Navigating the Crypto Winter: Unearthing Resilience in a Market Downturn

Six months ago, investors captivated by the promise of a crypto “supercycle” could scarcely have imagined the dramatic turn of events. Bitcoin, once soaring, has since plummeted by nearly half, falling from a peak of $125,000 on October 6, 2025, to its current $66,600 – a staggering 46.56% decline. This isn’t merely a market correction; it’s a systemic cleansing, a brutal stress test for the entire digital asset ecosystem.

PANews conducted an extensive analysis, pulling price data for all 424 USDT spot trading pairs on Binance, revealing a stark reality:

* Only 11 assets (2.6%) recorded positive returns over this six-month period.

* A staggering 405 assets (95.5%) experienced maximum drawdowns exceeding 50%.

* Even when broadening the criteria to “outperforming BTC,” only 50 assets managed to do so, meaning 88% of altcoins underperformed the broader market.

* Among 45 key projects across 8 major sectors, only Maker posted a positive return.

This is a harsh report card. However, the purpose of this analysis isn’t to dwell on the wounds, but rather to identify the vital signs amidst the wreckage. As the tide recedes and bubbles burst, assets that continue to generate profit, public chains that attract capital, and ecosystems that sustain user growth emerge as the most precious signals in the market. PANews leverages comprehensive Binance spot data, on-chain metrics from 12 major public chains, and price performance of 45 representative projects across 8 sectors to pinpoint these “signs of life” in the crypto landscape.

(Analysis Scope: The research period spans from October 6, 2025, to March 30, 2026. The 424 Binance spot pairs represent valid samples after de-duplication and exclusion of stablecoins, fiat-pegged tokens, and leveraged tokens. On-chain data is sourced from DefiLlama, growthepie, and Token Terminal. Sector project prices are taken from Binance and CoinGecko.)

I. The 10 Survivors Among 424 Assets: Three Distinct Species Emerge

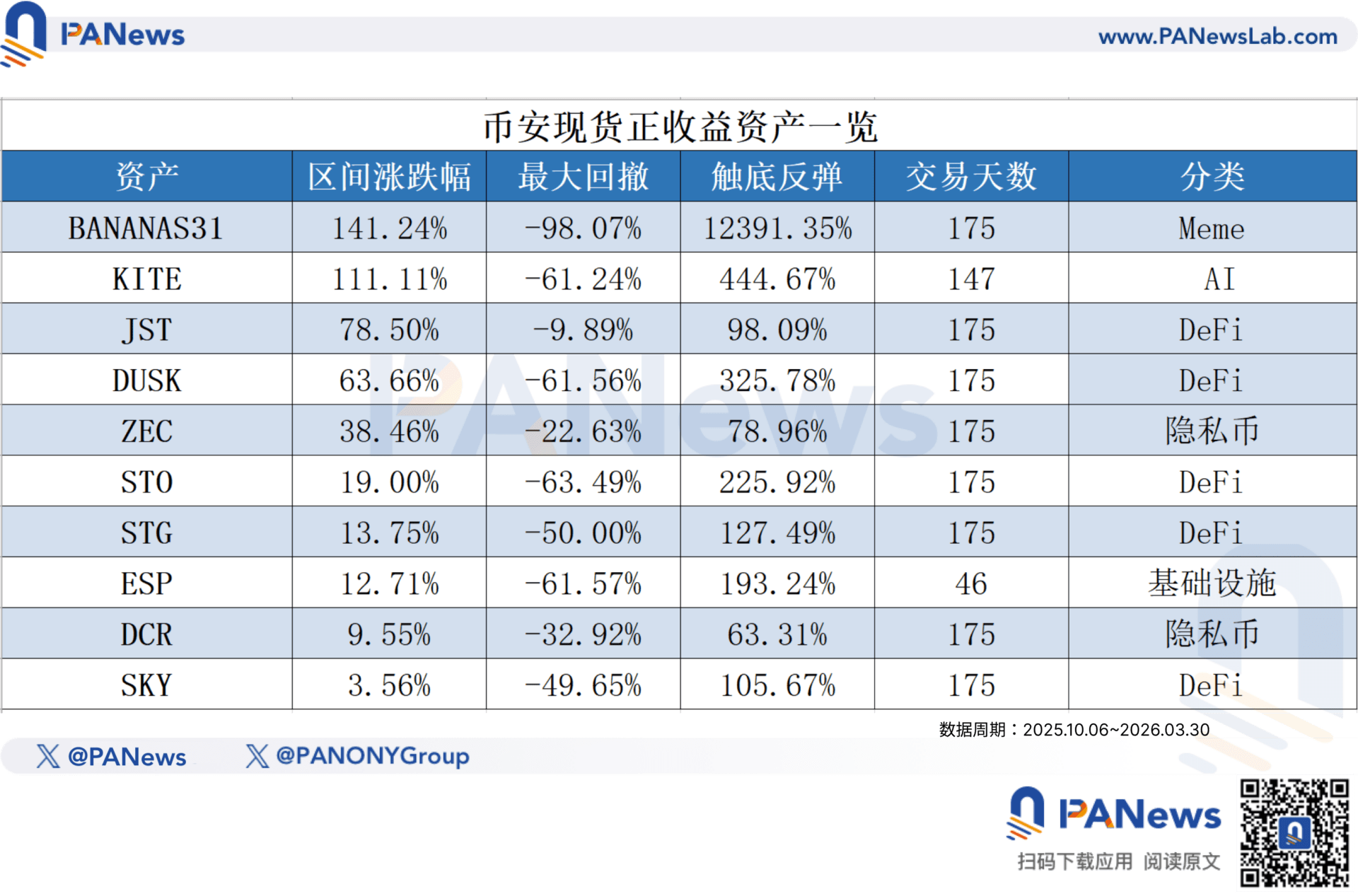

Let’s first examine the full list of assets that managed to record positive returns during a six-month period where Bitcoin was halved and the broader market bled red:

At first glance, gains like BANANAS31’s 141% and KITE’s 111% seem impressive. However, a closer look reveals that these 11 “survivors” belong to three entirely different categories.

**The First Category: True Resilience** – JST, ZEC, and DCR exemplify genuine strength.

JST stands out with a 78.5% gain and a maximum drawdown of only 9.89%, making it the sole positive-return asset with a drawdown below 10% across the entire market. While 95% of assets saw pullbacks exceeding 50%, JST surged against the tide. The core reason lies in JustLend DAO’s “JST Repurchase and Burn Proposal,” officially launched on October 11. This proposal transparently utilizes DeFi income from the JustLend protocol to repurchase and permanently burn JST on-chain, creating continuous deflation. This measure demonstrated fundamental resilience amidst market panic and liquidations, swiftly attracting capital inflows and driving price recovery.

ZEC and DCR, on the other hand, represent a different logic: the safe-haven effect of privacy coins in a bear market. ZEC’s maximum drawdown was 22.63%, and DCR’s was 32.92%, showcasing rare resilience in a landscape of widespread collapse. The ability of these established privacy coins to hold their ground stems not just from their narrative, but from a long-standing community base and sustained demand for anonymous transactions.

Additionally, STG (Stargate, a cross-chain bridge protocol) rose 13.75%, and SKY (MakerDAO’s rebranded governance token) gained 3.56%. Both fall under DeFi infrastructure. Cross-chain bridges address a critical need in a weak market (users need to transfer funds across chains for risk mitigation), while stablecoin governance protocols benefit from consistent protocol revenue, mirroring JST’s underlying logic.

**The Second Category: Phoenix from the Ashes** – BANANAS31, DEXE, and others. These assets share a common characteristic: extremely deep maximum drawdowns (87% to 98%), followed by bounces of hundreds or even thousands of percentage points from their lowest points. BANANAS31, for instance, experienced a maximum drawdown of 98.07%, then rebounded 12,391% from its bottom, appearing to have surged 124x. However, this is primarily due to an extreme price drop on October 11, where even minimal buying volume could trigger massive percentage rebounds, turning them into playgrounds for opportunistic manipulators.

**The Third Category: Newly Listed Tokens** – KITE has only 147 days of trading history, and ESP only 46 days. Their high gains largely reflect post-listing performance and haven’t fully endured the bear market’s scrutiny.

Stripping away these confounding factors, the true “winter survivors” list narrows down to JST, ZEC, DCR, STG, and SKY. These five assets endured the full six-month cycle with controlled drawdowns and authentic gains. A clear common thread unites them: either they possess real on-chain use cases (lending, cross-chain bridging, stablecoins) or they benefit from a long-standing community foundation (privacy coins). This is the first sign of life: in the crypto world, “utility” outlives “fame.”

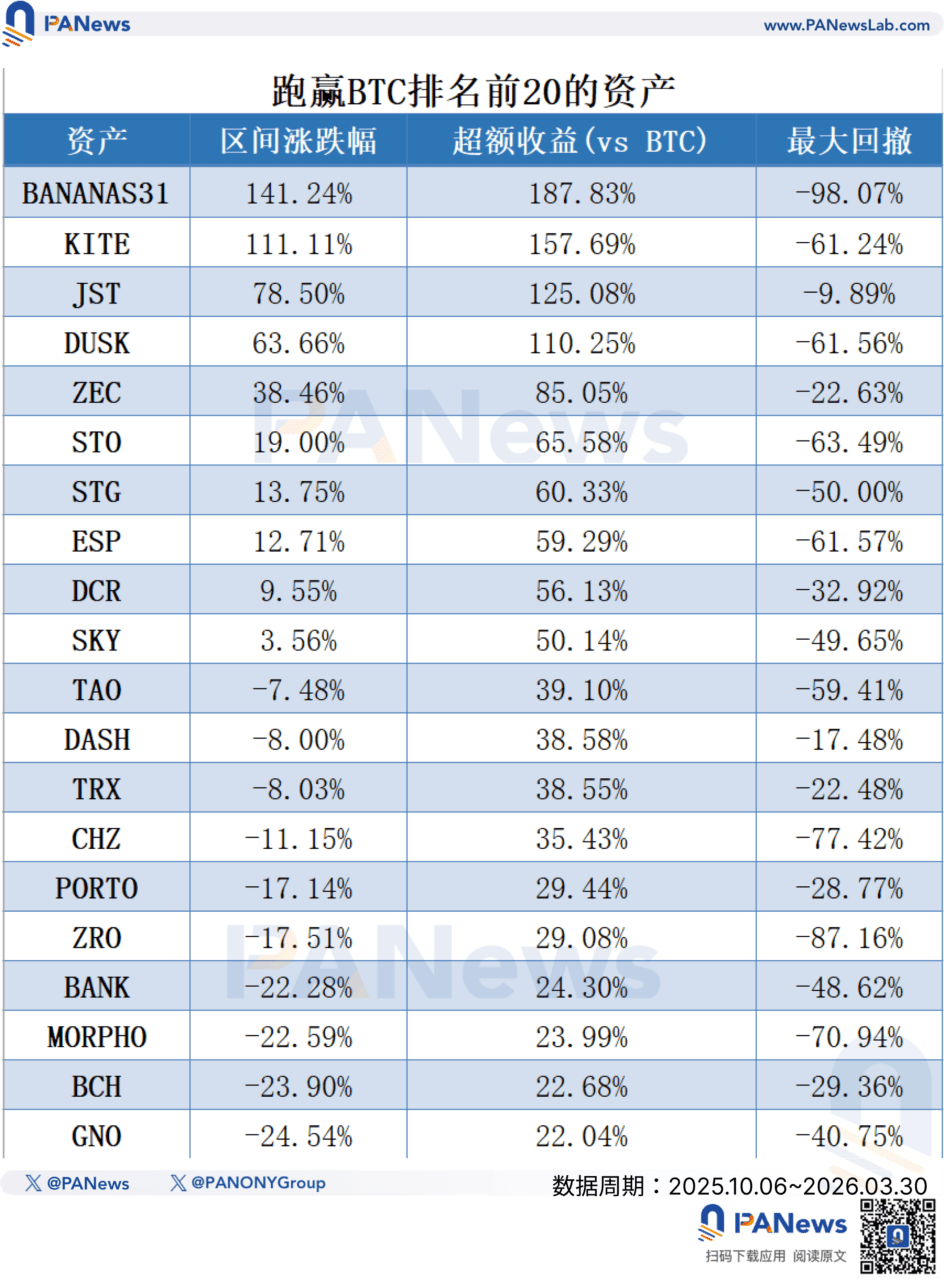

II. Tracing Clues Among the 50 Assets That Outperformed BTC

While BTC itself fell 46.56%, most of the 50 assets that “outperformed” it don’t necessarily signify “good performance,” but rather a relatively smaller decline. Beyond the 11 positive-return assets, 14 saw declines between 0% and 30%, and 25 fell between 30% and 46%. The remaining 374 assets, representing 88% of the total, underperformed the market.

Within these 50 names, several clues are worth tracking:

**TRX (down 8.03%)** is the native token of the Tron public chain. Combined with JST’s performance in the previous section, a clear picture emerges: the Tron ecosystem has demonstrated overall resilience during this bear market. With single-digit token declines and positive returns from DeFi projects within its ecosystem, the underlying support is the genuine demand for stablecoin settlement. Tron facilitates the largest share of USDT circulation across the entire network, and its position as a settlement layer has not only remained unshaken but has become more solidified in a weak market.

**TAO (down 7.48%)** is Bittensor, the only project in the AI sector with a single-digit decline. Against a backdrop where AI Agent concept coins collectively halved or even went to zero, TAO’s resilience suggests the market is distinguishing between “AI narratives” and “AI infrastructure.” Projects with actual decentralized computing networks in operation have maintained their pricing logic.

**VIRTUAL (down 44.32%)** saw a relatively controlled decline in an AI Agent sector where most projects fell 70% to 90%. However, looking at its actual chart movement, it appears to have started falling even before the October 11 crash and is currently still consolidating at low levels.

With 88% of altcoins underperforming BTC, the remaining 12% offer faint glimmers of survival. The strength of the Tron ecosystem is underpinned by stablecoin settlement demand, the fundamental value of AI computing networks represented by Bittensor, and the essential needs served by some large DeFi infrastructure. These subtle clues all point in the same direction: **real utility, not just narrative.**

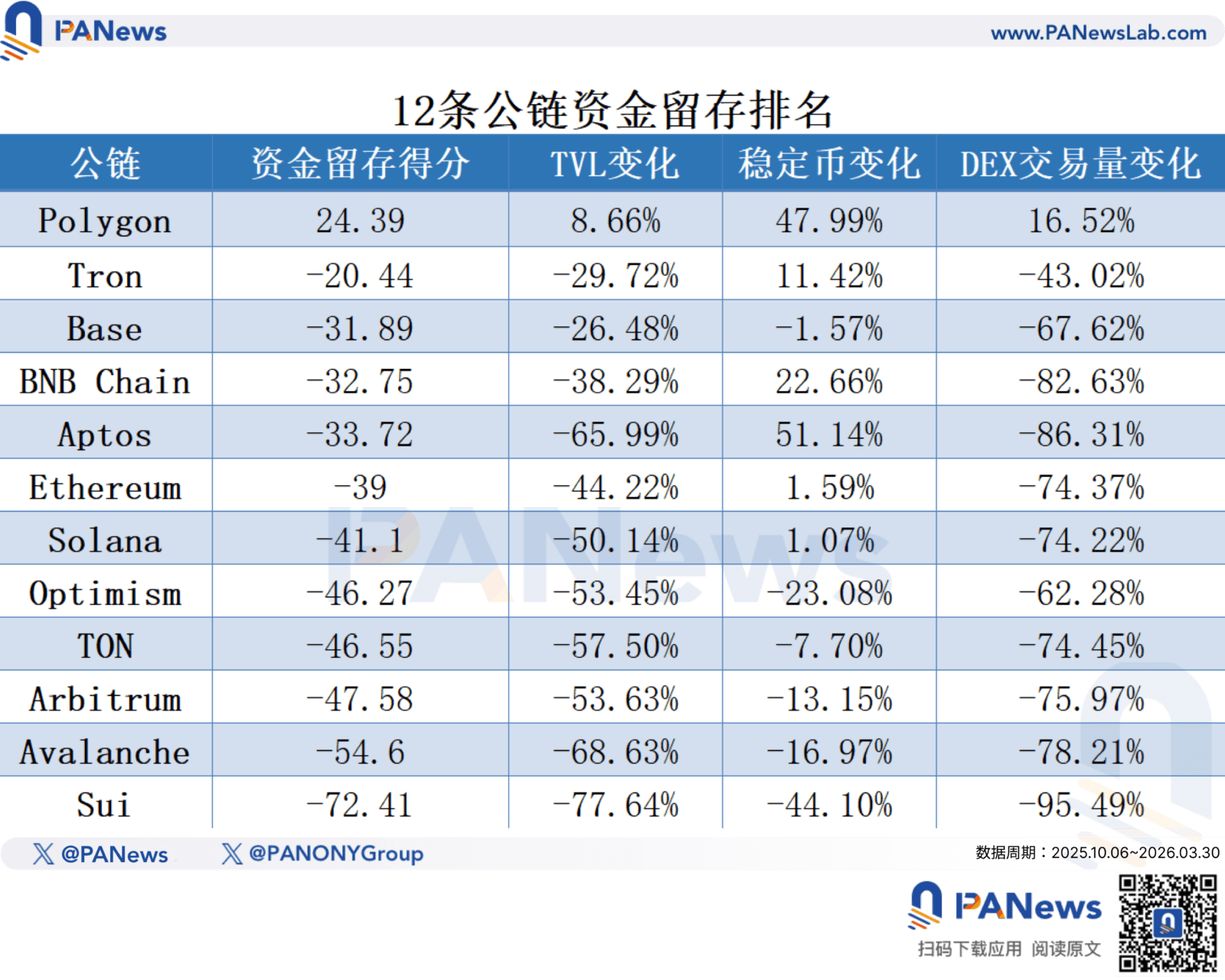

III. 12 Public Chains’ Health Check: Capital Reallocation, User Migration

While token prices reflect market sentiment, on-chain data reveals the true health of an ecosystem. PANews conducted a comprehensive health check on 12 major public chains, examining capital retention (TVL, stablecoin circulation, DEX trading volume) and user activity (daily active addresses). A scoring system was applied, averaging the percentage changes across these dimensions without specific weighting.

The results indicate a significant contraction in capital and activity across most public chains, but amidst this contraction, several anomalous bright spots are emerging.

**Capital Retention: Polygon Stands Alone**

Focusing on capital, Polygon demonstrates the best capital retention among the 12 public chains. Its TVL grew by 8.66%, stablecoin circulation by 47.99%, and DEX trading volume by 16.52% – all three metrics showing positive growth. In a market characterized by substantial capital outflow, Polygon is the only public chain with “all three green.”

The primary driver behind this is likely the surge in popularity of the prediction market Polymarket, which invigorated the entire Polygon ecosystem. Furthermore, Polygon also underwent its Rio upgrade during this period, enhancing performance and accommodating the prediction market’s activity.

Tron (-20.44%), ranking second, is negative overall but saw stablecoin growth of 11.42% and a relatively contained decline in trading volume, indicating a still-acceptable overall performance. Sui (-72.41%), at the bottom, experienced a complete collapse, with TVL down 77.64%, stablecoins down 44.10%, and DEX trading volume down 95.49%, effectively being drained of liquidity.

**Stablecoin Flow: The Most Authentic Capital Compass**

Among all on-chain metrics, stablecoin changes are perhaps the most crucial to watch.

Data shows Aptos’s stablecoin growth of 51.14% as the highest, with Polygon close behind at 47.99%, followed by BNB Chain at 22.66%, and Tron at 11.42%. On the other end, Sui’s stablecoins fell 44.10%, Optimism’s 23.08%, and Arbitrum’s 13.15%. Ethereum (+1.59%) and Solana (+1.07%) remained largely flat.

This data set reveals a critical truth: stablecoins are not largely exiting the crypto market; rather, they are re-parking. Capital is withdrawing from high-risk DeFi protocols, L2 ecosystems, and MEME pools, reallocating to chains that are relatively stable or possess future narrative potential.

Aptos warrants special attention: stablecoins surged 51%, and daily active users grew, yet TVL plummeted 65.99%. This discrepancy is partly due to Aptos’s initially smaller stablecoin market cap (around $1.1 billion). Furthermore, the TVL decline primarily reflects the market cap evaporation caused by a sharp drop in the APT token price. Overall, Aptos’s stablecoin growth is indeed rapid, propelling it into the top ten public chains.

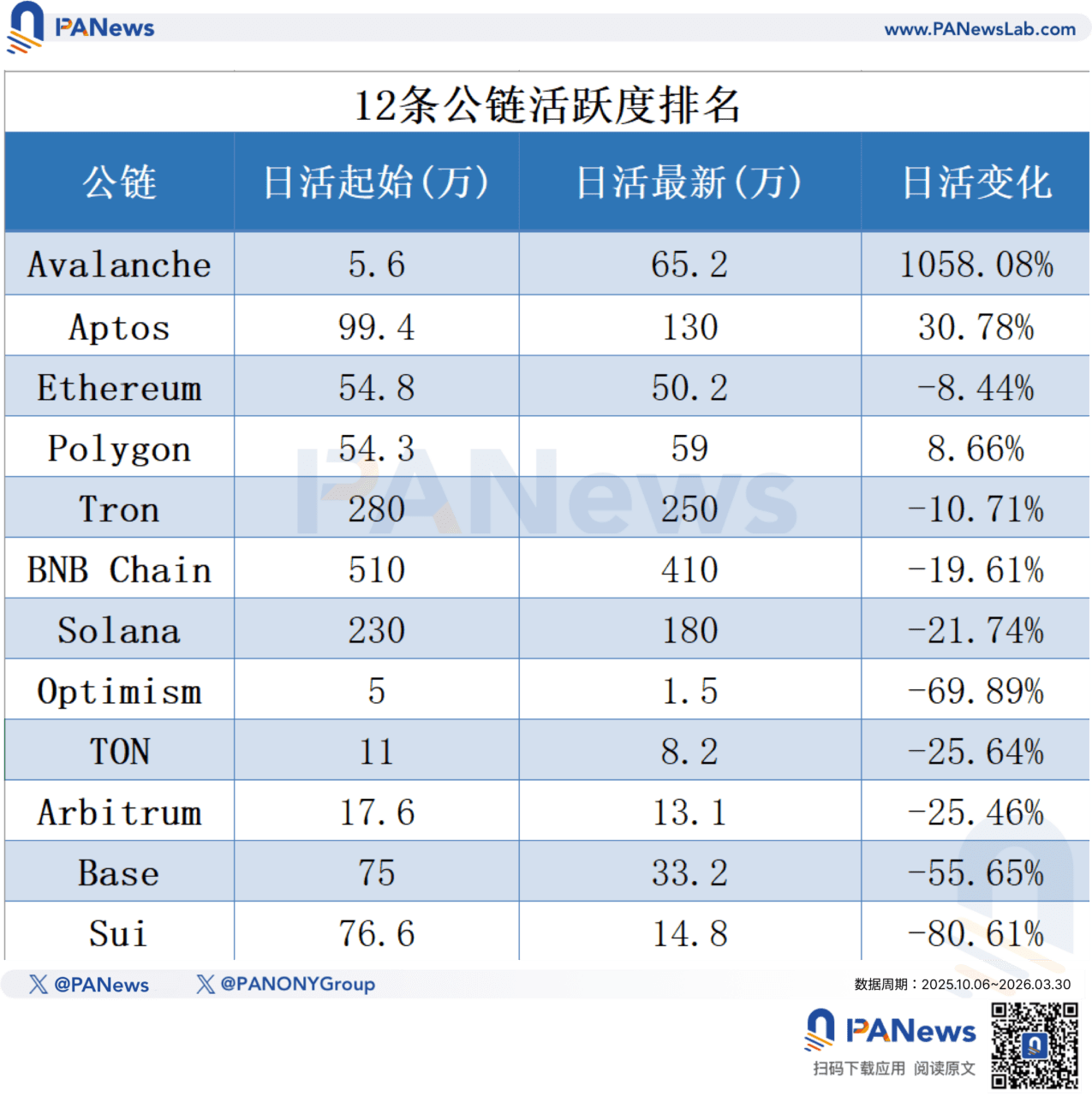

**Daily Active Users: Avalanche’s 10x Surge is the Biggest Surprise**

Using data from growthepie (Ethereum and L2s) and Token Terminal (L1 public chains), PANews analyzed daily active user metrics for all 12 public chains within the research period.

Only 4 of the 12 public chains achieved positive daily active user growth (Avalanche, Aptos, Polygon, and Ethereum which remained largely flat). However, two extremely important discoveries are hidden within this data.

The most significant growth came from Avalanche, with daily active users skyrocketing from 56,300 to 652,000, an increase of over 10x. Yet, during the same period, Avalanche’s TVL fell 68.63%, and DEX trading volume dropped 78.21%. This surge in users despite shrinking capital suggests that new user growth struggled to offset the bear market’s token price declines. This growth primarily occurred after January, with an Avalanche weekly report in January indicating that after January 11, Avalanche’s Interchain Communication (ICM) enabled independent Avalanche L1 blockchains to communicate and transfer assets or data. Notably, three gaming-related L1s—CX, Grotto, and Henesys—contributed a significant volume of transactions.

The second key finding is Ethereum, which saw only an 8.44% decrease in daily active users, almost flat, but a substantial 58.19% increase in transaction count. This indicates that users remaining on Ethereum have become more active. While the number of users slightly decreased, those who stayed are using the network more frequently and intensively.

Aptos’s daily active user growth of 30.78%, coupled with 51.14% stablecoin growth, points to dual growth in both capital and users, yet TVL fell 65.99%. The combined signal is that Aptos is attracting new participants, but they haven’t yet entered DeFi on a large scale.

Conversely, Sui serves as a negative example, with daily active users plummeting from 766,000 to 148,500, an 80.61% drop, forming a three-dimensional downward resonance with TVL and stablecoins. The previous Sui ecosystem craze has completely dissipated, with capital, users, and trading volume all making a full retreat.

IV. Eight Major Sectors: DeFi is the Only Winner, L2 Shows No Pulse

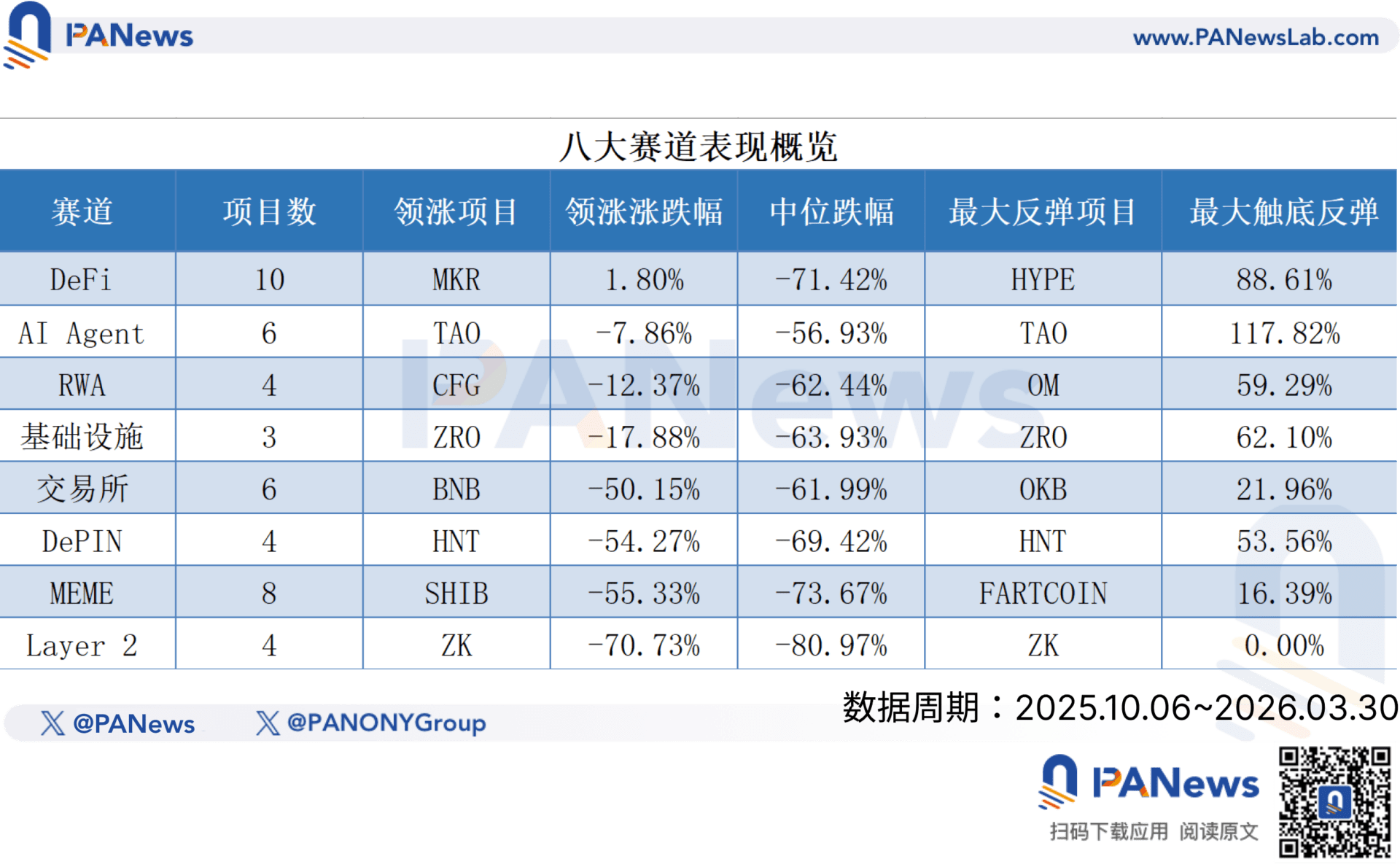

PANews selected 45 representative projects across eight major sectors—DeFi, AI Agent, RWA, Infrastructure, Exchanges, DePIN, MEME, and Layer 2—focusing on those with the highest market capitalization and recognition. From a sector perspective, the ranking from strongest to weakest is: DeFi, AI Agent, RWA, Infrastructure, Exchanges, DePIN, MEME, and Layer 2.

**DeFi: Cash Flow as the Bear Market’s Only Moat**

Among the 45 projects, only Maker (MKR) recorded a positive price return (+1.8%), making it the sole winner. Maker’s sustained growth is attributed to its consistently robust protocol revenue, which has remained at high levels since 2025.

Hyperliquid, with an 18.09% decline, ranked second in the DeFi sector. As a decentralized perpetual futures exchange, it also benefits from the logic that “trading demand does not disappear in a bear market.”

However, internal differentiation within the DeFi sector is severe. Ethena fell 85.10%, Raydium 81.05%, and Pendle 77.71%. Notably, these projects are not without revenue. In fact, many heavily declining DeFi projects have decent protocol revenues. The true dividing line isn’t “having revenue,” but rather the cyclical sensitivity of that revenue. Maker’s stablecoin minting and RWA earnings are not swayed by market sentiment, whereas Pendle’s points trading, Ethena’s funding rate arbitrage, and Raydium’s MEME trading highly depend on bullish market conditions. Once the market cools, both revenue and token prices collapse.

**Layer 2: The Most Devastated Sector**

zkSync fell 70.73%, Arbitrum 80.58%, Starknet 81.37%, and Optimism 86.58%. All four L2 tokens showed 0% bottom bounce, indicating that at the time of data collection, their latest prices were their lowest in the period, continuing to hit new lows with no signs of recovery.

The L2 narrative, as hot as it was in the previous cycle, has suffered an equally thorough collapse in this one. Airdrop expectations, TVL races, and technical roadmap debates – these engines that once drove valuations have all stalled as the market cooled.

**MEME: No Buyers for Established MEMEs**

From SHIB (down 55.33%) to MOG (down 82.77%), bottom bounces were all in the single-digit percentages, with SHIB’s highest at only 8.51%. This suggests that no capital seems willing to step in and support established MEME tokens. However, the MEME market itself still appears active, with platforms like Pump.fun maintaining high levels of revenue and new token creation.

**AI Agent: Platform-Oriented Outperforms Community-Driven**

AI Agent Bittensor (down 7.86%) and Virtual Protocol (down 44.36%) are the only two projects in the AI sector with declines under 50%. In contrast, ElizaOS fell 91.90%, and AIXBT dropped 75.15%. The differentiation logic is clear: projects with actual computing networks or platform functionalities are still being valued by the market, while pure narrative and socially driven AI concept coins are heading towards zero. This logic mirrors the differentiation in the DeFi sector: **what survives is what is “useful.”**

V. Five Signals from the Wreckage

By overlaying data from 424 assets, 12 public chains, and 8 sectors, it becomes clear that the market is engaged in a brutal yet precise re-pricing of everything within the crypto world. The valuation standard is no longer narrative, hype, or expectation, but rather **usage, revenue, and retention.**

From this cleansing, PANews discerns five signals worth continuous monitoring:

**1. Cash Flow Has Become a Survival Threshold.** Four of the 11 positive-return assets are in DeFi. Polygon, the public chain with the strongest capital retention, relies on the continuous transaction volume and active users brought by prediction markets. Maker, the sole sector winner, thrives on protocol revenue. “Real revenue” is no longer a bonus in this market cycle; it’s the minimum threshold for survival. However, this doesn’t automatically guarantee superior token performance.

**2. Stablecoins Are Reallocating, Not Exiting.** Public chains like Polygon (+47.99%), Aptos (+51.14%), and BNB Chain (+22.66%) are attracting stablecoin capital. These public chains, with their clear performance advantages, appear to be gaining capital bets within the new stablecoin narrative.

**3. The Value of Active Users is Declining.** Avalanche saw a 10x surge in daily active users but a significant TVL drop. Aptos experienced dual growth in capital and users but a TVL decline. A closer look reveals that creating a boom in active addresses seems relatively easy, but retaining real capital requires substantial effort.

**4. Previous Hype Narratives Have Completely Failed.** L2 tokens are all at historical lows with zero rebounds. The tail end of AI Agent tokens has fallen over 80%. MEME tokens have broadly collapsed, and Sui is experiencing a three-dimensional downward resonance. The narratives that propelled the market from late 2024 to early 2025 have been deemed severely overvalued by the market.

**5. True Utility Emerges After the Tide Recedes.** JST’s lending, Maker’s stablecoin minting, Stargate’s cross-chain bridge, and Ethereum’s fundamental infrastructure properties. These are not exciting stories, but they are indispensable when users need to transfer funds, seek refuge, or settle transactions.

For the average investor, this data may not directly point to the next 100x token, but it clearly outlines a survival strategy for navigating market cycles. When narratives fade and liquidity dries up, only what is truly being used will be revealed, much like a riverbed during a drought. This is perhaps the most valuable lesson each bear market imparts to the ecosystem.