Author: Campbell, Macro Analyst

Translated by: Yuliya, PANews

Editor’s Introduction: Recently, the U.S. memory chip sector has emerged as a primary driver of the technology market, with companies like Micron Technology, SK Hynix, and SanDisk experiencing sustained stock price surges. Concurrently, the debate over whether Artificial Intelligence (AI) is entering a bubble phase has intensified. Market opinions are sharply divided: Dan Niles, a renowned chip analyst from the dot-com era, posits that current AI development more closely resembles the mid-stage sprint of internet infrastructure in 1997 rather than the tail end of the 1999 bubble. He highlights that the rise of AI agents is fueling a surge in computing power demand, suggesting that while chip stocks may appear overvalued in the short term, their long-term potential remains robust. Legendary hedge fund manager Paul Tudor Jones also estimates that the AI bull market is currently 50% to 60% complete and could persist for another one to two years. In contrast, Michael Burry, the inspiration for the protagonist in the film “The Big Short,” has issued a stark warning, asserting that the current market bears a strong resemblance to the eve of the dot-com bubble burst in 2000.

Amidst this blend of euphoria and apprehension, with prominent figures holding divergent views, a critical question arises: If a bubble truly exists, how should investors respond? Drawing from personal experience, the author of this article offers an in-depth practical guide on “how to short a bubble.” The original article follows below:

To be frank, I don’t know if we are currently in a bubble, nor am I certain if it’s even a knowable question. My understanding largely mirrors yours: the AI revolution is undeniably real.

Despite having shifted my professional investment career towards long positions and writing about it for the past three years, I still feel I haven’t gone long enough. Like many of you, I look around and see individuals becoming extraordinarily wealthy simply by chaining together tokens for AI applications (or going all-in on infrastructure projects providing the computational power to generate these tokens). This sends shivers down my spine, tinged with envy. This, in turn, creates a feedback loop where I struggle to discern whether my views are influenced by jealousy, or if jealousy is merely reinforcing a truth I already know: “keep going long.”

To some extent, I genuinely believe that “the future is here, and it demands immense computational power,” which naturally inclines one to acquire these assets.

I don’t perceive software stocks as performing particularly well, and the market is actively shedding these equities, so there’s little opportunity there.

Like you, I’ve also observed the ultra-low valuations in Korean equities and am intrigued by the opening of their market, which is clearly linked to recent stock market rallies.

I was also surprised by the authorities’ quiet relaxation of the supplementary leverage ratio (eSLR), allowing banks and funds to hold less regulatory capital for purchasing U.S. Treasuries. This feels like a classic case of hidden liquidity injection, a wolf in sheep’s clothing.

-

I can envision a day when interest rates rise sufficiently to end this “liquidity feast,” but that time is not yet upon us.

-

I can also imagine a war bringing this feast to an end; the extreme volatility there previously shook me out of an upward trend, so who knows what the future holds.

-

Furthermore, I can conceive of Canadian bank stocks, trading at three times book value with very low volatility, presenting an excellent shorting opportunity. However, the lack of accessible trading avenues and sufficiently long-dated options prevents me from offering concrete actionable insights in a full article.

Candidly, there’s much more I cannot explicitly discuss here. While this doesn’t alter my fundamental view on trends, it significantly limits what and whom I can address. If you’re familiar with Andreesen’s “Stop the Internal Friction” philosophy, you’ll understand that my cautious nature ensures I’ll never be a billionaire.

However, there is one thing I do know how to do. This is the bit of alpha I can offer you. Today, we won’t debate whether we are in a bubble, but rather, how to short a bubble if you so choose.

Why Is Shorting a Bubble So Challenging?

What defines a bubble? If it looks like a bubble, sounds like a bubble, moves parabolically skyward, and requires increasingly elevated expectations and leverage to sustain price appreciation, then it is a bubble.

So, why is shorting a bubble notoriously difficult?

The core issue is that the easiest assets to short are those with deteriorating fundamentals that gradually become public knowledge, leading to a steady decline and eventual collapse. While you might encounter short squeezes during this process, these often present opportune moments to add to your short position, as the asset is ultimately destined for zero.

Shorting a bubble, however, is an entirely different beast. When an asset’s price surges in an unsustainable, exponential fashion, your short exposure amplifies exponentially with every price increase.

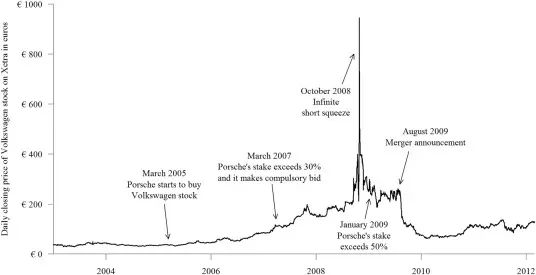

Just ask those who shorted Porsche and Volkswagen in 2008.

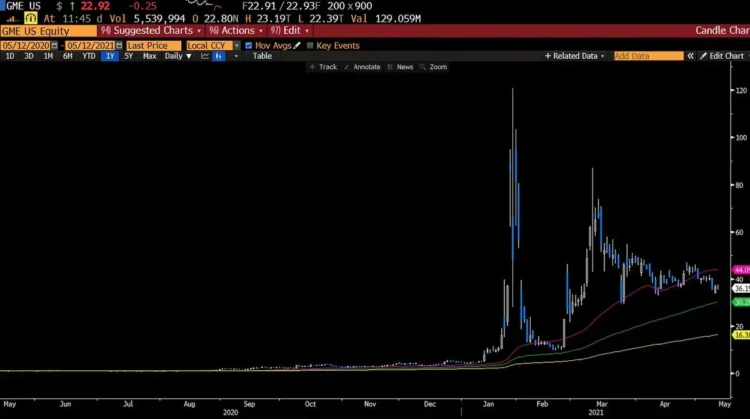

Ask those who shorted GameStop.

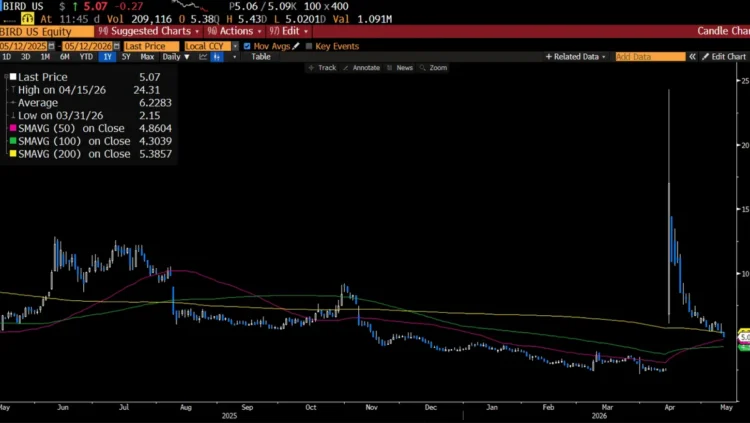

Or ask those who, just a few weeks ago, shorted an obscure shoe company that inexplicably rebranded as an AI firm and crushed all its shorts.

A long investor who sells simply moves to cash. A short seller, however, must buy back the asset to close their position. If their bill quintuples, they are doubly incentivized to cover, sometimes at any cost.

Another reason bubbles are hard to short is that the very characteristics that make them appear exhilarating—”exploding volatility! Fantastic!”—also render their options prohibitively expensive.

If an asset rises 10% daily, its annualized volatility is 160%. Options with such high volatility (160%) mean that merely buying a call option today could cost half the stock’s price. The inherent hedging value derived from actual volatility is so high that these options become impractical for simple directional bets.

Therefore, we are left with only a few viable approaches.

The only ways to effectively short a bubble are:

- Seek the “Wedge”: Identify something external that can puncture the bubble.

- Short the “Victims”: Bet on assets closely tied to the bubble that face potentially limitless downside when it bursts.

- Await “Confirmation”: Wait for definitive breaks in trends and chart patterns.

The remainder of this article will provide examples for each of these methods.

A) Seeking the “Wedge”

The first method to short a bubble is to avoid shorting the bubble itself directly.

Instead, you must identify the “wedge”—the external force capable of puncturing the bubble. You then acquire this wedge to protect your portfolio from the bubble’s eventual collapse.

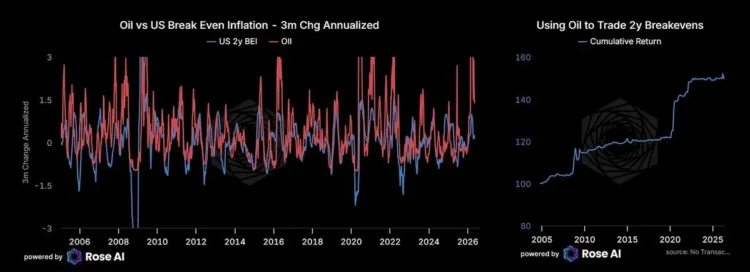

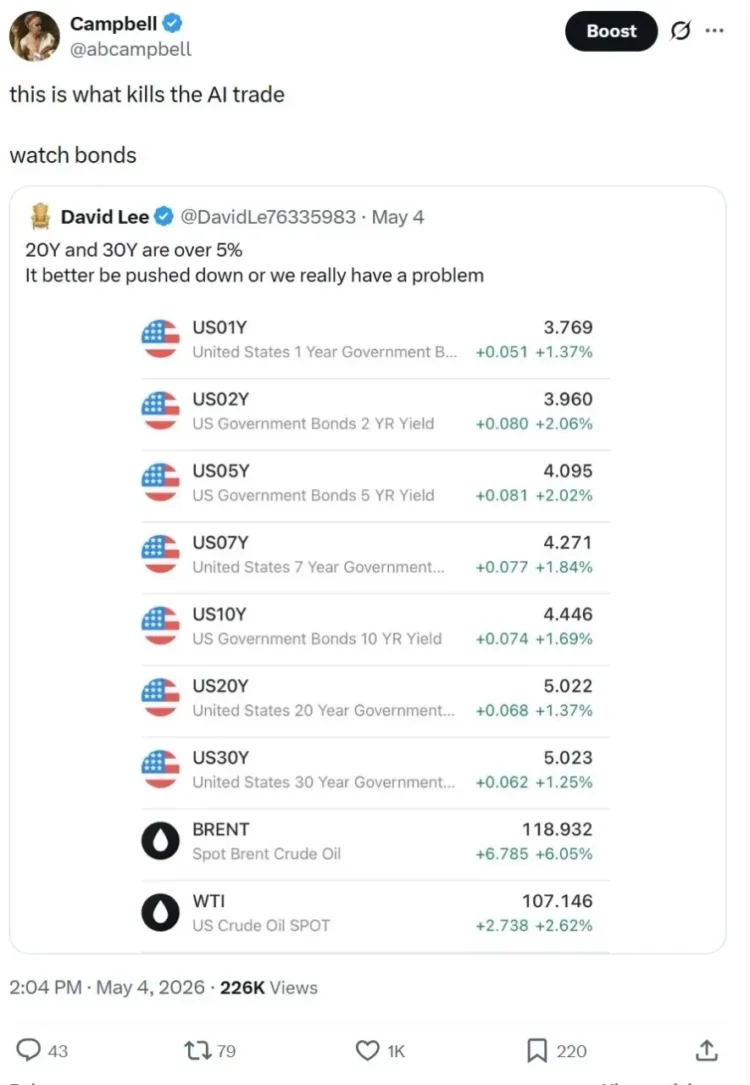

We began implementing this today, just before CPI data confirmed what we already knew: inflation is on the rise.

Interest rates are highly likely to follow suit. As Bob Prince frequently observed, equities also possess bond-like characteristics.

This is the “wedge.” You don’t short the bubble; you go long on the trend that will kill the bubble. If AI is a bubble, then rising interest rates are its wedge.

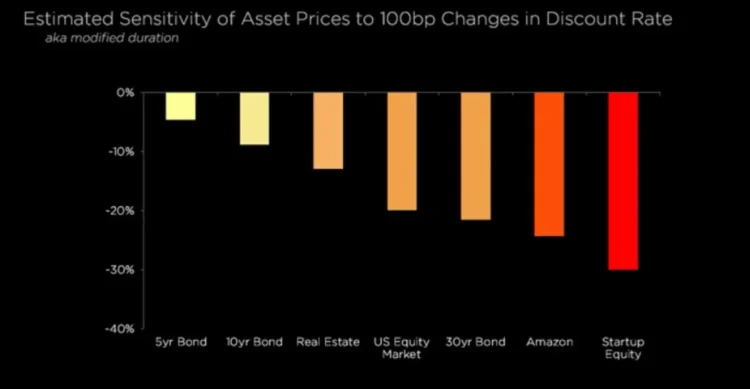

All wildly overvalued assets are, in essence, disguised ultra-long duration assets. As discount rates (interest rates) climb, the present value of those lofty future expectations diminishes significantly. Stocks inflated by speculative projections of 2030 cash flows will be brought back to earth.

Core Principle: Within every bubble, there are elements that depend entirely on its sustenance. The moment the bubble merely pauses, the weakest links will break. You are not betting on the market’s euphoria ending; you are betting that the weakest links cannot survive a market pause.

The beauty of the “wedge” strategy is that it does not require precise timing. The bubble doesn’t even need to burst; it merely needs to cease its acceleration for a quarter, and highly leveraged, speculative assets will begin to collapse.

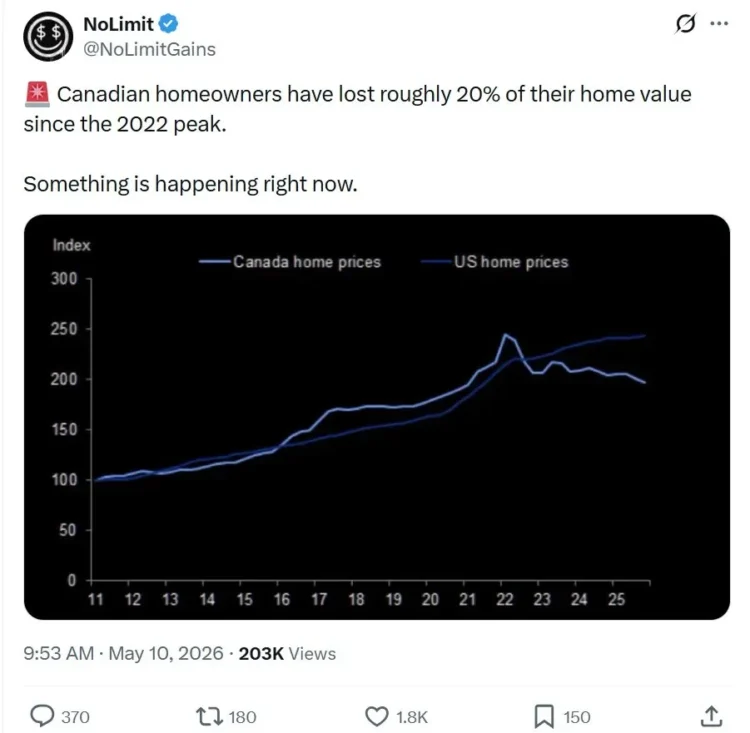

Where is the “wedge” now? I’ll tell you what I’m watching. Canadian banks, trading at three times book value, are laden with “negative amortization” mortgages (where borrower payments don’t even cover interest, with the shortfall added directly to the principal, akin to PIK loans with capitalized interest). They face a real estate market that makes the 2007 U.S. housing market seem remarkably restrained.

I can’t acquire the options I desire on these banks, but I’m keeping a close eye on them. Furthermore, in the broader credit market, as we discussed previously in “Observing Credit,” private credit currently feels like a “roach motel”—money goes in, but it doesn’t come out, reflecting increasingly lax lending standards. When the bubble pauses, the book values of these assets won’t immediately change, as no one forces a revaluation. Not until they are forced to confront reality.

B) Shorting the “Victims”

The second method for shorting a bubble is to identify assets that will be collateral damage when the bubble bursts—those closely adjacent to the bubble.

Evergrande serves as an excellent example. You didn’t need to short Chinese bank stocks, which would have cost you money for a decade. Instead, you sought out a developer with absurdly high leverage, heavily reliant on pre-sales of unbuilt properties, knowing that even a slight slowdown in the Chinese property market could cause it to implode. The bubble could continue to inflate, but Evergrande couldn’t sustain it.

What you’re looking for is “downside convexity”—assets whose decline accelerates in speed and magnitude. You absolutely cannot short assets that are rising exponentially; that’s akin to fighting double the upward momentum.

However, by examining its neighbors, you might find assets whose option volatility hasn’t been inflated to an absurd 70%.

Recall airlines before the pandemic. They weren’t a bubble themselves, but they faced extremely asymmetric risk, leading to a catastrophic decline. At the time, put options were expensive but not prohibitively so. You could still buy options on both ends (e.g., a straddle). So, we did. In hindsight, it seems obvious, but the “bubble” then was actually people’s blind optimism that “everything was normal.”

Consider financial stocks in 2007/08. You didn’t need to short real estate directly (frankly, shorting real estate is exceedingly difficult and technically demanding, though finding mortgage CDS default swaps would be an impressive feat). You simply needed to short Bank of America.

Core Principle: Bubbles create correlations that only become apparent during a collapse. The options market typically prices this correlation only when disaster strikes. Your mission is to find “victims” with cheap options that are destined to be dragged down by the expensive-option bubble assets.

As for who the current “victims” are? Honestly, I haven’t pinpointed them yet.

C) Awaiting “Confirmation”

The third method demands the most discipline, and it’s precisely why most investors fail.

It is simply this: wait.

I understand; waiting is excruciating. Sometimes you watch an asset surge vertically, and you simply cannot resist the urge to act. But again, you absolutely do not want to be run over by a full-speed locomotive.

Therefore, you must await confirmation signals. What do these signals look like?

They are typically a combination of the following:

-

Fundamentals begin to deteriorate.

-

Buying pressure exhausts, and market sentiment wanes.

-

Trendlines definitively break.

Crucially, this is not a minor pullback, but a decisive breakdown. It’s the kind of drop where an asset, previously on a strong upward trajectory, suddenly slices through a key support line, sparking frenzied screenshot sharing on Twitter. We witnessed such a breakdown in silver’s trajectory in January of this year (though don’t look now, it has since rallied back; we’ll discuss this in a future article).

Depending on your chosen timeframe, chart information can appear dramatically different.

The most critical truth regarding AI right now is that the only deteriorating factor is: too much of its projected cash flow is anchored in the distant future.

The problem is, you must discount those future promises using today’s interest rates. If inflation resurfaces, forcing policymakers to tighten monetary policy (imagine if oil prices surge to $150-$200 a barrel; they certainly would), then the net present value (NPV) of many such assets would shrink significantly. This mirrors the logic we articulated during the bond bubble of 2021.

Another aspect to monitor is correlation. Be wary when previously reliable patterns suddenly fail, or when an asset unexpectedly becomes sensitive to factors it previously shrugged off. We might be witnessing this dynamic today.

Practical Application & Conclusion

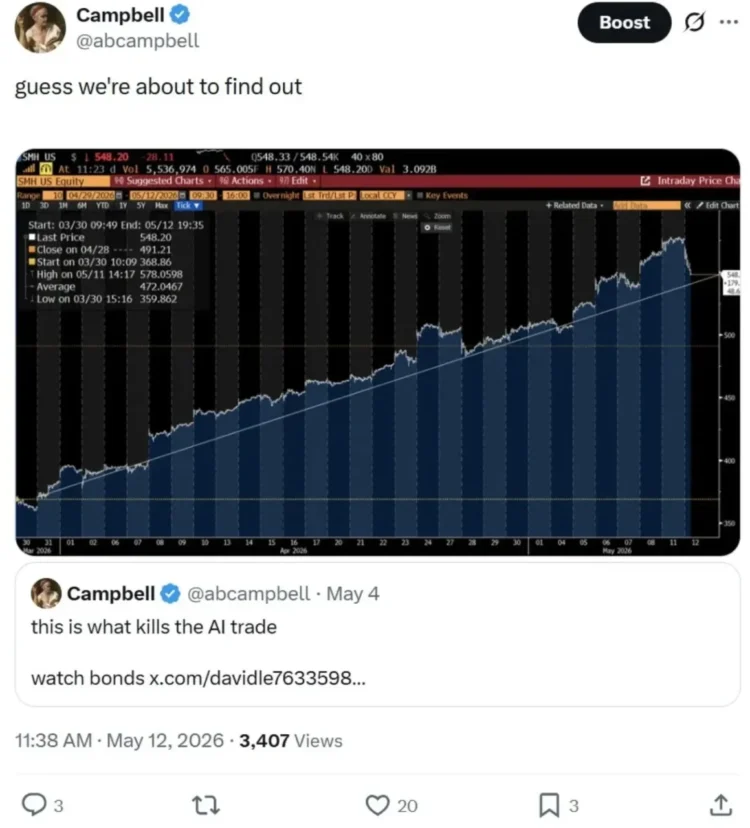

What did I do today? (Earlier today, May 13th) Before the market plunge, I had already implemented some hedges, but not enough. I further shorted 5% of the S&P 500 (SPX) and 10% of high-yield bonds (HYG), then acquired a small short-term put spread. I stepped away for a bit, only to return to a dire situation.

So, what was my actual strategy? I did not short semiconductors, as the core fundamental demand remains intact, and the uptrend hasn’t broken. However, I did short more bonds, specifically buying a U.S. Treasury put spread. If the trendline holds and the market rebounds, I consider it a small price for peace of mind on my “wedge” strategy, largely inconsequential. If the trendline fails, I’d retain cash and protective positions, and only then would I aggressively target specific short opportunities. Oh, and I also sold 5% of my Canadian bank shares.

Hedge, find the wedge, await confirmation, then act decisively.

Listen, I don’t know if we’re in a bubble right now. This rally might only be in the fourth inning (unlikely, given the aggressive price action), or it could be in the ninth inning (which I doubt, as that would require a breakdown in demand for the underlying computational power that generates tokens, a sign I don’t currently observe). The only thing I know for sure is that the “unstoppable” feeling AI evokes in me is strikingly similar to the sensation I experienced in 1999, as a high school student, assembling my first internet stock portfolio. Yes, those stocks eventually recovered, giving rise to giants like Amazon, and if held until today, would have yielded an internal rate of return (IRR) in the mid-teens.

But I also haven’t forgotten the brutal crash that preceded it.

So, if you’ve made it to the end of this meandering essay, you might feel a sense of unease. If you do, the answer is absolutely not to short an asset that is moving vertically. The answer is: find the wedge, buy put options on the victims, then patiently await confirmation signals before acting decisively.

During this period, never fight the market trend. Never short an asset undergoing a parabolic surge.

(The above content is excerpted and reproduced with permission from our partner PANews. Original Link | Source: )

Disclaimer: This article provides market information only. All content and views are for reference purposes only and do not constitute investment advice. They do not represent the views or positions of BlockTempo. Investors should make their own decisions and trades. The author and BlockTempo shall not be held responsible for any direct or indirect losses incurred by investors’ transactions.