Author: Jonah Burian, Investor at Blockchain Capital

Compiled by: Felix, PANews

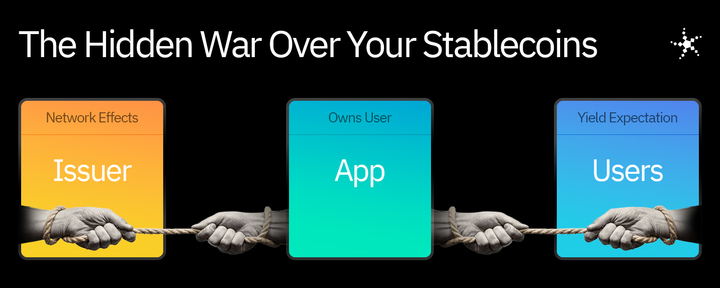

Stablecoins have emerged as a cornerstone of the digital economy, underpinning trillions in transactions and generating immense profits for their issuers. Yet, this unparalleled profitability has ignited a fierce, three-way battle for value capture between stablecoin issuers, the application layers that distribute them, and the end-users who ultimately drive demand. Drawing insights from Blockchain Capital investor Jonah Burian, this article delves into the evolving economics of stablecoin profit distribution and the strategic maneuvers shaping its future. Ultimately, in this intricate game, users may paradoxically emerge as the primary beneficiaries, capturing a significant portion of the total yield.

The Golden Goose: Stablecoin Issuers’ Unprecedented Profitability

The business model of stablecoin issuers is arguably one of the most lucrative on the planet. The mechanics are elegantly simple: users deposit fiat currency, and in return, issuers mint an equivalent amount of digital dollars on the blockchain. Behind the scenes, these fiat reserves are strategically invested in highly liquid, low-risk assets like cash equivalents or U.S. Treasuries, generating a substantial, virtually risk-free yield. Unlike traditional banks burdened by lending, credit risk management, and extensive branch networks, or insurance companies facing potential payouts, stablecoin issuers primarily hold government debt, enjoying a robust cash flow stream without the inherent complexities or significant risks.

This lean operational model means that as their Assets Under Management (AUM) swell, operating costs remain remarkably stable, creating an unconstrained cash flow engine. Tether, for instance, with a team of approximately 300 individuals, projects a staggering $10 billion in profit by 2025 – a testament to a business model arguably among the best in history. However, such extraordinary profitability inevitably attracts intense scrutiny and competition.

The Application Layer’s Assertiveness: Demanding a Share

The vast majority of stablecoin users do not directly interact with issuers. Instead, they engage with stablecoins through various application layers – from popular wallets like Phantom to major exchanges and decentralized finance (DeFi) protocols. These applications are critical as they own the user relationship and thus wield significant bargaining power over issuers. By controlling default stablecoin selections, integrating or deprecating specific stablecoins through product decisions, and influencing fund flows, these platforms can dictate terms.

If billions of dollars in stablecoins reside within a particular application, that application can confidently demand a share of the float. The rationale is clear: “We are your primary distribution channel, anchoring user behavior to your asset. Therefore, you must share your profits, or we will redirect our users to a competing stablecoin.” This dynamic has already played out. A prime example is the historical relationship between Coinbase and Circle. In its early days, Coinbase served as a pivotal distribution engine for USDC, negotiating a substantial profit-sharing agreement. Reports indicated Coinbase secured 100% of the interest generated from USDC on its platform and 50% from USDC held off-platform. This strategy is now being actively pursued by a growing number of applications, both within and outside investment portfolios, as they vie for their slice of the stablecoin pie.

Beyond Negotiation: The Rise of Branded Stablecoins and White-Label Solutions

To further bypass issuers and capture a larger share of the value, application layers are exploring the creation of their own branded stablecoins or “wrapped tokens.” Rather than directly promoting USDC or USDT, these platforms offer users a proprietary dollar-denominated balance, backed by a diversified portfolio of underlying stablecoins and short-term notes. In essence, the distributor begins to participate in the issuance process itself. Aave’s GHO stablecoin serves as a notable example of this approach.

However, building a complete stablecoin issuance infrastructure requires substantial resources and regulatory licenses, which many applications lack. This has led to the emergence of “Issuer-as-a-Service” white-label solutions. Paxos stands out as a leading provider in this space, powering PayPal’s PYUSD. This model allows entities like PayPal to benefit from the float without the need for direct, often complex, negotiations with established stablecoin issuers.

Issuer Counter-Leverage: The Power of Network Effects and Neutrality

Despite the application layer’s growing assertiveness, stablecoin issuers retain significant leverage. Established stablecoins like USDC and USDT benefit from powerful network effects, serving as critical reserve assets across the entire DeFi ecosystem and forming the base pair for countless trading activities. Proprietary, branded stablecoins, while offering profit capture to the issuing application, often suffer from lower liquidity and integration across the broader crypto landscape, making them less attractive to end-users.

Furthermore, white-label stablecoins may lack the “neutrality” of a widely adopted asset like USDT. A company competing with PayPal, for instance, might be reluctant to accept or promote PYUSD, as doing so would indirectly fund a competitor. A similar dynamic arguably influenced Circle’s early growth trajectory; exchanges like Binance may have been hesitant to fully endorse USDC due to its close ties with rival Coinbase, leading Binance to default to USDT. Today, USDT trading volumes on Binance are approximately five times higher than those of USDC, illustrating the impact of such strategic considerations.

The User Factor: A Growing Demand for Yield

In developed markets, a critical new pressure point is emerging: user expectations for yield. With risk-free rates hovering around 4%, users in regions like the United States are increasingly questioning why their digital dollars are not generating any returns. When one wallet offers yield on stablecoin balances while a competitor does not, users naturally gravitate towards the former. Should this expectation become the norm, the application layer will face a significant dilemma. To remain competitive, applications will likely be compelled to pass on a portion of the yield to their users, thereby intensifying their negotiations with stablecoin issuers. If an application cannot secure a share of the float, it becomes challenging to pay interest to users without incurring losses. As more products begin to market “yield on stablecoin balances” as a core feature, the traditional model where all yield remains with the underlying issuer will become increasingly unsustainable.

Geographic Nuances: Where Yield Matters Less

However, this pressure for yield is not universally distributed. In many international markets, the primary value proposition of USD stablecoins lies in their ability to combat local hyperinflation and circumvent foreign exchange controls, rather than generating yield. A user striving to protect their assets from annual depreciation of 50% or more may have little concern for an additional 4% interest. For global issuers with deep penetration in these regions, the user demand for yield is far less urgent than in markets like the U.S. This dynamic could potentially favor Tether, given its extensive overseas user base.

Conclusion: The Evolving Landscape and the Ultimate Beneficiary

In conclusion, the burgeoning expectations of users for yield, coupled with the immense profitability of stablecoin issuers, are placing the application layer in a strategic bind. They find themselves caught between demanding users on one side and profit-preserving issuers on the other. The stablecoin architecture is undergoing rapid evolution, and the ultimate distribution of these substantial profits remains a fiercely contested game. Our hypothesis is that, ironically, the users – the very foundation of the ecosystem – may emerge as the ultimate beneficiaries, eventually capturing the majority of the stablecoin yield.

(The content above is an authorized excerpt and reproduction from our partner PANews. Original Link)

Disclaimer: This article is for market information purposes only. All content and views are for reference only, do not constitute investment advice, and do not represent the views and positions of BlockTempo. Investors should make their own decisions and transactions. The author and BlockTempo will not bear any responsibility for direct or indirect losses resulting from investor transactions.