Bitcoin’s ‘Winter’ Lingers: K33 Research Sees Echoes of 2022 Bear Market Bottom

Bitcoin’s recent downturn has left many investors feeling the chill, with some declaring the return of a crypto winter. A new report from research firm K33 Research, released on Tuesday, suggests that while the market may be nearing a bottom, a significant breakthrough rally isn’t on the immediate horizon. The current market structure, according to K33, bears striking similarities to the tail end of the 2022 bear market.

Unpacking the “Market Mechanics Indicator”

Vetle Lunde, Head of Research at K33, highlights that the firm’s proprietary “Market Mechanics Indicator” reveals a strong resemblance between current Bitcoin data and the market conditions observed in September and November 2022. These periods were crucial phases where the previous bear market was approaching its floor. Key metrics analyzed include derivatives yields, open interest, ETF flows, and the U.S. yield curve.

However, Lunde cautions against expecting a rapid recovery. While these signals typically appear near market bottoms, they are often followed by prolonged periods of weak price performance and tedious sideways consolidation, rather than sharp bounces. Investor patience, he warns, will be severely tested.

Defensive Posturing in Derivatives and Spot Markets

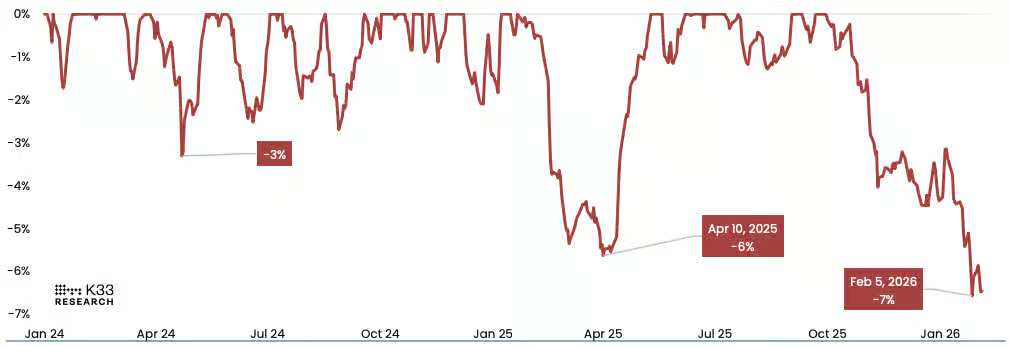

K33’s report notes that Bitcoin has retraced almost 28% since its January peak, with the derivatives market clearly reflecting a defensive stance. Funding rates have remained negative for 11 consecutive days, indicating a stronger demand for hedging over speculative upside bets. Concurrently, nominal open interest has fallen below 260,000 Bitcoins, suggesting investors are actively closing long positions and adopting a wait-and-see approach.

This structure, Lunde explains, implies a limited risk of short or long squeezes driven by derivatives in the near term. Instead, the market appears to be digesting the previous downtrend rather than preparing for a new directional breakout.

K33 emphasizes the high weighting given to derivatives data in its model, as these metrics provide the most real-time insight into genuine market demand for hedging or upward exposure. Negative yields signal an excess of hedging demand, while declining open interest suggests traders are unwinding positions rather than aggressively initiating new long or short bets.

A Slow Grind: Historical Precedent and Price Outlook

In highly similar market environments, K33’s historical analysis indicates an average 90-day return of approximately 3%. In less similar scenarios, returns were slightly negative. This suggests Bitcoin is more likely to enter a period of “slow progress and sentiment erosion” – a prolonged consolidation phase.

Vetle Lunde anticipates Bitcoin will trade within a range of $60,000 to $75,000. While current entry points may appear attractive, he stresses the necessity of patience. The transition from a “bear market bottom” to the “early stages of a bull market” is, he predicts, a lengthy psychological battle.

Cooling Activity and Institutional Caution

Following the recent sell-off, market activity has notably cooled. Bitcoin spot trading volume decreased by 59% week-over-week, and futures open interest has dropped to a four-month low. These behavioral patterns are historically common during phases where the market absorbs losses and gradually stabilizes.

Lunde adds that as market fluctuations converge and volatility normalizes, it reinforces the expectation of a “low-noise, low-stimulation” trading environment.

Institutional investors are also exhibiting caution. K33 points out that participation from institutional traders on the CME has been low, with yields and open interest remaining subdued. This indicates a lack of strong directional consensus among major players.

Furthermore, Bitcoin ETPs have seen cumulative net outflows of 103,113 Bitcoins since their peak in October last year. Despite Bitcoin’s price falling nearly 50% from its high, approximately 93% of institutional exposure positions have opted to “hold firm.” This suggests that while professional investors are de-risking, a full-scale retreat has not occurred.

Fear, Greed, and the Path to Recovery

On the sentiment front, the Crypto Fear & Greed Index recently plunged to a low of 5, signaling extreme market pessimism. However, Vetle Lunde warns that this indicator has limited accuracy in predicting future gains.

K33’s data supports this, showing that buying during “extreme fear” periods yielded an average 90-day return of only 2.4%. In stark contrast, buying during “extreme greed” periods saw returns as high as 95% over the same timeframe. This underscores that panic sentiment alone is not a reliable signal for a market rebound.

K33 concludes that Bitcoin’s current market conditions strongly mirror the end stages of previous bear markets, suggesting that downside risk may be gradually diminishing. However, a genuine recovery will likely require more time to materialize, with the market potentially replaying the “long and tedious” consolidation process witnessed after the 2022 bottom.

Disclaimer: This article is for market information purposes only. All content and views are for reference only and do not constitute investment advice. They do not represent the views or positions of the author or BlockBeats. Investors should make their own decisions and trades. The author and BlockBeats will not bear any responsibility for direct or indirect losses incurred by investors’ transactions.