Authored by Jae, PANews

On March 4th, as geopolitical tensions in the Middle East escalated dramatically, global financial markets instantly shifted into a “wartime state.” For investors worldwide, it was a trading day destined for the history books.

Disruptions to shipping in the Strait of Hormuz, a critical global energy chokepoint, triggered a sharp surge in international oil prices. A wave of panic swiftly swept through traditional capital markets, leading to an epic sell-off across Asia-Pacific stock exchanges.

South Korea’s KOSPI index plummeted an unprecedented 12% in a single day, marking its largest ever daily decline. Japan’s Nikkei 225 plunged 3.7%, its worst performance in five months. Middle Eastern local stock markets, catching up from earlier closures, briefly crashed nearly 5%. Major European and American indices also closed universally lower.

Yet, amidst this widespread market turmoil, an extraordinary phenomenon quietly emerged.

The cryptocurrency market, typically characterized by “high risk and high volatility” and often the first asset class to buckle under geopolitical crises, remarkably held its ground this time.

Following a brief panic sell-off, Bitcoin rapidly stabilized and rebounded, surging past $74,000 at one point to hit a two-week high. On the very same day, investors in Seoul watched in disbelief as the KOSPI breached its circuit breaker limits.

This event transcends a simple “safe haven” versus “risk asset” dichotomy; it signifies a profound re-evaluation of asset intrinsic value, pricing logic, and fundamental market structures.

Asia-Pacific Markets Bear the Brunt: South Korea’s KOSPI Plunges 12%

As conflict ignited, global stock markets entered a grim competition of declines. Asia-Pacific markets, heavily reliant on external energy sources, bore the brunt of the crisis.

South Korea’s stock market suffered the most severe blow.

The Korea Composite Stock Price Index (KOSPI) closed down over 12%, recording its largest single-day drop in history. This followed a 7% decline the previous day (March 3rd). Over two trading days, the cumulative loss approached 20%, wiping approximately $430 billion from its total market capitalization—the most severe two-day consecutive fall since the 2008 global financial crisis.

The KOSDAQ, South Korea’s tech-heavy junior market, fared even worse, plummeting 14% and triggering multiple circuit breakers during the session.

Why was South Korea so vulnerable?

As the world’s eighth-largest oil consumer, South Korea imports roughly 70% of its oil from the Middle East. Net oil imports account for 2.7% of its GDP. Its economy, predominantly manufacturing-driven and export-oriented, is acutely sensitive to energy price fluctuations.

The blockade of the Strait of Hormuz and the ensuing oil price surge translated directly into soaring corporate costs, diminished profit expectations, and intensified inflationary pressures. For this export-dependent economy, the Middle East conflict was not distant news but a direct hit to corporate balance sheets.

The market structure exacerbated the vulnerability. Foreign investors hold over 30% of South Korean equities, while retail investors’ margin trading accounts for nearly 80%. When panic struck, foreign capital withdrawal, margin call liquidations, and algorithmic stop-losses converged, triggering a devastating stampede sell-off.

Japan followed closely behind.

The Nikkei 225 index closed down 3.7%, marking its steepest single-day decline in nearly five months, while the broader TOPIX index fared even worse, falling 4%.

Japan, too, is a major energy importer. Threats of “larger-scale military action” against Iran were enough to send shivers through Tokyo’s trading floors.

Meanwhile, Middle Eastern domestic markets found themselves at the epicenter of the storm.

Upon reopening after a two-day closure, Dubai Financial Market’s main index in the UAE plummeted as much as 4.7% in early trading, an uncommon depth of decline in recent years. Saudi Arabia’s benchmark stock index initially plunged nearly 5% at the onset of the conflict. Kuwait’s stock exchange simply halted trading to avert a catastrophic sell-off.

For Gulf nations, war implies uncertainty in oil revenues, stagnation in tourism and aviation, and an acceleration of capital flight.

The ripple effects of the Middle East conflict swiftly spread to global financial markets, causing European and American equities to collectively weaken. Although the declines were somewhat moderated, major indices still closed in negative territory.

Global Equities Tumble, Crypto Market Stages an Early Rebound

While global stock markets reeled, the cryptocurrency market’s performance astonished many observers.

After an initial panic sell-off, Bitcoin quickly stabilized and rebounded, surging past $74,000 on March 5th to reach a two-week high.

This divergence was no accident. It is the culmination of multiple factors, including pricing efficiency, valuation disparities, inflation risks, anchoring mechanisms, and participant structures.

When the conflict erupted over the weekend, the crypto market was the only one available for trading.

There were no market closures, no circuit breakers, no delays. From the first explosion in Tehran, global investors could immediately express their market judgments within the crypto space.

This meant that by the time Asia-Pacific stock markets opened on Monday morning, the crypto market had already completed several rounds of price discovery, proactively digesting and pricing in most of the associated risks. Bitcoin’s “initial dip, then surge” trajectory precisely reflects this pricing efficiency.

In certain moments, the highly sensitive crypto market may be evolving into a leading indicator for all asset classes.

Furthermore, prior to this “black swan” event, stock markets and crypto markets were operating in distinct valuation cycles.

Major global stock markets had been on a sustained upward trend since the beginning of the year, with the Nikkei 225 repeatedly hitting historical highs, South Korea’s KOSPI at a five-year peak, and the three major U.S. indices hovering near all-time highs. Significant accumulated profits and valuation bubbles were present across global equities.

The emergence of a “black swan” event led to concentrated profit-taking, compounded by stop-loss orders, triggering precipitous declines.

In contrast, the crypto market had undergone multiple deep corrections since October 2023. Valuations and leverage levels for mainstream crypto assets had returned to more reasonable ranges, accumulated profits had been largely realized, and risks were released in advance.

When panic strikes, a market with inflated bubbles and high leverage naturally reacts differently from one that has been deleveraged and potentially undervalued.

The macroeconomic risk variable introduced by the Middle East conflict is inflation.

Soaring energy prices will fuel persistent inflation, forcing global central banks to delay interest rate cuts or even maintain high rates. For stocks, this is a “double whammy” of valuation and earnings compression: higher rates suppress valuations, and increased costs squeeze profits.

For Bitcoin, the inflation logic is precisely the opposite. Its fixed supply of 21 million coins positions it as “digital gold” in an environment of excessive fiat currency issuance and high inflation.

Amid escalating geopolitical conflicts that heighten fiat currency credit volatility, an increasing number of investors are utilizing Bitcoin as a hedge against inflation and currency devaluation.

Concurrently, local capital in the Middle East faces a triple dilemma of fiat currency depreciation, stock market crashes, and heightened geopolitical risk. The need to find borderless, jurisdiction-agnostic safe-haven assets has made cryptocurrencies a primary destination. This influx of incremental capital also helped offset some of the sell-side pressure.

Stock market pricing is anchored to the real economy and corporate earnings, whereas the crypto market’s pricing is anchored to global liquidity and its decentralized nature.

For export-oriented, energy import-dependent economies like South Korea and Japan, the Middle East conflict directly impacted their economic fundamentals. Surging crude oil prices inflated production costs, and in a climate of weak global demand, companies struggled to pass on these cost pressures, significantly compressing profit margins.

Conversely, the fiat currency depreciation and cross-border capital controls triggered by the Middle East situation underscored the decentralized nature of crypto assets, positioning them as an alternative for global capital hedging against geopolitical risk.

This fundamental difference explains why stock markets and the crypto market reacted so divergently to the same geopolitical risk.

BlackRock’s research has previously indicated that Bitcoin performs better than gold and stocks during geopolitical shocks. To date, this conclusion continues to hold true.

The structure of market participants, in turn, dictates volatility.

The steep decline in the South Korean stock market exposed the fragility of its market structure: a high proportion of foreign investment, crowded leveraged trading, and dominance by programmatic trading.

When panic struck, these three factors resonated, directly triggering stampedes and circuit breakers.

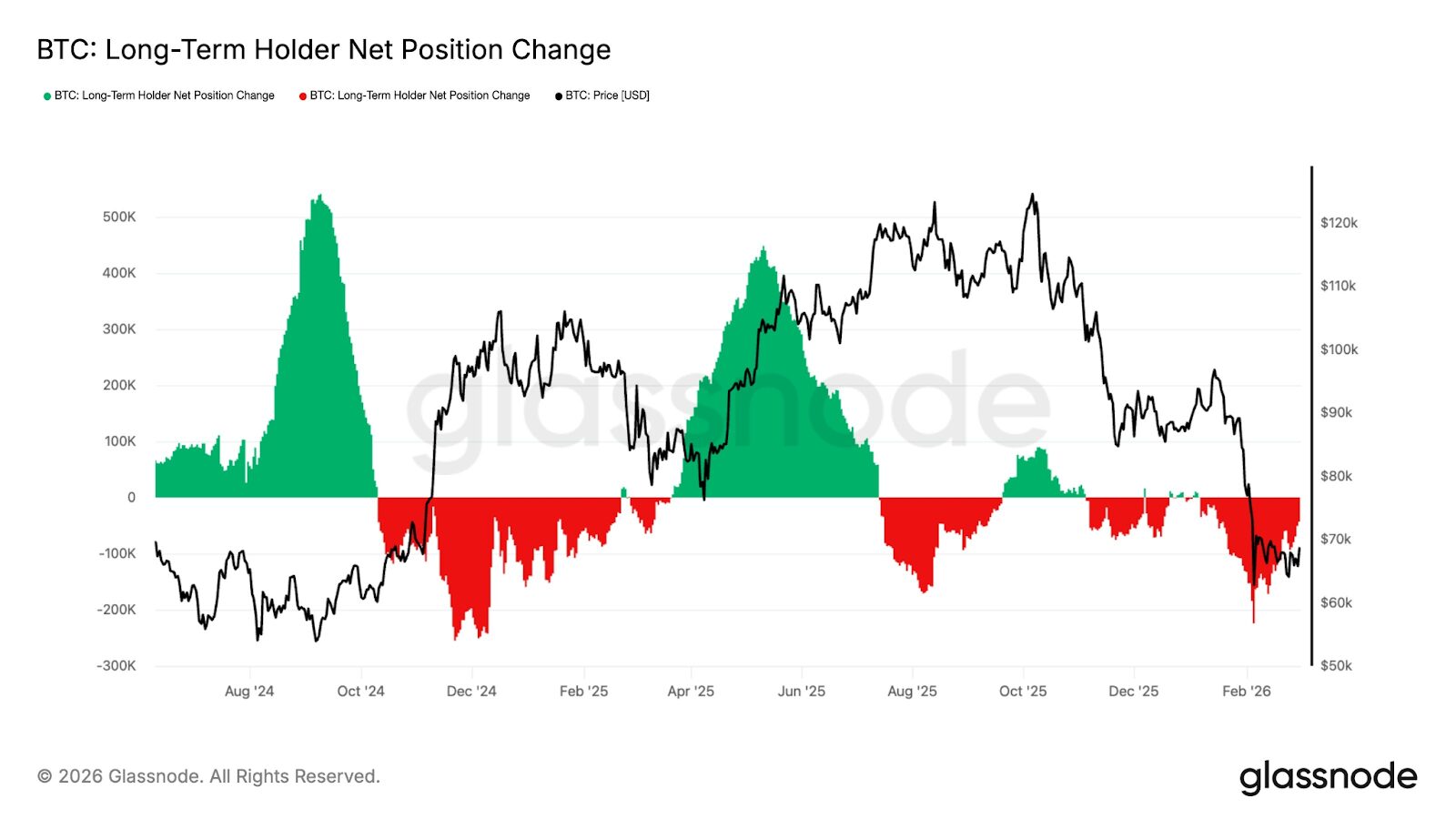

Meanwhile, the participant structure of the crypto market has undergone fundamental changes. Glassnode data indicates a moderation in the net position changes of long-term Bitcoin holders, suggesting a weakening of selling intensity.

The introduction of U.S. spot Bitcoin ETFs has also brought in stable institutional capital. A portion of pricing power has shifted to institutional hands, which typically possess more sophisticated risk management capabilities and a longer-term investment perspective, forming a bedrock of liquidity support.

Crucially, the crypto market had completed multiple rounds of deleveraging before this “black swan” event, and there were no large-scale cascading liquidations in the derivatives market, further mitigating overall volatility.

War is a human tragedy, but it also serves as a crucible for market resilience.

Yesterday’s global sell-off offered a crucial lesson to all investors.

What is perceived as “high risk” may not always be so. While the crypto market held its ground amidst volatility, traditionally “relatively stable” stock markets experienced crashes and circuit breakers.

Whether this is a temporary dislocation or a deeper shift in underlying logic and asset labeling remains to be seen over time.

However, in an era where geopolitical risk is becoming normalized, asset pricing anchors are shifting. Assets tightly bound to a single economy will become increasingly vulnerable, while those anchored to global liquidity will prove increasingly resilient.

The divergence between stock markets and the crypto market during this Middle East conflict once again demonstrates that crypto assets are gradually becoming an indispensable alternative medium in the global geopolitical landscape.

For many nations, the Middle East conflict represents an unavoidable economic shock. For the crypto market, the same conflict has been a validation of its value proposition.

When the storm arrives, what matters is not where you stand, but what your anchor is tied to.

(The above content is an excerpt and reproduction authorized by our partner PANews. Original Link)

Disclaimer: This article is for market information purposes only. All content and views are for reference only and do not constitute investment advice. They do not represent the views or positions of BlockBeats. Investors should make their own decisions and trades. The author and BlockBeats will not bear any responsibility for direct or indirect losses incurred by investors’ transactions.