By Ariel, CryptoCity

JPMorgan Identifies Permissioned Blockchains as Bitcoin’s True Structural Threat

In a recent report highlighted by The Block, JPMorgan’s analytical team has pinpointed a significant structural threat to Bitcoin: the growing trend of traditional financial institutions bypassing open public blockchains to build their own proprietary infrastructure. This development, according to JPMorgan, poses a more profound risk to Bitcoin than even MicroStrategy’s strategic asset sales, which recently commenced following the launch of its digital credit capital framework.

JPMorgan analysts acknowledge that MicroStrategy’s planned Bitcoin sales for cash generation will introduce cyclical selling pressure. However, they caution that a widespread future shift of tokenization and settlement layers towards closed, permissioned chains could severely dampen overall crypto ecosystem activity, reduce liquidity, and ultimately suppress Bitcoin’s price.

The Institutional Preference for Permissioned Blockchains

Explaining the rationale, JPMorgan analysts elaborated on why institutional investors overwhelmingly favor permissioned blockchains. The primary drivers include enhanced privacy protection, seamless compliance with Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations, and superior clarity in governance and regulatory frameworks. This institutional inclination, the report suggests, directly challenges the dominance of open public chains like Ethereum.

The Bank for International Settlements (BIS) echoes this sentiment, having previously issued warnings about the use of public chains for critical financial infrastructure. Instead, BIS advocates for permissioned unified ledgers that can integrate tokenized central bank money and traditional bank deposits, further solidifying the trend towards controlled environments.

Tokenized Deposits and SWIFT Initiatives Poised to Constrict Stablecoin Demand

The report delves into specific applications, citing banks’ efforts to develop proprietary blockchains for innovations such as tokenized deposits. A key warning emerges: should non-transferable tokenized deposits gain widespread adoption, institutional demand for stablecoins could significantly diminish.

Furthermore, the ongoing advancement of SWIFT’s blockchain initiatives and the development of Central Bank Digital Currencies (CBDCs), such as the digital euro, are expected to reinforce the appeal of regulated, compliant alternatives, potentially sidelining existing stablecoin solutions.

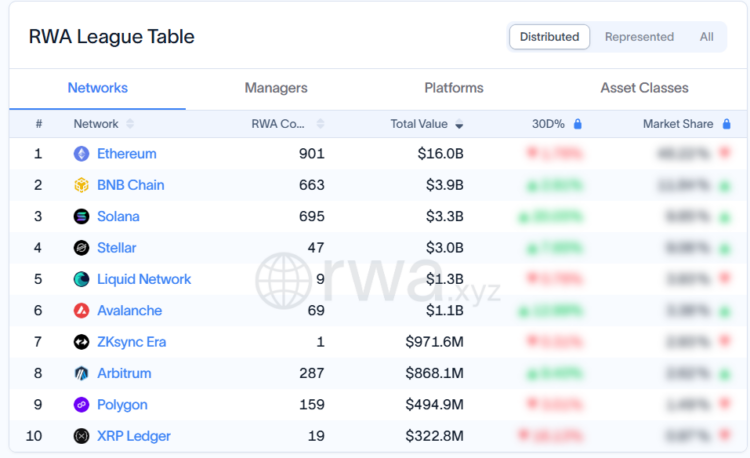

Data from RWA.xyz indicates that the current Real World Asset (RWA) tokenization market stands at $33 billion in on-chain asset value, with a substantial portion presently leveraging Ethereum. However, analysts view this Ethereum-hosted share as merely an early experimental phase. As institutional adoption matures, the issuance of on-chain assets is anticipated to migrate towards private facilities better equipped to meet stringent confidentiality requirements.

Could Upcoming Crypto Legislation Stifle Public Chain Growth?

The JPMorgan report also contemplates the potential impact of forthcoming regulatory frameworks. It suggests that even the anticipated passage of the Digital Asset Market Clarity Act in the US this year, while seemingly beneficial, could inadvertently encourage banks to issue tokenized deposits. This move would bolster the advantages of traditional financial institutions, potentially constraining the organic growth and development of public blockchains.

However, the analysts also provide caveats to this prediction. They note that the emergence of a hybrid model where public and private chains coexist, coupled with improved regulatory clarity fostering stablecoin adoption, or Bitcoin solidifying its role purely as a digital gold hedge, could all serve to overturn their current outlook.

Indeed, hybrid models are already taking shape. For instance, the Depository Trust & Clearing Corporation (DTCC) is experimenting with connecting its permissioned facilities to the Stellar blockchain. Similarly, Securitize leverages a regulated platform to issue tokenized assets on both Solana and Avalanche, showcasing a pragmatic approach to bridging the divide.

The Interoperability Imperative: A Contrasting View from Blocktrend

While many enterprises currently gravitate towards developing and researching closed, controllable chains, Taiwanese crypto media outlet “Blocktrend” offers a contrasting perspective, asserting that the ultimate purpose of on-chain asset tokenization lies in fostering interconnectivity.

In his article, “JPMorgan Spent 7 Years Learning to Use Ethereum,” Blocktrend author Hsu Ming-en highlights JPMorgan’s historical commitment to closed systems. The financial giant launched JPM Coin, based on a private chain architecture, in 2019, accumulating over $3 trillion in cumulative transaction volume by 2026.

However, the inherent limitations of a closed network – primarily restricting transfers to internal clients and preventing integration with external tokenized funds – eventually led to a pivotal decision. By mid-2025, JPMorgan opted to migrate its deposit tokens to Base Chain, an Ethereum Layer 2 scaling solution developed by Coinbase.

Hsu Ming-en posits that this strategic shift unequivocally demonstrates that openness is the paramount factor in determining the true value of on-chain assets. He argues that when faced with the undeniable demand for interoperability, even financial behemoths will ultimately be compelled by their clients to integrate with the broader public blockchain ecosystem.

(The above content is an authorized excerpt and reproduction from our partner, CryptoCity. Original Link)

Disclaimer: This article is provided for market information purposes only. All content and views are for reference and do not constitute investment advice. They do not represent the views or positions of BlockTempo. Investors should make their own decisions and conduct their own transactions. The author and BlockTempo assume no responsibility for any direct or indirect losses incurred by investors as a result of their transactions.