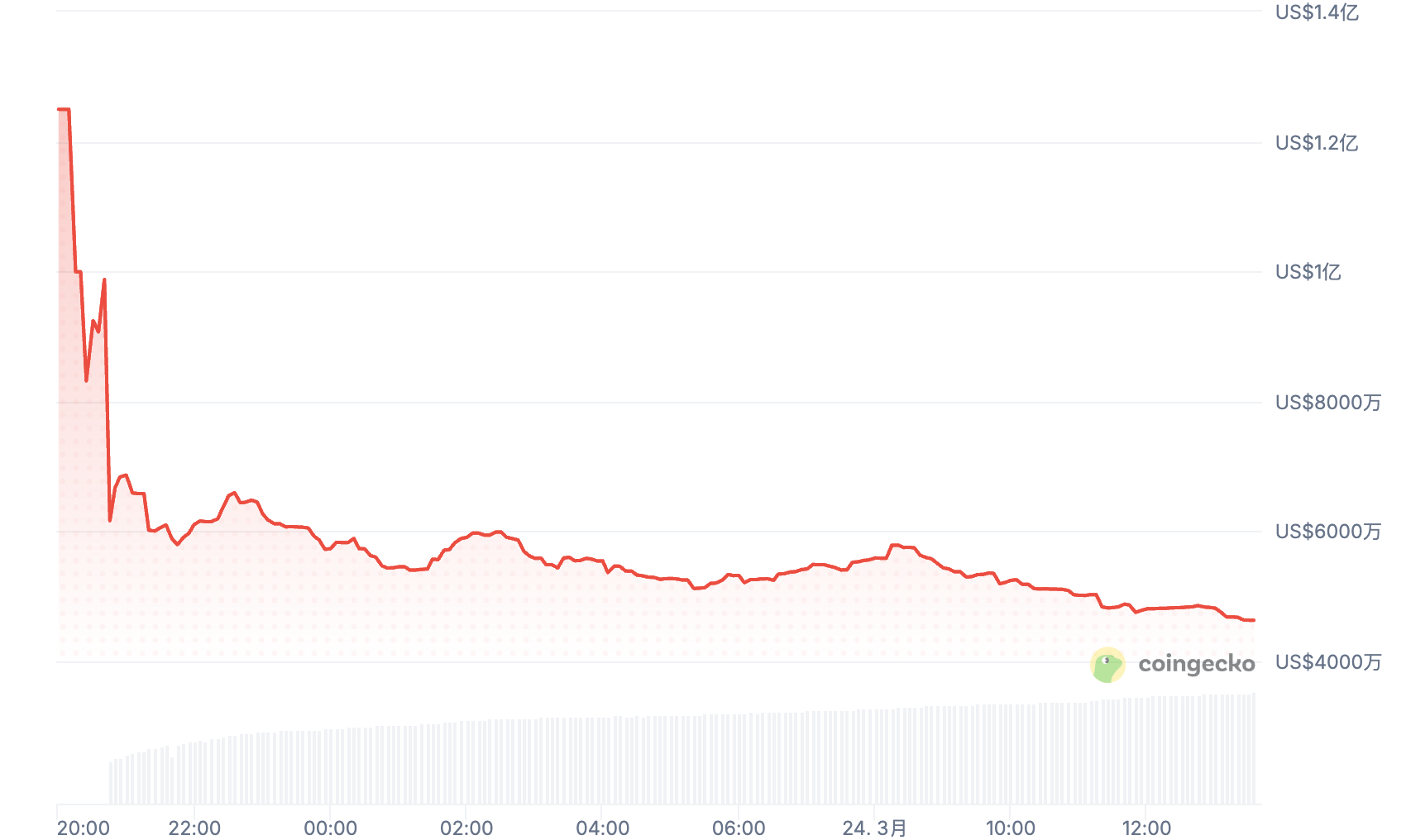

After three years of anticipation, the launch of Backpack’s native token, BP, was met not with celebration, but with a storm of controversy. On March 23rd, the highly-anticipated Token Generation Event (TGE) for the Backpack trading platform unfolded amidst a challenging market, failing to deliver the expected uplift. The token’s price plummeted post-launch, settling at a fully diluted market capitalization of under $200 million. However, the true shockwave through the community stemmed from widespread accusations of a “witch hunt” – a mass disqualification of users from airdrop rewards. Long-standing participants, from small-scale interactors to high-volume traders, found their efforts invalidated, labeled as ‘witches’ without clear criteria. This unilateral enforcement of undisclosed rules ignited a severe trust crisis, compelling Backpack to hastily establish an appeal process on March 24th.

The sentiment echoes a bitter truth: “In a bull market, you farm others; in a bear market, you farm the project.” This recent trend, following similar disappointments from Opinion and Backpack, signals a potential turning point, if not an end, for the once-lucrative airdrop farming ecosystem, leading some seasoned participants to declare their withdrawal.

KOLs Caught in the Crossfire: Chinese Community Hit Hardest by “Anti-Farming”

The promise of “pure community allocation” ultimately devolved into a large-scale “anti-farming” event. Yesterday, Backpack finally opened the token claim portal for BP. According to previous official announcements, 25% of the total token supply (approximately 250 million BP) in this TGE was designated entirely for community distribution, with 24% allocated to points holders and 1% to Mad Lads NFT holders. The official statement emphasized that this portion of tokens belonged exclusively to the community, with no team or investor shares participating in the initial circulation.

However, the opening of the claim portal delivered a heavy blow to many users. A significant number discovered their accumulated points had been drastically reduced, or even wiped out, leaving them with only symbolic participation rewards, or nothing at all. What exacerbated the dissatisfaction was that many of these disqualified users were not peripheral accounts, but core participants: long-term active single-wallet users, high-point farmers, and Mad Lads NFT holders.

Anger quickly spread through the community, with Chinese users particularly affected by this “witch cleansing.” Numerous complaints from prominent traders and Key Opinion Leaders (KOLs) flooded social media: “4 billion USD in trading volume, 100% witch rate,” “Over 1.5 billion USD in trading volume, 800+ hours spent, over $300,000 in fees, only half the expected airdrop,” “330,000 points yielded only 2,000 tokens,” “Ranked first in total network trading volume, received only 20,000 tokens from 170,000 points.” These figures represent substantial capital investment and time commitment, yet in the final distribution, these users were collectively categorized as “witches” and disqualified.

The frustration was amplified not just by the loss of potential earnings, but by the perceived invalidation of their contributions. Many of these users had maintained long-term communication with the project team, consistently produced content endorsing the project, and actively participated in community growth and ecosystem expansion. These efforts, however, were not factored into any weighting and were ultimately disregarded.

Even more contentious was the “guilt by association” approach. Some community leaders, responsible for growth and expanding the ecosystem, found themselves not only purged but also saw the legitimate users they invited affected. This punitive mechanism turned the very growth logic, reliant on social propagation, into a source of risk.

Compounding the issue, the rapid decline of the BP token immediately after its listing further amplified overall losses and intensified negative market sentiment.

At the heart of all these disputes lies Backpack’s lack of transparency regarding its rules.

Backpack’s “witch identification” criteria were never publicly disclosed, yet its risk control mechanisms were continuously upgraded. Just before the TGE, Backpack not only mandated KYC for all accounts participating in points activities but also conducted a large-scale audit, citing reasons to “purify the environment and reward real users.” This process reportedly identified over 50 million points from “non-genuine behavior,” which were then reclaimed and reallocated. However, for users, clear answers on what constituted “non-genuine behavior,” the basis for judgment, or its boundaries remained elusive.

Can Returning Points and Token Compensation Rebuild Trust?

Under immense public pressure, Backpack quickly moved to address the crisis.

Claire, a Backpack team member, tweeted that the Backpack Chinese team engaged in intense discussions with the Western team overnight. The Chinese team expressed its reluctance to see the interests of its supportive users compromised and held in-depth talks with the anti-witch负责人 (person in charge of anti-witch activities).

As an experienced compliance professional, Claire stated that for the anti-witch team, “one person, one account” is an absolute baseline. Under this standard, a disproportionately higher number of Chinese users were affected compared to other regions, a consequence of differing user habits. Western users’ strict adherence to rules and sensitivity to KYC information meant that multi-account behavior itself was often outside their understanding. In subsequent actions, Backpack founder Armani and the core team prepared to immediately open an appeal channel, establishing clear rules to protect user interests to the maximum extent.

Subsequently, Backpack’s Chinese account announced the activation of a manual appeal channel, allowing users to submit data for review. It also declared adherence to a “3-account rule”: if an account operating on the same device (up to 3 accounts) was deemed a witch, and subsequently verified through manual appeal, over 50% of their points would be returned. Furthermore, the Backpack team plans to initiate a project buyback program in the coming days, repurchasing tokens from the secondary market for targeted compensation to eligible users.

However, for those users who had invested fully, these remedies might mitigate some losses, but trust, once broken, is notoriously difficult to rebuild.

Equity for a Year-Long Lock-up? Backpack Bets on an IPO Narrative

Historically, most crypto projects tend to experience a post-launch pump-and-dump, often fading into obscurity. Against the backdrop of a crypto bear market, Backpack chose to pivot towards an IPO narrative even before its official token launch, aiming to bolster market confidence.

In February, Backpack CEO Armani Ferrante stated that a core principle of the company’s token economic model is to prevent insiders from dumping on retail investors. No founder, executive, employee, or venture capitalist should accrue wealth through tokens before the product achieves “escape velocity.” For Backpack, the answer to “escape velocity” is clear: the company plans to pursue an IPO in the United States.

This strategy implies that the token’s value capture will be re-anchored and closely tied to the company’s overall valuation. At this juncture, Axios recently reported that Backpack is in talks for a new funding round, aiming to raise $50 million at a pre-money valuation of $1 billion, according to informed sources.

Backpack has also demonstrated “sincerity” in its token unlock schedule. While 37.5% of tokens will gradually unlock before the IPO based on key milestones, an additional 37.5% will be held in the company treasury and locked until at least one year post-IPO. Team members, in this model, will solely hold company equity.

Furthermore, Backpack announced that it would allocate 20% of its company equity, offering users who stake BP tokens for at least one year the opportunity to convert their tokens into company equity at a fixed ratio. Recently, Backpack also launched an on-chain IPO new share allocation feature, allowing users to directly acquire IPO shares through the platform and open a waitlist registration.

However, the specific details of the token-to-equity conversion remain undisclosed, including the conversion format, scope of rights, and timeline. This has sparked community concerns that it might be another round of “PUA” (pickup artist tactics – implying manipulation), locking users’ assets first and then slowly fulfilling promises, using equity conversion to buy the project more time for survival.

Armani Ferrante himself has revealed that the IPO “might happen soon, or it might not be so soon, or it might not happen at all. But regardless, he and the team will give it their all.”

Disclaimer: This article provides market information only. All content and opinions are for reference purposes only and do not constitute investment advice, nor do they represent the views and positions of BlockTempo. Investors should make their own decisions and trades. The author and BlockTempo will not bear any responsibility for direct or indirect losses incurred by investors’ transactions.