Bitcoin is currently consolidating around the $68,000 mark, igniting widespread calls for “buying the dip.” Many investors are asking: Is this a once-in-a-lifetime opportunity to enter the market? On-chain data suggests that while we might be closer to a “golden buying point” than at any time in the past three years, it’s still premature to definitively declare a market bottom.

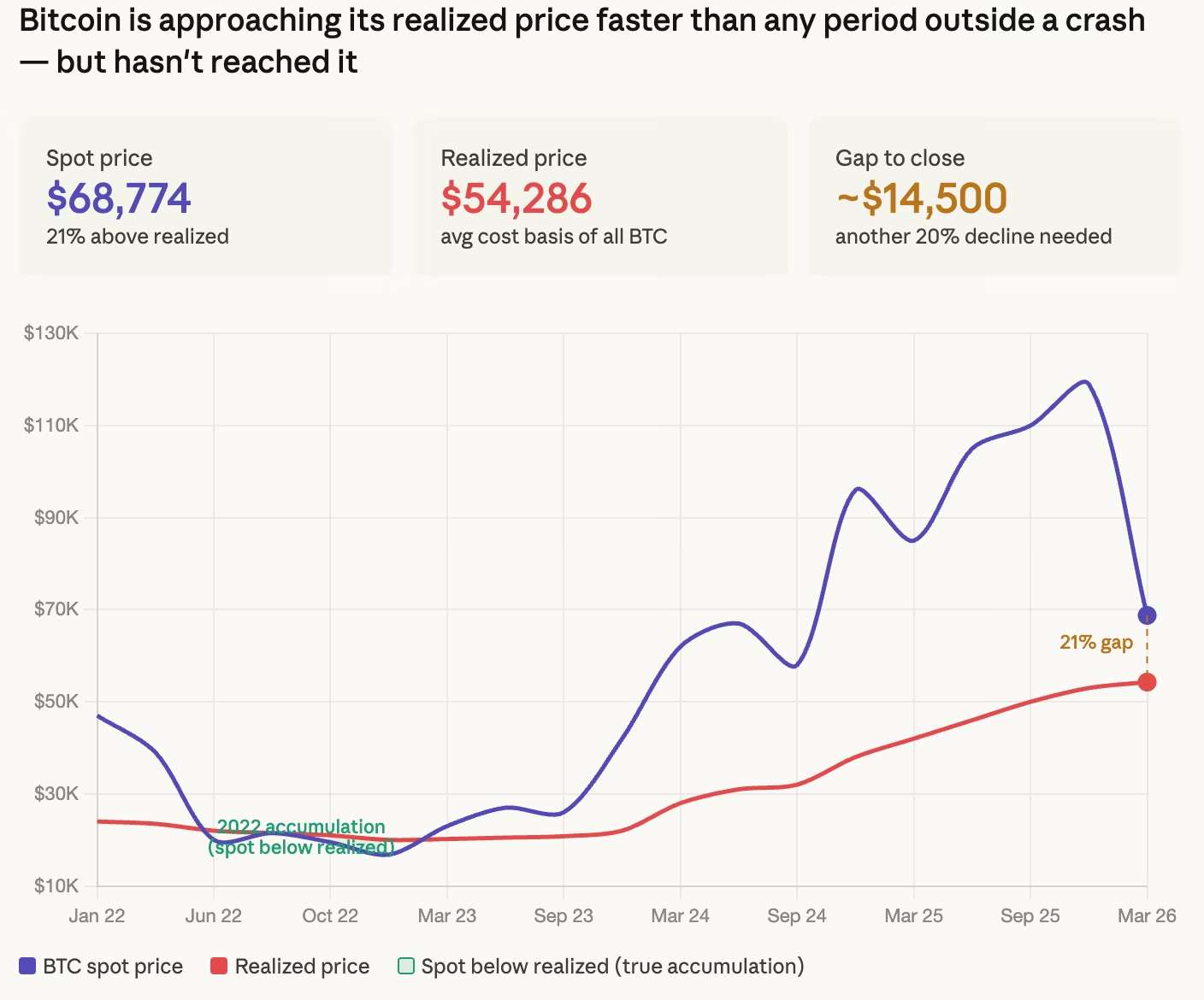

Data from CryptoQuant reveals that Bitcoin’s “Realized Price”—the average cost of all Bitcoin on the network based on its last transaction price—currently stands at approximately $54,286. In contrast, the spot price is $68,774, indicating a premium of about $14,500, or roughly 21% above the average cost basis.

Recalling the 2022 bear market, the true signal confirming a market bottom emerged when the spot price plummeted below the realized price. From June to October of that year, Bitcoin’s trading price consistently remained below the network’s overall average cost. During the most severe phase of the downturn, the spot price even dipped 15% below the realized price, precisely aligning with the absolute bottom of that cycle at around $15,500.

The infamous COVID-19 crash in early 2020 followed a similar script. Both these significant downturns were recognized as “Golden Accumulation Zones”—periods where major capital aggressively buys and accumulates assets at low prices. This was primarily because, at those times, the average holder across the network was experiencing losses. Historical patterns consistently show that boldly entering the market when the collective is in a state of loss often proves to be the most reliable and highest-probability strategy.

However, the current market landscape presents a different picture. With the market price still commanding a 21% premium over the average cost, the majority of holders are currently profitable, providing a substantial buffer. For Bitcoin to retrace to its realized price, it would need to fall approximately 20% from its current level, bringing it down to the $54,000 range.

Remarkably, the speed at which this gap is narrowing is astonishing. During Bitcoin’s significant rallies, the spot price premium relative to the realized price was as high as 120%. In a relatively short span, this gap has now narrowed to 21%. Excluding black swan events, this marks one of Bitcoin’s fastest convergences towards its realized price in history.

CryptoQuant analyst Oinonen recently suggested that Bitcoin has entered an “accumulation zone” similar to late 2022. However, a strict interpretation of the data definitions suggests this assertion might be premature. A clear look at the charts reveals that the 2022 accumulation zone was characterized by the spot price falling to or below the realized price. In contrast, the currently identified “bottom zone” still sees the spot price hovering significantly above this critical indicator, making the comparison somewhat tenuous.

Other on-chain signals also corroborate the view that the market has “not yet been thoroughly flushed out.” For instance, the “Coinbase Premium Index” recently dipped back into negative territory, indicating relatively weak buying pressure in the U.S. market and signs of cooling institutional demand.

Of course, this doesn’t preclude Bitcoin from staging a rebound from its current position. Over the past month, despite escalating tensions in the Middle East and heightened geopolitical risks, Bitcoin has demonstrated remarkable resilience, holding steadily within the $65,000 to $70,000 range. Furthermore, the Bitcoin spot ETFs attracted over $1 billion in inflows in March, signaling a robust and stable underlying buying base in the market.

Nevertheless, from the perspective of on-chain data, the “ultimate stress test” that truly challenges the market’s bottom line has yet to arrive. The widespread lament and capitulation of investors, a hallmark of true bottoms, have not yet occurred. And often, that is the genuine signal that heralds a super bottom.

Disclaimer: This article is for informational purposes only. All content and opinions are for reference only and do not constitute investment advice. They do not represent the views or positions of the author or BlockTempo. Investors should make their own decisions and transactions. The author and BlockTempo will not be held responsible for any direct or indirect losses incurred by investors’ transactions.