On May 6th, MicroStrategy released its Q1 2026 financial report.

The figures presented a challenging picture: a net loss of $12.54 billion, predominantly attributed to fair value adjustments in its substantial Bitcoin holdings. During the earnings call, CEO Michael Saylor notably suggested the company “might sell some Bitcoin to pay dividends,” a statement that sent ripples through the market.

Immediately following this announcement, MicroStrategy’s stock price experienced an after-hours decline of over 4%, while Bitcoin briefly retreated below the $81,000 mark.

Yet, even as traditional markets reacted with apprehension, a distinct narrative was unfolding in the decentralized finance (DeFi) space. MicroStrategy’s perpetual preferred stock, STRC, has rapidly emerged as a “new darling,” captivating DeFi protocols with its unique characteristics.

A sophisticated “BTC on-chain yield structure” has been meticulously crafted around STRC by three prominent DeFi protocols—Saturn, Apyx, and Pendle. This collaboration marks an ambitious financial experiment, pushing the boundaries of Bitcoin’s capital efficiency.

DeFi’s New Darling: MicroStrategy’s STRC Transforms Bitcoin into a Yield-Bearing Asset

The 11.5% Yield Lure: STRC Fuels DeFi Integration

Introduced on Nasdaq in July 2025, STRC, MicroStrategy’s perpetual preferred stock, is designed without a maturity date and requires no principal repayment. Instead, it offers monthly dividend payments, effectively serving as a continuous financing mechanism for the company’s Bitcoin acquisition strategy.

MicroStrategy has implemented an adaptive dividend policy: when STRC’s market price dips below its $100 par value, the board raises the dividend rate to incentivize buying. Conversely, the rate is lowered if the price rises. As of May 2026, STRC’s annualized dividend rate has climbed to an attractive 11.5%, significantly surpassing the approximate 3.7% yield offered by US Treasuries, making it a highly sought-after asset for a broad spectrum of investors.

This ingenious mechanism underpins MicroStrategy’s financing “flywheel.” The company issues new shares at par to raise capital only when STRC’s price is at or above $100. The funds generated, after reserving for dividends, are then channeled into Bitcoin purchases.

Michael Saylor famously terms this approach “intelligent leverage.” For every dollar raised via STRC, MicroStrategy concurrently issues $2 worth of its common stock (MSTR), maintaining an approximate 33% leverage ratio. This strategic allocation means that every $1 of STRC effectively translates into $3 of additional Bitcoin buying power.

Today, STRC’s issuance volume has swelled to $8.5 billion, positioning it among the largest preferred stocks globally. Despite MicroStrategy’s Q1 net loss of $12.8 billion due to Bitcoin impairment, STRC boasts a robust Sharpe ratio of 2.53 and maintains ample liquidity, laying the groundwork for its integration into the DeFi ecosystem.

Saturn: Bringing STRC Dividend Yield On-Chain

Saturn pioneered the on-chain integration of STRC. Having secured $800,000 in seed funding from Yzi Labs and Sora Ventures, Saturn converts STRC’s traditional dividend yield into a seamless, on-chain stablecoin cash flow. Co-founder Kevin Li aptly describes the protocol as “Tether for digital credit.”

Saturn employs a dual-token architecture, reminiscent of Ethena, designed to separate liquidity from yield:

-

USDat: The foundational stablecoin, 100% collateralized by tokenized US Treasuries. It acts as the protocol’s liquidity layer, primarily facilitating payments, settlements, and serving as DeFi collateral.

-

sUSDat: The yield-bearing counterpart to USDat. When users stake USDat into a designated contract, Saturn strategically reallocates the underlying reserve from Treasuries to STRC. Consequently, sUSDat’s yield is directly derived from STRC’s monthly dividend payments.

Saturn’s total STRC holdings have rapidly expanded to approximately $50 million. As STRC dividends are paid in cash, Saturn enhances sUSDat’s value relative to USDat on-chain through mechanisms like cash reinvestment or exchange rate adjustments. As of May 7th, sUSDat’s impressive yield had reached 9.51%.

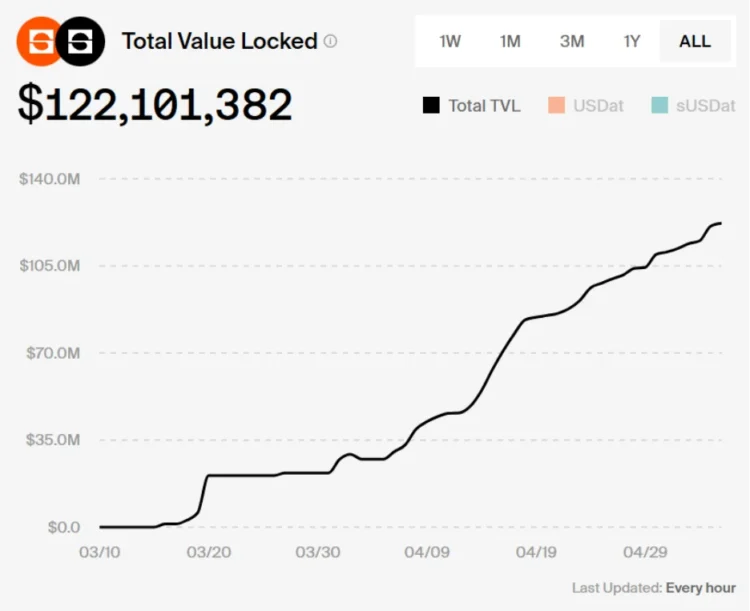

To catalyze early adoption, Saturn launched its “Gravity Points” incentive program, offering 18 to 20 times point rewards for liquidity providers on Curve’s USDC/USDat and USDC/sUSDat trading pairs. This strategy quickly established significant liquidity depth. Within just one month of its mainnet launch, Saturn’s Total Value Locked (TVL) soared from $40 million during its internal testing phase to $122 million—a remarkable increase of over 300%.

Apyx: Supercharging STRC Yield with $130 Million Holdings

While Saturn lays the groundwork for a base currency, Apyx elevates the credit yield proposition. As the largest external holder of STRC on-chain, with holdings valued at nearly $130 million, Apyx specializes in “yield aggregation,” transforming basic dividends into amplified returns.

Apyx, similar to Saturn, distinguishes between a non-yielding stablecoin and a yield-bearing certificate:

- apxUSD: A synthetic dollar, over-collateralized by a basket of assets including STRC and SATA (a preferred stock issued by Strive). apxUSD itself does not generate direct yield; its primary function is to provide liquidity within lending markets.

- apyUSD: A yield certificate. Users deposit apxUSD to acquire apyUSD, which appreciates by capturing all dividend streams from the underlying asset portfolio.

Unlike Saturn, Apyx’s yield incorporates a potent “leverage effect.” Not all apxUSD holders opt to stake their tokens. Consequently, the entirety of the dividends generated by STRC is distributed among a smaller pool of apyUSD holders, effectively amplifying their individual returns. As of May 7th, apyUSD’s 30-day average annualized return stood at 11.1%, with an ambitious expected return target exceeding 13%.

Apyx also integrates sophisticated risk management mechanisms, borrowing elements from traditional finance:

- Dynamic rebalancing: The underlying asset basket is automatically adjusted based on predefined issuer concentration limits, liquidity demands, and over-collateralization requirements.

- 30-day redemption cool-off period: To mitigate the risk of liquidity runs, apyUSD redemptions are subject to a 30-day cool-off period.

Pendle: Carving a Yield Curve for STRC Assets Through Tokenization

As Saturn and Apyx facilitate the on-chain migration of STRC dividends, Pendle introduces a crucial layer of financial sophistication: yield tokenization, imbuing these assets with inherent credit attributes.

Pendle dissects yield-bearing assets like sUSDat and apyUSD into two distinct, independently tradable tokens:

-

PT (Principal Token): These tokens typically trade at a discount. Holders who retain PT until maturity can redeem them 1:1 for the underlying asset, effectively locking in a fixed annualized yield and hedging against potential interest rate volatility.

For instance, if a user acquires PT-apyUSD with a one-year term and an implied yield of 18.42%, spending 1 apyUSD to purchase 1 PT-apyUSD would yield 1.18 apyUSD upon redemption at maturity.

-

YT (Yield Token): YT prices are generally significantly lower than the underlying asset’s value. This structure allows users to gain leveraged exposure to potential increases in STRC dividends with a comparatively smaller capital outlay.

For example, if 1 YT-sUSDat is priced at 4% of 1 sUSDat, a user could purchase 25 YT-sUSDat for the cost of 1 sUSDat. This means even a modest uptick in the sUSDat (STRC) yield could translate into a 25-fold increase in the user’s returns.

Furthermore, users can provide liquidity to Pendle’s sUSDat and apyUSD pools, earning transaction fees and PENDLE token incentives.

Pendle’s innovation marks a pivotal moment, introducing an “implied yield” curve to the Bitcoin credit market for the first time. This development fundamentally signifies Bitcoin’s evolution towards a credit-type asset. Currently, the Total Value Locked (TVL) for assets issued by Apyx and Saturn on Pendle stands at an impressive $200 million and $55 million, respectively.

DeFi’s Dual Impact: Bolstering STRC Resilience While Unveiling Systemic Risks

The widespread integration of STRC by DeFi protocols, while representing an exciting evolution in decentralized finance, simultaneously exerts a profound influence on MicroStrategy’s financing capabilities and the very asset characteristics of Bitcoin.

DeFi protocols, acting as significant STRC purchasers, are objectively enhancing the preferred stock’s price resilience in the secondary market. As long as STRC maintains its value at or above par, MicroStrategy retains the ability to issue new shares and acquire further Bitcoin holdings.

MicroStrategy’s disclosures indicate that over $270 million worth of STRC is currently circulating within the DeFi market, accounting for approximately 3% of its total issuance. This innovative model, where on-chain liquidity reinforces off-chain credit, is poised to become a landmark case study in the burgeoning Real World Assets (RWA) sector.

Through STRC and its sophisticated DeFi derivatives, Bitcoin is being endowed with “interest-bearing” characteristics. For decades, Bitcoin has been primarily regarded as “digital gold,” valued for its scarcity rather than its capacity to generate cash flow. Now, investors can access annualized returns exceeding 10% by holding stablecoins underpinned by STRC’s dividend streams, all without divesting their Bitcoin.

However, the ingenuity of STRC’s on-chain yield structure comes with amplified risks due to its multi-layered, nested nature.

Certain DeFi participants are leveraging circular strategies to significantly amplify their returns: users deposit assets into Apyx to obtain apxUSD, which is then wrapped into Pendle to acquire PT. This PT is subsequently collateralized on Morpho to borrow USDC, which is then used to purchase more apxUSD. This iterative, 5x leveraged process can potentially boost base yields to 60% or even higher.

Yet, the foundational assumptions underpinning this sophisticated chain are remarkably fragile: STRC faces dividend deferral risk. Preferred stock dividends are not mandatory; under adverse market conditions, MicroStrategy’s board could opt to suspend or defer payments. Such a decision would likely cause STRC’s price to deviate sharply from its par value. Should apxUSD consequently become under-collateralized, it could potentially trigger a cascading wave of on-chain liquidations.

From Nasdaq-listed STRC to its intricate three-tiered on-chain yield structure, the crypto market is forging a novel capital logic: a digital credit ecosystem where Bitcoin serves as the foundational asset, Nasdaq facilitates transparent price discovery, and DeFi efficiently manages distribution and circulation.

Saturn fortifies the monetary layer, Apyx strengthens the yield layer, and Pendle dissects the interest rate layer. Together, these protocols form the essential framework of a burgeoning digital credit system, marking Bitcoin’s profound evolution from a mere currency to a robust asset, and now, to the underlying bedrock of a credit infrastructure.

Nevertheless, high returns are perpetually intertwined with high risks, and in the relentless, ever-vigilant Bitcoin market, the inherent cost of leverage often materializes unexpectedly and with significant impact.