Author: Nancy, PANews

SpaceX Soars: Elon Musk’s Trillion-Dollar Space Dream Takes Flight on Nasdaq

After more than two decades of audacious vision and relentless pursuit, Elon Musk has finally launched SpaceX onto the public markets, marking an epochal moment in the history of commercial space exploration.

At the momentous Nasdaq bell-ringing ceremony, Musk, beaming in remotely from SpaceX’s Starbase headquarters in Texas, articulated the company’s grand ambition: “It’s hard to believe a company that started in a small warehouse in El Segundo is now embarking on the largest IPO in history. We hope that in the future, anyone who wants to go to the Moon, anyone who wants to go to Mars, or even any corner of the solar system, will have the opportunity to do so. Someday, we hope to be able to take you there, not just a select few astronauts. Whoever you are, SpaceX hopes to take you to the Moon, take you to Mars, and ultimately beyond. I am now very confident that with this incredible team at SpaceX, we will make all of this a reality in the near future.”

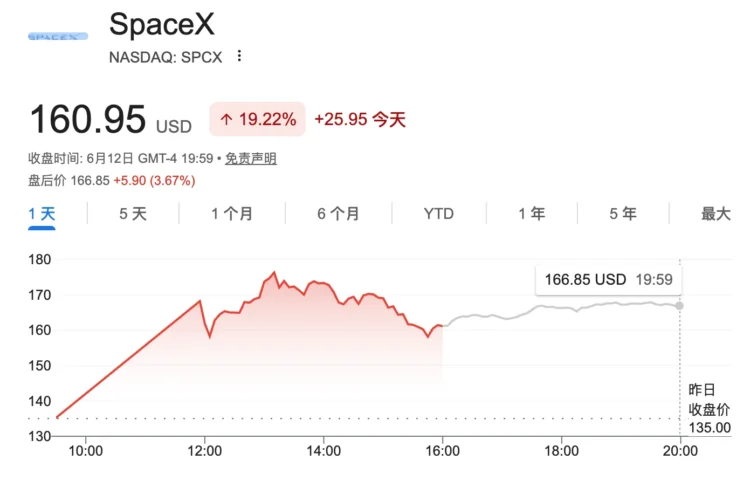

On the evening of June 12th, SpaceX officially rang the opening bell on Nasdaq, trading under the ticker symbol “SPCX.” By market close, SpaceX shares had sustained their robust rally, surging over 30% intraday from their offering price of $135 and ultimately closing up 19.22% at $160.95. This propelled the company’s total market capitalization to an astounding $2.1 trillion, instantly establishing it as the sixth-largest company by market cap in the United States.

This space titan, which once endured three rocket launch failures and teetered on the brink of cash depletion, had repeatedly pushed Musk to the darkest hours of all-or-nothing gambles. Today, it has successfully opened the doors to the public market with a stratospheric valuation, not only setting a new record for the world’s largest IPO but also ushering in an unprecedented new chapter for the commercial aerospace industry.

A Global Frenzy: The IPO Subscription Battle

Even before its market debut, Wall Street had already entered “SpaceX time.”

To orchestrate this monumental IPO, SpaceX assembled a formidable syndicate of 23 Wall Street investment banks. Goldman Sachs led as the primary underwriter, with Morgan Stanley, Bank of America, Citi, and J.P. Morgan among the many participating institutions.

Senior investment executives personally spearheaded efforts to secure client resources, hosting exclusive roadshows for ultra-high-net-worth individuals and institutional clients. Goldman Sachs and Bank of America even showcased rocket models in their headquarters lobbies, while Musk’s mother, Maye Musk, made an appearance at J.P. Morgan’s roadshow. Market estimates suggest this IPO alone could generate over $500 million in underwriting fees for the participating banks.

Analysts noted that these major investment banks not only aimed to ensure a smooth listing for SpaceX but also hoped to leverage this landmark IPO to bolster market confidence, creating a more favorable environment for anticipated large-scale IPOs from companies like OpenAI and Anthropic.

From the long-term vision of a multi-planetary civilization to the hyper-scale commercialization of orbital AI, SpaceX’s electrifying roadshow ignited investors’ imaginations, drawing in a torrent of global capital. Multiple media outlets cited market sources indicating that SpaceX’s IPO garnered over $250 billion in subscription demand, far exceeding the planned fundraising target of approximately $75 billion, resulting in an oversubscription rate of nearly four times.

Institutional funds emerged as the primary drivers of this subscription frenzy, with around 1,000 institutional investors participating. BlackRock reportedly placed a single subscription order exceeding $5 billion, while Middle Eastern sovereign wealth funds such as Saudi Arabia’s Public Investment Fund (PIF) and the Kuwait Investment Authority (KIA) submitted multi-billion dollar orders.

Retail enthusiasm was equally fervent. Bloomberg, citing sources familiar with the matter, reported that retail investor demand for SpaceX subscriptions surpassed $100 billion, vastly outstripping the allocation reserved for individual investors. Under the current offering structure, it was anticipated that most retail subscription applications would not receive full allocation, with many missing out entirely.

The allocation results for cryptocurrency investors were particularly limited, essentially a wipeout, with only a select few receiving minimal “consolation” shares:

- Kraken users generally received approximately 4.2786 SPCXx shares each, equivalent to about $600. Regardless of the subscription amount, this was largely a “participation prize,” with all remaining funds fully refunded.

- Gate adopted a proportional allocation, with a success rate of about 3% of the subscribed principal, slightly better than other platforms.

- Binance announced full refunds and additionally purchased $1 million worth of SPCXB tokens from its own pocket for an airdrop, averaging about $40 per user.

- Bitget also provided full refunds, along with a roughly $10 fee discount coupon as compensation.

- Bybit, in addition to refunds, compensated users with a 10% annualized yield for four days on their deposited funds.

The initial high enthusiasm among crypto users ultimately led to frustration, with many receiving only full refunds or symbolic compensation, sparking discontent and even transforming some IPO groups into rights protection forums. The primary reason for this phenomenon was that most exchanges relied on xStocks as their underlying asset provider. The overwhelming institutional and retail subscription demand significantly exceeded the underwriting quota, leading to substantial reductions, and in some cases, complete cancellation, of orders across multiple platforms.

Nevertheless, this did not dampen the fervent excitement surrounding SpaceX. During the SPCX opening phase, trading did not commence at the regular 9:30 AM EST as scheduled, experiencing a delay. This is characteristic of ultra-large-scale IPOs, where exchanges typically initiate an opening cross-auction process to centralize buy and sell orders, balance supply and demand, and determine a fair opening price. Similar delays have occurred with other major IPOs such as Meta, Alibaba, and Figma.

In fact, to prepare for the potentially historic trading volumes and order processing pressures, institutions like Nasdaq, Citadel Securities, Jane Street, and S&P Global had conducted multiple rounds of internal drills and system stress tests weeks in advance. S&P Global stated that it had increased its processing capacity by approximately 200% over the past six weeks through system upgrades and real-time testing, describing it as an extraordinary preparation for unprecedented trading scale, a level of readiness rarely seen in previous large IPO projects.

Early Investors and Employees Reap Unprecedented Wealth

Following SpaceX’s multi-trillion-dollar IPO bell-ringing, an unparalleled realization of wealth began to unfold.

For early investors who had supported SpaceX through its long growth trajectory, this listing delivered historic returns. For instance, Google’s stake in SpaceX is now estimated to be worth over $100 billion. Hedge fund D1 Capital Partners’ holdings are valued at approximately $20 billion. Legendary investor Ron Baron, who participated in 27 rounds of SpaceX funding over the years, has seen his stake grow to about $12 billion. Meanwhile, prominent Silicon Valley venture capital firm Andreessen Horowitz’s stake is valued at approximately $1 billion.

American university endowment funds also emerged as significant beneficiaries of this wealth surge. For example, about 10% of the University of North Carolina System’s endowment fund had exposure to SpaceX. Washington University in St. Louis held SpaceX-related assets accounting for over 15% of its fund size, and Stanford University also held a substantial stake.

Beyond institutional investors, SpaceX employees also reaped considerable rewards. SpaceX currently employs approximately 22,000 individuals, alongside hundreds of former employees. According to an analysis by the investment platform Hill, roughly 400 current and former employees hold shares valued at over $100 million, becoming a new generation of billionaires.

While Elon Musk became the world’s first trillion-dollar individual, SpaceX COO Gwynne Shotwell and CFO Bret Johnsen are also expected to hold shares worth over $1 billion each. Antonio Gracias, a SpaceX board member and founder of Valor Equity Partners, holds shares potentially valued at around $68 billion, while fellow board member Luke Nosek’s stake is estimated to be approximately $5 billion.

More than 4,400 employees became millionaires in this IPO. From rocket welders and manufacturing engineers to administrative staff and cafeteria workers, many shared in the company’s growth dividends. According to The Wall Street Journal, many initially received stock when it was valued at less than $2 per share, a time when SpaceX hadn’t even achieved rocket reusability. As the company underwent multiple funding rounds, stock splits, and continuous valuation increases, the value of their holdings soared.

For example, former welder Juan Hernandez joined SpaceX in 2015 with an hourly wage of $28 and initially received about $10,000 in equity incentives. Although he sold some shares when the company was valued at approximately $36 billion, his retained equity is still worth around $880,000. Another former SpaceX engineer, who received stock incentives years ago, now holds shares valued at over $28 million.

However, many employees missed out on even greater appreciation by selling their holdings too early. The Wall Street Journal reported instances of individuals selling shares to repay a spouse’s student loans, using proceeds to buy vacation homes for parents, or investing funds into their own startup ventures. These practical choices meant they forgo tens or even hundreds of times their initial investment in wealth growth.

A Trillion-Dollar Space Story: Is It Overvalued?

A company still “burning cash” becoming the world’s most expensive IPO has inevitably sparked a fervent debate in the market about the “Musk premium” or “dream-to-earnings” ratio.

From a financial perspective, SpaceX is still far from a mature profitability stage. Its prospectus revealed a first-quarter revenue increase of 15% year-over-year, reaching $4.69 billion, but also a net loss of $4.28 billion for the same quarter. Since its inception in 2002, the company has accumulated approximately $41.3 billion in losses and frankly stated in its prospectus that it might not achieve sustained profitability in the future.

However, supporters argue that traditional profitability models are insufficient to gauge SpaceX’s true worth. In their view, SpaceX is not merely a rocket launch company but a multifaceted platform enterprise integrating satellite internet, artificial intelligence, and future space infrastructure. Its real value, they contend, lies in its growth potential over the coming decades.

For instance, tech analyst Daniel Newman suggests that “if investors take a five-year view, SpaceX will perform exceptionally well. An offering price of $135 per share might seem expensive a year from now, but looking back five years later, it will likely be considered quite cheap.” He revealed plans for a small initial purchase on SpaceX’s listing day to avoid missing the opportunity entirely due to short-term judgment errors, but also anticipates that more ideal entry points might emerge within the first 12 months post-listing.

Currently, Oppenheimer has initiated coverage on SpaceX with an “Outperform” rating, setting a 12-to-18-month price target of $190, representing approximately 40% upside from the $135 offering price. New Street Research also offered an optimistic assessment, providing a “Buy” rating and a $165 price target upon its initial coverage, corresponding to about 22% upside.

Furthermore, sources familiar with the matter indicated that SpaceX informed investors it had secured investment-grade ratings from three major bond rating agencies, which could help lower its financing costs for future capital raises post-IPO.

Yet, skepticism abounds in the market. Valuation guru Aswath Damodaran believes SpaceX is currently overpriced and stated he would not buy immediately, predicting a scenario similar to Facebook and Uber’s significant post-IPO corrections (which saw drops of over 50%). He advises patience, suggesting to wait for lower entry points, noting that while the AI business adds to SpaceX’s grand narrative, it also increases volatility, potentially pressuring short-term performance.

Veteran Wall Street commentator Jim Cramer posited that the primary risk for the SpaceX IPO lies not in undersubscription but in the potential for short-term investors who received allocations to cash out early, thereby amplifying stock price volatility.

Famed short-seller James Chanos asserted that SpaceX’s high-profile listing is driven more by investor enthusiasm for Musk and AI than by financial fundamentals, making it difficult to justify the company’s valuation based on any reasonable business assumptions. He characterized it as an IPO sustained by “hope and dreams.”

On one side lies the financial reality of colossal losses, and on the other, the grand imagination of stars and oceans. As a pioneer in the space economy, SpaceX has no direct precedents, and its future remains shrouded in uncertainty. With the multi-trillion-dollar bell now rung, the market has begun to price the space dream.

(The above content is an excerpt and reproduction authorized by partner PANews. Original link)

Disclaimer: This article is for market information purposes only. All content and views are for reference only, do not constitute investment advice, and do not represent the views and positions of BlockTempo. Investors should make their own decisions and trades. The author and BlockTempo will not be responsible for any direct or indirect losses incurred by investor transactions.