MicroStrategy’s Bitcoin Accumulation Engine Stalls as STRC Preferred Stock Breaks Par Value Anchor

MicroStrategy, under the visionary leadership of Michael Saylor, has become synonymous with institutional Bitcoin adoption. Its innovative financing mechanism, particularly the issuance of STRC perpetual preferred stock, was once hailed as the bedrock of its relentless Bitcoin acquisition strategy. However, this meticulously crafted engine, designed to fuel a continuous cycle of Bitcoin accumulation, has recently hit a significant snag.

On April 14th, MicroStrategy’s STRC perpetual preferred stock experienced a critical downturn on Nasdaq, plummeting below its crucial $100 par value anchor to a low of $99.06. This de-anchoring was accompanied by a drastic reduction in trading volume, falling to just 47% of its usual levels, and the stock has since continued to trade in a discounted range.

The efficiency of STRC’s financing is directly tied to MicroStrategy’s ability to expand its Bitcoin reserves. A sustained dip below par value signals a temporary halt in the company’s primary financing conduit for acquiring more Bitcoin. As the world’s largest corporate holder of Bitcoin (a “Digital Asset Treasury” or DAT leader), a disruption to MicroStrategy’s capital-raising capabilities could significantly diminish the marginal buying pressure supporting the broader Bitcoin market, leaving it in a precarious position.

The Bitcoin Accumulation Engine: How STRC Was Designed

STRC was conceived to address a key challenge for Michael Saylor: how to consistently draw capital from traditional financial markets to purchase Bitcoin without diluting the voting power of MicroStrategy’s common shares (MSTR). The core design principle was to maintain the trading price of STRC near its $100 par value, thereby enabling the company to continuously raise funds through “At-the-Market” (ATM) offerings.

- If STRC’s price consistently traded below $100, the board would strategically increase the dividend, attracting income-seeking investors to stabilize and boost the price.

- Conversely, if the price rose significantly above $100, dividends would be maintained or lowered to optimize financing costs.

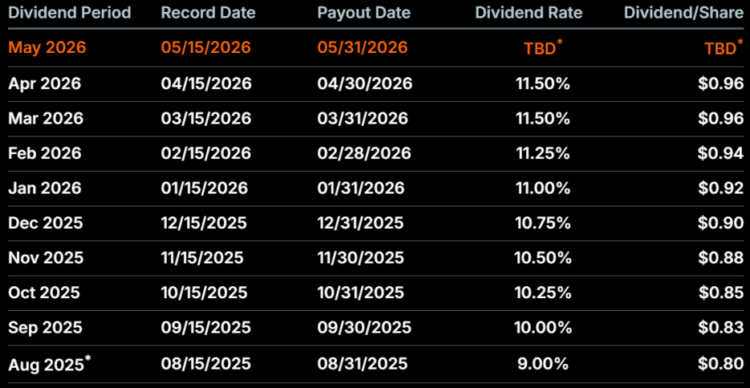

Initially launched with a 9% annualized dividend, STRC saw its yield steadily climb over seven consecutive months, eventually reaching an attractive 11.5%. This high, stable yield proved highly appealing to investors, ensuring STRC consistently traded above par. This mechanism allowed Saylor to effectively channel capital from traditional markets into the Bitcoin ecosystem, transforming it into sustained buying pressure.

Beyond traditional valuation metrics, Saylor introduced the “Bitcoin Gain” metric to underscore MicroStrategy’s value as a “Bitcoin-standard” enterprise. This innovative metric measures the percentage growth of Bitcoin holdings per common share, reflecting the company’s core mission.

MicroStrategy reported a 6.2% Bitcoin gain in Q1 2026, targeting an ambitious 9.5% for the full year. STRC was the strategic leverage tool for this goal: by issuing preferred stock with predictable financing costs, MicroStrategy could acquire Bitcoin, an asset with significant long-term appreciation potential. Saylor’s calculations suggested that as long as Bitcoin’s annualized growth surpassed 2.05%, common shareholders would continuously benefit.

For the better part of a year, this self-reinforcing cycle operated flawlessly: STRC issuance for financing → Bitcoin acquisition → Bitcoin price appreciation → increased stock market value → heightened demand for STRC → more capital raised for further Bitcoin purchases. STRC effectively functioned as a perpetual financing machine, consistently supplying the necessary capital for Saylor’s expanding Bitcoin empire.

The Anchor Snaps: Unpacking the De-Anchoring of STRC

The $100 par value was the critical lifeline for STRC’s financing flywheel. Its breach meant the immediate cessation of ATM offerings, effectively stopping the “money printing machine.” This de-anchoring event was the result of a powerful confluence of macroeconomic headwinds and deteriorating market sentiment.

The geopolitical tensions, particularly the conflict in Iran and its impact on shipping through the Strait of Hormuz, triggered a surge in crude oil prices. This, in turn, fueled inflation fears, pushing market expectations for a Federal Reserve interest rate cut further into the future, from mid-2026 to 2027. For STRC, a preferred stock with strong bond-like characteristics, a prolonged period of high benchmark interest rates significantly eroded the attractiveness of its 11.5% dividend, as risk-free rates became more competitive.

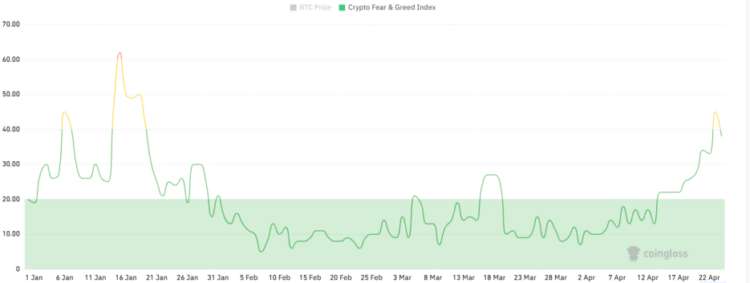

Simultaneously, the broader cryptocurrency market experienced a period of “extreme fear,” with the Fear & Greed Index plummeting to 9. Capital, previously seeking stable returns, began divesting from non-core assets, making the relatively illiquid STRC particularly vulnerable.

While the macro environment provided the external impetus, MicroStrategy’s dividend decision on April 1st served as the critical internal catalyst. The company announced it would maintain the 11.5% dividend but ended its seven-month streak of monthly increases. While MicroStrategy likely intended to signal stability and confidence that rates had peaked, investors, particularly the retail segment (comprising 80% of STRC holders), interpreted this differently. They saw it as a sign that the company’s financing capacity had reached its limit and perhaps even a loss of confidence in Bitcoin’s future price trajectory.

This abrupt halt in dividend increases shattered the prevailing investor expectation of “monthly rate hikes and stable prices above par.” A mass exodus of retail investors ensued, causing trading volume to collapse and the $100 par value anchor to break. The implications extended beyond MicroStrategy, impacting the entire Bitcoin market’s supply-demand dynamics.

With STRC trading below par, ATM offerings became economically unviable. Issuing new shares at a discount would only further depress the price, creating a detrimental feedback loop. Consequently, MicroStrategy was forced to halt new STRC issuances. Recent financing data confirms this, showing zero new STRC capital raised. MicroStrategy’s substantial purchase of 34,164 Bitcoins last week was reportedly funded by residual capital from previous financing rounds.

The temporary cessation of STRC financing means the Bitcoin market’s largest institutional buyer has paused its aggressive accumulation. This effectively removes an estimated $1-2 billion in weekly marginal buying pressure, leaving a noticeable void in the market.

MicroStrategy’s Strategic Counter-Move: Bi-Weekly Dividends and Asset Depth

Faced with the paralysis of its key financing tool, MicroStrategy swiftly announced a strategic maneuver to regain pricing power. On April 28th, the company will put a proposal to shareholders to increase STRC’s dividend payment frequency from monthly to bi-weekly.

This move is a calculated psychological play, primarily targeting retail investors. By shortening the dividend cycle, MicroStrategy aims to mitigate the typical price drop observed on ex-dividend dates (historically an average of 45 cents, requiring about 12 days for recovery). Bi-weekly cash flow returns are expected to significantly reduce reinvestment lag, making STRC more attractive to cash-flow-sensitive retail investors and income-focused funds. If approved, STRC would become one of the rare listed equity instruments globally to offer bi-weekly dividends.

Furthermore, to address accusations of its model resembling a Ponzi scheme, MicroStrategy proactively highlighted the robustness of its non-Bitcoin assets. The company disclosed approximately $2.25 billion in cash reserves, sufficient to cover preferred stock dividend obligations for about 30 months without resorting to new share issuance or Bitcoin sales. Its traditional business intelligence software segment also generates a healthy $320 million in annual gross profit, providing a crucial safety net even in extreme market conditions.

Navigating Controversy: Chronic Bleeding vs. Asset Accretion

Despite the backing of substantial Bitcoin reserves, STRC has consistently been a subject of debate among financial experts. Critics like Peter Schiff argue that since Bitcoin itself generates no income, STRC’s high dividends are inherently unsustainable, relying either on a continuous influx of new investors or by eroding common shareholder value.

Their “death spiral” hypothesis suggests: Bitcoin price drops → STRC price falls → financing capabilities diminish → inability to buy more Bitcoin to support its price → forced sale of Bitcoin to cover dividends → further Bitcoin price decline. While MicroStrategy’s proactive interventions could prevent a rapid “death spiral” akin to UST, the risk of “chronic bleeding” remains – a self-reinforcing downward trend that slowly erodes value.

MicroStrategy, however, vehemently defends its model, asserting that STRC is predicated on Bitcoin’s long-term appreciation as a deflationary asset. They argue that as long as Bitcoin’s appreciation rate outpaces the cost of financing, preferred stock issuance creates a positive “asset accretion” effect, rather than merely shuffling funds. The company highlights that its current Bitcoin reserves cover preferred stock principal more than 4.3 times, implying that STRC would only face genuine insolvency if Bitcoin’s price plummeted below approximately $18,000.

Yet, capital markets are often driven by sentiment, reacting well before fundamental thresholds are reached. Panic in the Bitcoin market could trigger a collapse in STRC’s secondary market price long before the $18,000 insolvency point.

A crucial point often overlooked by investors is STRC’s underlying legal classification. While it carries a nominal par value and fixed dividends, it is legally an equity security, not a bond. This means it lacks the mandatory principal repayment obligations and fixed maturity date of a bond. In the hierarchy of capital liquidation, STRC ranks behind debt instruments like convertible bonds and secured debt.

Conclusion: A Wake-Up Call for the Bitcoin Standard

STRC’s fall below its $100 par value is a significant development, marking a crucial test for Bitcoin’s maturation as a digital asset treasury. For investors, it serves as a stark reminder: in the volatile crypto market, no “anchoring” mechanism is absolute. Liquidity remains the paramount principle for survival.

While STRC’s 11.5% yield is undeniably attractive, it inherently carries credit risk and the potential for a liquidity trap. As MicroStrategy continues its ambitious journey towards a “Bitcoin standard,” the de-anchoring of STRC is likely a temporary setback. The ultimate success of this long-term endeavor hinges not just on scale, but crucially, on ensuring the structural resilience and robust health of its financing mechanisms.