Author: CryptoCity

- This article was updated on April 8, 2026, to reflect the Executive Yuan’s officially approved draft version.

Taiwan’s Virtual Asset Service Act Draft Clears Executive Yuan: Your Essential Guide to New Crypto Regulations

Taiwan’s burgeoning cryptocurrency industry is poised for a transformative shift as it enters a new era of clear and comprehensive regulation. Following the Financial Supervisory Commission’s (FSC) initial proposal last year, the Executive Yuan **has officially approved the amendment draft of the “Virtual Asset Service Act” in early April this year.** This landmark legislation will now advance to the Legislative Yuan for deliberation, aiming to foster the healthy development and robust management of virtual asset businesses in Taiwan, safeguard investor interests, and stimulate financial technology innovation.

Notably, the Executive Yuan’s endorsed version introduces significantly stricter penalties and management protocols compared to the 2025 iteration. After a thorough review of the complex legal provisions, CryptoCity has distilled the most crucial details into four key highlights, offering readers a rapid and clear understanding. For those seeking the complete legislative text, the official “Virtual Asset Service Act” PDF file is available here.

Virtual Asset Service Act Draft: 4 Core Pillars of Regulation

Pillar 1: VASP Classification and Licensing Framework

The “Virtual Asset Service Act” draft unequivocally mandates that **Virtual Asset Service Providers (VASPs) must secure specific permits and official licenses from the competent authority, tailored to their operational type, before commencing business.** Unauthorized entities engaging in virtual asset activities will be prohibited.

Furthermore, the **revised draft explicitly requires all operators to join an industry association to conduct business,** thereby embedding a robust framework for industry self-regulation. Traditional financial institutions, upon obtaining the necessary permits, will also be permitted to “concurrently operate” virtual asset businesses, benefiting from exemptions on certain regulations.

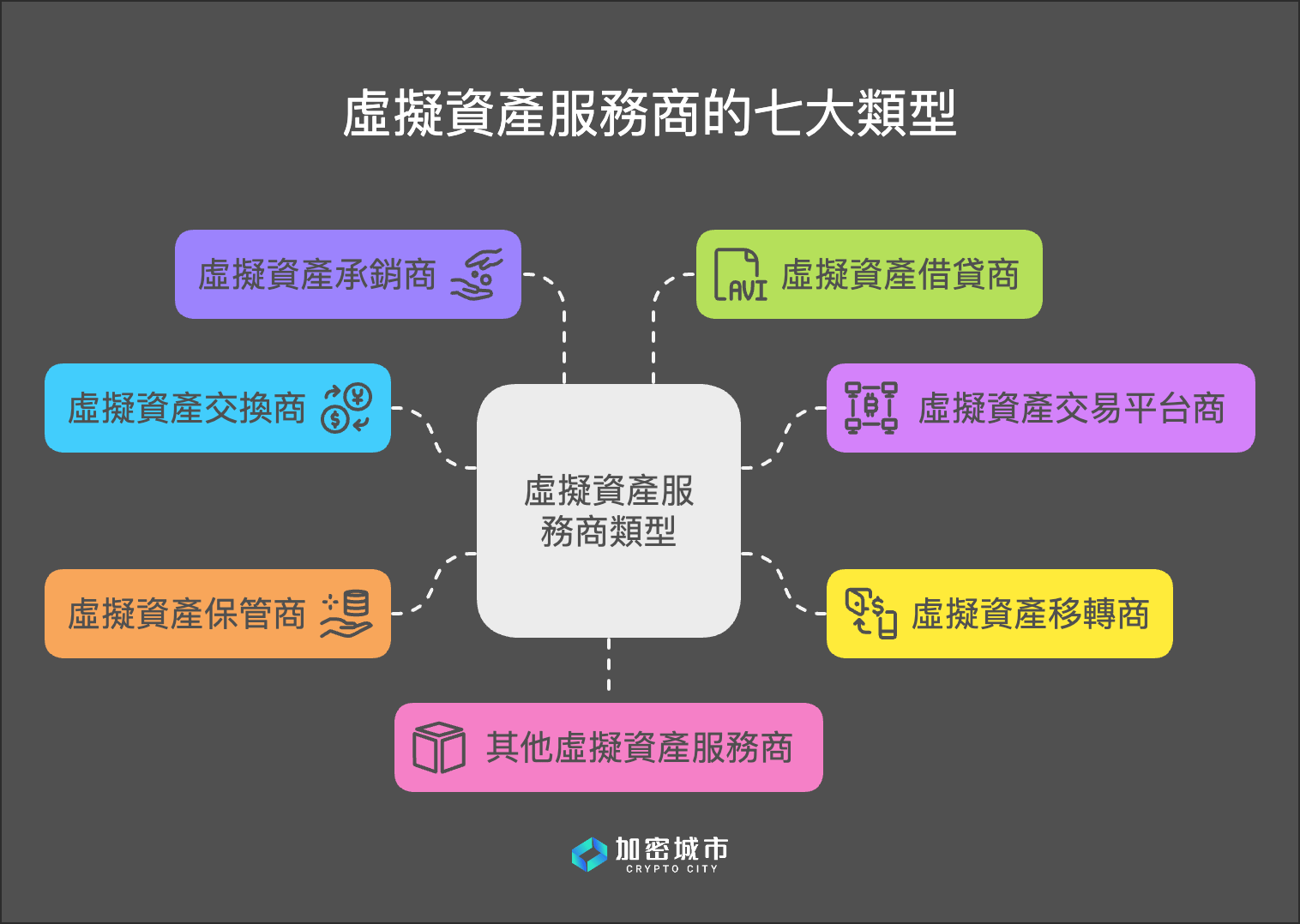

The FSC has meticulously categorized Virtual Asset Service Providers into seven distinct types:

- Virtual Asset Exchange Provider: Facilitates the exchange of virtual assets with New Taiwan Dollars, foreign currencies, or currencies issued in mainland China, Hong Kong, or Macau, as well as virtual asset-to-virtual asset exchanges and related services.

- Virtual Asset Trading Platform Provider: A specialized Virtual Asset Exchange Provider that operates centralized virtual asset trading markets.

- Virtual Asset Transfer Provider: Engages in the transfer of virtual assets and associated services, including those related to virtual asset payments.

- Virtual Asset Custody Provider: Offers services for the custody or management of virtual assets or the tools used to control them.

- Virtual Asset Underwriting Provider: Specializes in the issuance or sale of virtual assets and related services.

- Virtual Asset Lending Provider: Involves the transfer of virtual assets with an agreement for the return or payment of an equal or greater quantity or value of virtual assets, along with related services.

- Other Virtual Asset Service Provider: Encompasses any other virtual asset services designated and approved by the competent authority.

Crucial Licensing Application Deadlines

Addressing the industry’s most pressing concern, the Executive Yuan’s version provides explicit details on the transition period: **Existing operators already registered for anti-money laundering compliance must submit their license applications within 9 months of the Act’s enforcement and secure their official license within 18 months.** Failure to meet these deadlines will result in the cessation of operations.

Regulations for International Crypto Businesses Entering Taiwan

For overseas Virtual Asset Service Providers, such as international cryptocurrency exchanges, **establishing a branch in Taiwan will necessitate obtaining permission and a license from the competent authority, alongside completing company or branch registration within Taiwan.**

Pillar 2: Robust VASP Management and Compliance Architecture

Drawing inspiration from leading global frameworks like the EU’s MiCA, and regulations in Japan and Singapore, the FSC has outlined stringent requirements for Virtual Asset Service Providers. CryptoCity highlights the following critical aspects:

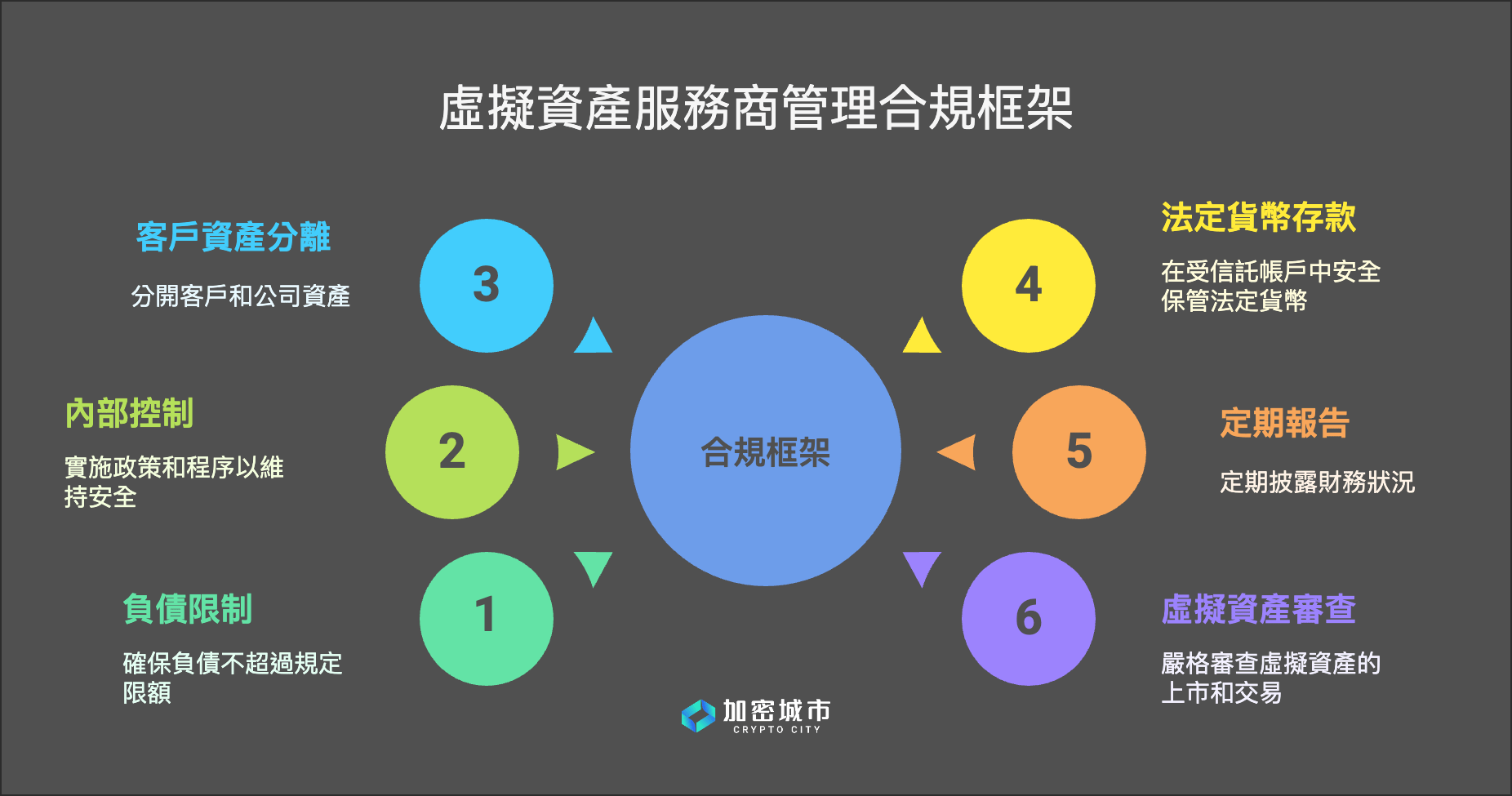

Total Liabilities and Financial Prudence

A VASP’s total external liabilities must not exceed a specified multiple of its net worth, and its current liabilities are similarly capped as a percentage of its current assets. Exemptions apply to financial institutions operating concurrently. The precise multiples and percentages will be determined by the competent authority.

Internal Controls and Administrative Penalties

Service providers are mandated to implement robust internal control systems and stringent cybersecurity protocols. Deficiencies in internal controls, non-compliance with financial reporting, or inadequate listing/delisting review processes will incur administrative fines ranging from NT$300,000 to NT$6,000,000, with the potential for repeated penalties.

Client Asset Segregation and Protection

A cornerstone of investor protection, client assets held by VASPs must be strictly segregated and maintained independently from the VASP’s proprietary assets, as per competent authority guidelines. This includes client virtual assets, fiat currency, and other holdings. Crucially, VASP creditors are explicitly barred from making claims against client assets under custody.

In the event of bankruptcy, client assets are expressly excluded from the VASP’s bankruptcy estate (Note). Client assets may not be utilized except under client instruction, for legal offsetting of fee debts, or with explicit permission from the competent authority. For Virtual Asset Custody Providers, the property rights of client virtual assets remain with the client and cannot be transferred by agreement; commingling with proprietary virtual assets is strictly forbidden.

- Note: The bankruptcy estate comprises all assets owned by a company prior to the conclusion of bankruptcy proceedings, encompassing movable and immovable property, and property claims.

Dedicated Client Fiat Currency Deposit Accounts

With client consent, VASPs may retain fiat currency related to virtual asset transactions in segregated deposit accounts of the same currency established at financial institutions. Such retained fiat currency must be placed in a trust or fully guaranteed by a bank. Reconciliation rules applicable to virtual asset custody providers will extend to retained client fiat currency.

Mandatory Regular Review and Reporting

VASPs are required to regularly submit and publicly announce financial reports, which must be audited or reviewed by a certified public accountant, to the competent authority. Specific reporting procedures, announcement details, and formats will be prescribed.

Virtual Asset Custody Providers must implement ongoing reconciliation measures for client assets under custody, commission certified public accountants to produce reports, and submit and announce these to the competent authority.

Rigorous Virtual Asset Listing/Delisting Review

Virtual Asset Exchange Providers must publish the whitepapers for all virtual assets offered on their platforms. Generally, if a virtual asset lacks a whitepaper prepared and announced in accordance with competent authority regulations, exchange services for that asset are prohibited.

Virtual Asset Trading Platform Providers are obligated to establish clear standards and procedures for listing and delisting virtual assets. Trading platform services for virtual assets not approved by the competent authority are strictly forbidden.

Pillar 3: Strict Stablecoin Issuance Regulations in Taiwan

Entities seeking to issue stablecoins within Taiwan will require explicit permission from the competent authority, which will involve consultation with the Central Bank. The Executive Yuan’s draft introduces exceptionally stringent “red lines” for stablecoins:

- Prohibition of Interest and Yield: Stablecoin issuers are strictly forbidden from paying any form of interest or yield, and must issue and redeem stablecoins at par value. This mirrors provisions found in leading international stablecoin regulations, such as the US “Clarity for Payment Stablecoins Act.”

- Robust Reserve Requirements and Central Bank Penalties: Issuers must maintain fully adequate reserve assets, held independently. Should reserves fall short, the Central Bank will impose a penalty, charging an “annual interest rate of five percent” on the insufficient amount, calculated based on the lowest lending rate.

- Regulation of Overseas Stablecoins: Virtual Asset Service Providers offering services that involve stablecoins not issued in Taiwan may still facilitate their trading within Taiwan, subject to the competent authority’s approval.

Pillar 4: Enhanced Penalties Targeting Fraud and Market Manipulation

The “Virtual Asset Service Act” draft introduces exceptionally severe penalties for fraudulent activities, market manipulation, and other illicit behaviors. The Executive Yuan’s version significantly bolsters practical prosecution mechanisms:

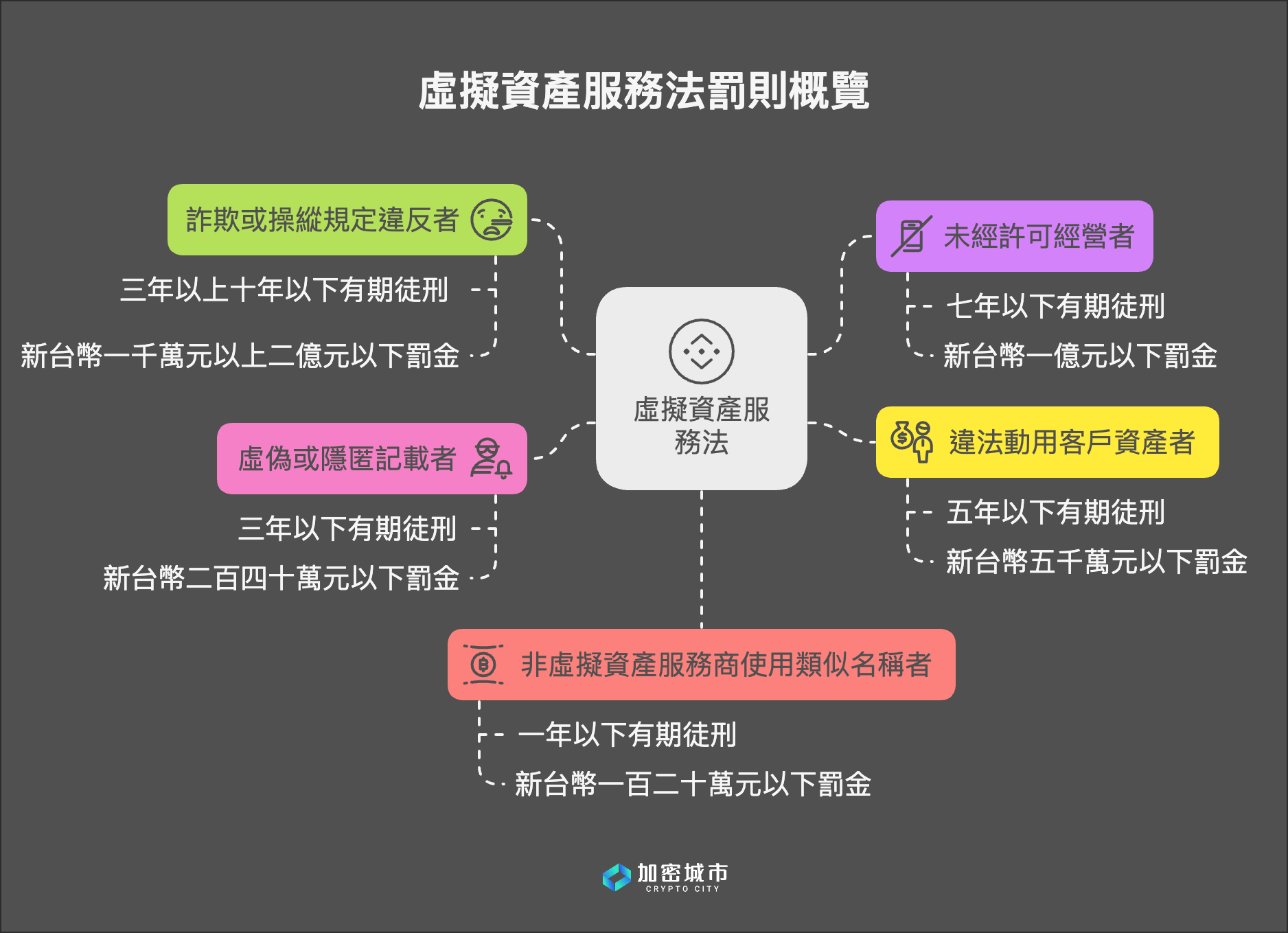

- Severe Penalties for Fraud or Manipulation: Perpetrators face imprisonment for three to ten years, coupled with potential fines ranging from NT$10 million to NT$200 million.

- Incentives for Cooperation: For fraud or manipulation cases, **offenders who self-surrender or confess during investigation, and fully compensate victims within 6 months, may receive reduced or exempted sentences.** This provision aims to facilitate investigations and trace upstream perpetrators.

- Penalties for Unauthorized Operations: Operating without a proper license or issuing stablecoins without permission is punishable by imprisonment for up to seven years, alongside potential fines of up to NT$100 million.

- Misuse of Client Assets: Responsible individuals found illegally using client assets face imprisonment for up to five years, and potential fines of up to NT$50 million.

- Corporate Liability: A concurrent punishment mechanism ensures that if an employee commits offenses such as operating without permission or illegally using assets, the company (legal entity) will also be subject to equally substantial fines, potentially up to NT$100 million or NT$50 million.

- Increased Community Service Terms: For fines of NT$50 million or more, the period for community service (易服勞役) is extended to up to 2 years; for fines exceeding NT$100 million, it increases to up to 3 years.

- Confiscation of Criminal Proceeds: The Act explicitly stipulates that criminal proceeds, whether obtained by the perpetrator or a third party, must be returned to victims and subsequently confiscated.

- Penalties for Misrepresentation and Misuse of Name: Providing false information in applications or failing to submit required reports can lead to imprisonment for up to three years or fines up to NT$2.4 million. Non-service providers using names similar to regulated entities face imprisonment for up to one year or fines up to NT$1.2 million.

The Virtual Asset Service Act: Balancing Protection with Innovation

The FSC emphasizes the imperative of this specialized legislation, citing the global trend of virtual asset regulation in major jurisdictions like the United States, European Union, Japan, South Korea, and Hong Kong. This international consensus underscores the need for a robust framework in Taiwan to ensure sound virtual asset business development, protect investors, and simultaneously foster financial technology innovation.

The revised “Virtual Asset Service Act” draft’s official passage by the Executive Yuan has ignited considerable debate within the industry. Proponents laud the regulations as a vital step towards industry maturation and legitimacy. Conversely, critics voice concerns that the stringent rules might inadvertently stifle innovation and disadvantage emerging startups.

However, it is particularly noteworthy that the Executive Yuan’s version includes specific provisions for **”innovation experiments” (regulatory sandbox) and “international cooperation.”** These clauses explicitly allow operators to apply for innovation experiments and empower the competent authority to facilitate cross-border information exchange, signaling a commitment to both oversight and progress.

In essence, the advent of the “Virtual Asset Service Act” marks Taiwan’s definitive transition from a “wild west” frontier to a fully regulated and compliant era for the cryptocurrency industry. While operators undoubtedly face a period of adaptation and “growing pains,” this legislative milestone sets a clear path for future growth and stability.

Further Insights into Taiwan’s Virtual Asset Industry

- Bitcoin, Stablecoins in Foreign Exchange Reserves? Central Bank Governor Yang Chin-long: Stance Unchanged, but Circumstances Evolve

- Can Taiwan-Issued Stablecoins Yield Interest? Legislative Yuan Submits Legal Analysis, FSC Responds

- Binance’s Potential Entry into Taiwan: Industry Concerns Over Local Platform Impact, National Security Implications of Chinese Capital Background?

(The content above is excerpted and reproduced with permission from our partner “CryptoCity”, original link)

Disclaimer: This article is provided for market information purposes only. All content and views are for reference and do not constitute investment advice, nor do they represent the opinions or positions of BlockTempo. Investors should make independent decisions and conduct their own transactions. The author and BlockTempo shall not be held liable for any direct or indirect losses incurred by investors’ transactions.