Author: Arrakis

Translated & Compiled by: Felix, PANews

This comprehensive analysis delves into the cross-platform lead-lag relationships across 29 cryptocurrency perpetual futures markets, offering critical insights into the underlying architecture of Perpetual Decentralized Exchanges (Perp DEXs).

Unpacking Price Discovery: A Deep Dive into Crypto Perpetual Futures Markets

Introduction

Hyperliquid has rapidly ascended to become the leading on-chain perpetual futures platform, boasting the highest trading volume and open interest. Its ambitious scope has expanded beyond crypto perpetuals to encompass Real World Assets (RWA), prediction markets, and a permissionless DeFi technology stack. Amidst its growth, a compelling claim has emerged: that Hyperliquid is displacing Binance as the primary venue for cryptocurrency price discovery.

This study rigorously examines this assertion. Drawing inspiration from Hoffmann, Rosenbaum, and Yoshida (2013), we employed a modified Hayashi-Yoshida lead-lag estimator across three prominent platforms: Hyperliquid, Binance, and Lighter.

Methodology: Quantifying Lead-Lag Relationships

The central question guiding our investigation is: How long does it take for asset price movements on one trading platform to be reflected across others?

Every trading platform publishes transaction logs, which include a timestamped list of all executed trades. A fundamental approach to quantifying cross-platform lead-lag involves selecting two such transaction logs, shifting one relative to the other across a range of time offsets, and identifying the offset that yields the closest alignment in price movements between the two records. This optimal alignment offset represents the lead-lag relationship between the two platforms.

For instance, if shifting Hyperliquid’s time backward by 700 milliseconds results in its price changes aligning perfectly with Binance’s, it implies that Binance leads Hyperliquid by 700 milliseconds. This analysis utilizes the Hayashi-Yoshida estimator, specifically designed for comparing two price series where trades occur at irregular, asynchronous times. For each candidate time shift, the estimator calculates:

Where Cov(X, Y) denotes the covariance between X and Y, which, in this context, represent the series of realized returns for trades on the two compared venues. σ_X and σ_Y are the standard deviations of these respective distributions.

To mitigate noise from sub-second bid-ask spread fluctuations, the estimator was run separately for buy-side (taker buys) and sell-side (taker sells) executions. For each platform pair, ρ values were computed across a grid ranging from -2,000 milliseconds to +2,000 milliseconds, with 100-millisecond intervals. The shift value where ρ reached its peak was then recorded. A positive lag indicates that the platform listed first is leading.

Our analysis encompassed the top 29 assets by market capitalization that are actively traded across all three platforms:

$BTC, $ETH, $BNB, $XRP, $SOL, $TRX, $DOGE, $HYPE, $ZEC, $ADA, $XMR, $BCH, $LINK, $TON, $XLM, $LTC, $SUI, $AVAX, $HBAR, $NEAR, $TAO, $DOT, $UNI, $ONDO, $WLFI, $ASTER, $ICP, $MORPHO, $AAVE.

The analysis window spanned 16 days, concluding on February 26, 2026. The tested platform pairs were: Hyperliquid vs. Binance, Hyperliquid vs. Lighter, and Lighter vs. Binance.

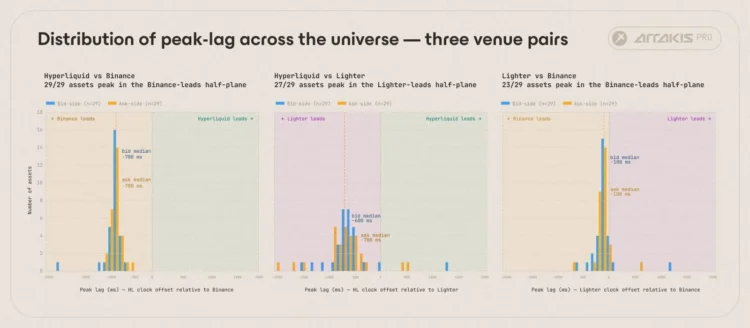

Consistent Findings: Binance Leads Across the Board

All analyses converged on a consistent set of conclusions:

- For all 29 assets: Binance consistently led Hyperliquid.

- For 27 out of 29 assets: Lighter consistently led Hyperliquid.

- For 23 out of 29 assets: Binance consistently led Lighter.

A striking observation is the near-identical appearance of the two Hyperliquid panels: the data consistently clusters around -700 milliseconds, regardless of which platform Hyperliquid is being compared against. From Hyperliquid’s perspective, both Binance and Lighter exhibit very similar delays, leading Hyperliquid by roughly the same magnitude. In contrast, the Lighter vs. Binance panel demonstrates an order of magnitude tighter clustering, peaking around -100 milliseconds, which represents the smallest incremental unit tested for lead-lag in this analysis.

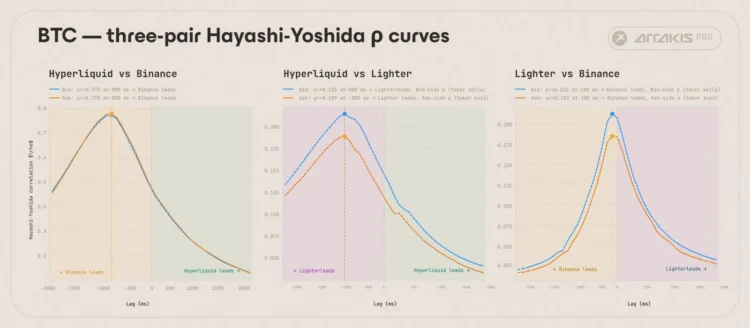

This phenomenon becomes exceptionally clear when examining BTC trades at a single-asset level. The correlation for both Hyperliquid vs. Lighter and Hyperliquid vs. Binance consistently peaks at -800 milliseconds, unequivocally indicating that Hyperliquid trails both platforms at these levels.

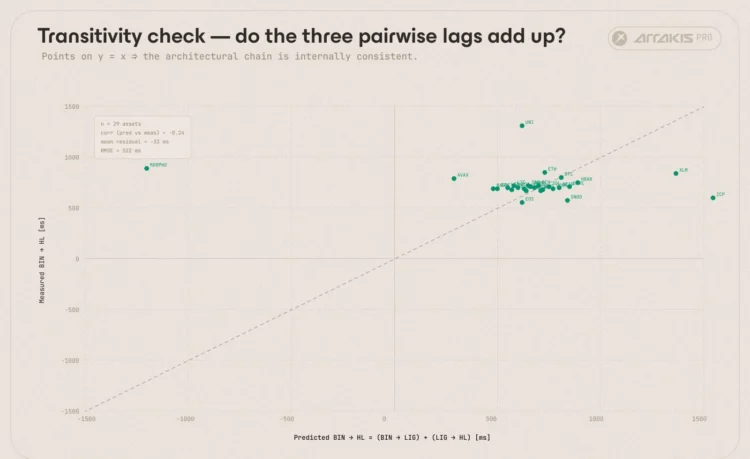

Verifying Transitivity: A Structural Consistency

If the observed pairwise lags between these three platforms reflect a common underlying microstructure, they should exhibit additivity: the lag from Binance to Hyperliquid should approximately equal the sum of (Binance to Lighter) + (Lighter to Hyperliquid). This transitivity was validated across all 29 markets analyzed.

With a median residual of just -33 milliseconds, the transitivity holds true for these assets. Outliers such as MORPHO, ICP, XLM, and UNI occurred because their lag-correlation curves never definitively peaked within the ±2000 millisecond window, preventing the estimator from yielding a clear lead-lag value for them.

All other markets conformed to this transitive relationship. This consistency strongly suggests that the lead-lag phenomenon is determined by the structural methods these platforms employ for matching and settlement, rather than any inherent flaw in a single trading pair.

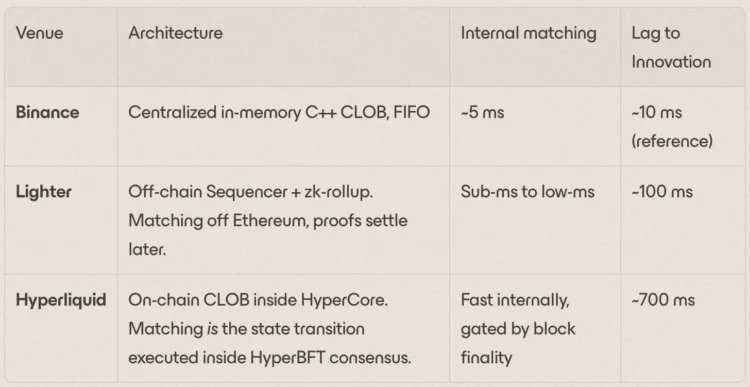

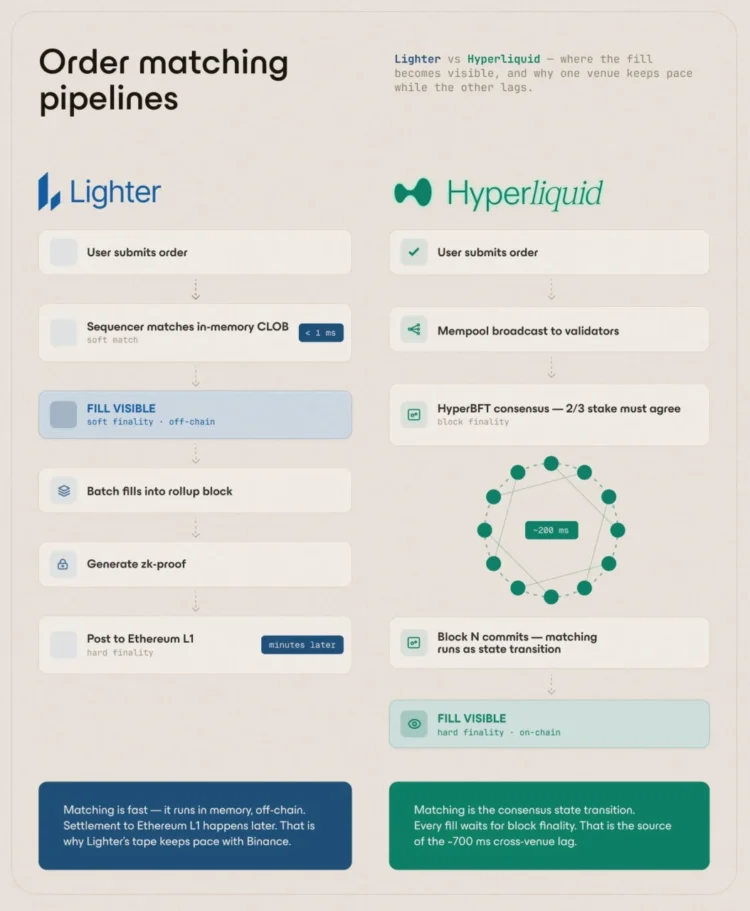

Hyperliquid’s Latency: An Architectural Deep Dive

The three platforms under examination operate with distinct matching architectures.

While Binance and Lighter execute matching in-memory at millisecond speeds, Hyperliquid’s matching mechanism is intrinsically tied to HyperBFT state transitions. Consequently, each trade requires waiting for approximately 200 milliseconds for block finality, as per Hyperliquid’s official documentation. However, the observed lag in executed trades is closer to 700 milliseconds, not 200 milliseconds. This additional ~500 milliseconds stems from the round-trip communication between market makers and traders.

The most plausible explanation is that a single “maker-taker” round trip spans two consecutive blocks. Here’s the sequence of events following a price change on Binance:

- **Stale Liquidity Persists on Hyperliquid:** Market maker quotes on Hyperliquid, still pending, become mispriced relative to Binance’s new price.

- **Mempool Competition:** Arbitrageurs speculatively submit numerous Immediate-or-Cancel (IOC) orders targeting this anticipated stale liquidity. Concurrently, market makers trigger “cancel-and-replace” transactions to update their quotes, designed to land at the top of the block. Market makers failing to refresh their quotes within this block become vulnerable to arbitrage.

- **Block N Commits (approx. 200-300ms):** Cancelations remove outdated market maker quotes, and new orders publish refreshed quotes. Surviving IOC orders consume any remaining stale liquidity at old prices, meaning most trades in this block occur at prices that are already outdated relative to Binance.

- **Order Book Cleansed, Awaiting Interaction:** At this point, Hyperliquid’s order book has been cleared, but no trades have yet occurred against these newly updated quotes.

- **Takers Engage with Updated Prices:** Takers begin to trade against the now-refreshed prices.

- **Block N+1 Commits (approx. 500-700ms):** Taker orders are matched against the refreshed quotes. This represents the first execution carrying the new price information, which is the trade captured by our estimator as being correlated with the price innovation on Binance.

This implies that a price change originating on Binance necessitates at least two full HyperBFT cycles to manifest within Hyperliquid’s execution data.

In stark contrast, Lighter completely bypasses this multi-block process. Its sequencer performs matching in-memory; quote updates and subsequent trades against those quotes occur within the same millisecond. The approximate 100-millisecond lag observed for Lighter reflects the combined latency of its indexer and API, which is also the minimum granularity unit tested in our estimator for lead-lag relationships.

The Lighter Paradigm: Challenging Assumptions

Lighter’s pricing closely tracks Binance, exhibiting only a marginal delay relative to Hyperliquid. This effectively refutes the assumption that “DEXs are inherently subject to lag” simply because they are decentralized, as Lighter is also a DEX. Lighter’s order flow is processed by a centralized off-chain sequencer, yet the entire system maintains a verifiable decentralized architecture through zero-knowledge proofs (zk-proofs settled on Ethereum).

The key differentiator lies in the layer at which decentralization is enforced. Hyperliquid implements decentralization at the matching layer: every order, cancellation, and execution is submitted by a validator set. Lighter, conversely, enforces it at the settlement layer: its sequencer matches orders in-memory and then cryptographically proves the correctness of these executions to Ethereum post-trade.

Lighter achieves its speed by shifting the trust boundary from the matching layer to the settlement layer. Hyperliquid, by maintaining the trust boundary at the matching stage, incurs a latency cost.

Pathways to Latency Reduction for Hyperliquid

To improve its pricing lag relative to price discovery platforms like Binance, Hyperliquid could implement several modifications to its current design:

- Tighter HyperBFT Pipeline: By optimizing leader rotation, enabling parallel voting, or enhancing network infrastructure, block times could be pushed below the current ~200-millisecond mark. Every millisecond saved would compress both block times in the round-trip process. While this wouldn’t eliminate the structural cause of the lag, any substantial improvement in block times would significantly reduce price latency.

- Pre-Confirmation or Soft Finality Layer: Establishing a separate, fast lane for pre-confirmations, where inclusion in a block is acknowledged while HyperBFT finality arrives asynchronously. Market makers could then post quotes against this pre-confirmed state, effectively reducing tick-to-tick latency. The trade-off here is that pre-confirmations are trusted commitments, requiring reliance on trusted infrastructure or collateral-backed assurances with slashing mechanisms. Both reintroduce trust assumptions that Hyperliquid currently avoids.

- Decoupling Matching from Consensus: This represents the most ambitious and costly solution. Operating an off-chain, high-speed matching layer to generate provisional executions, which are then batched and submitted to consensus, would structurally align Hyperliquid more closely with Lighter’s design. This would drastically compress the latency floor, but it would entail a significant shift in trust assumptions compared to the current permissionless validator model.

Each of these pathways necessitates intrusive architectural modifications at different layers and introduces trust assumptions that are not present in the current system. The question for the Hyperliquid team and community is whether the latency reductions afforded by these approaches are worth the trade-off of introducing additional trust assumptions.

Implications for the Future of On-Chain Price Discovery

Hyperliquid has undeniably cemented its position as a leading Perp DEX in terms of liquidity, open interest, and retail participation. It has pioneered a unique frontier in DeFi, introducing novel market types that don’t exist in traditional finance: weekend trading for equities and commodities, pre-IPO equity perpetual markets, and outcome prediction markets for inflation, among others.

However, as the market matures and more sophisticated participants enter the fray, the next wave of competition for on-chain perpetuals will increasingly revolve around latency. Hyperliquid has successfully built the most liquid platform on top of a truly decentralized, on-chain matching engine. The critical challenge now is whether it can maintain its status as the primary “price discovery” venue for these innovative markets while adhering to its foundational design principles.

(The above content is an excerpt and reproduction authorized by partner PANews. Original Link)

Disclaimer: This article is for market information purposes only. All content and views are for reference only and do not constitute investment advice. They do not represent the views or positions of BlockTempo. Investors should make their own decisions and trades. The author and BlockTempo will not bear any responsibility for direct or indirect losses incurred by investors’ transactions.