Source: McKinsey & QED Investors

Author: Yuliya, PANews

Editor’s Note: For years, the fintech landscape was defined by compelling narratives and aggressive customer acquisition strategies fueled by substantial investment. Today, that paradigm has fundamentally shifted.

A groundbreaking report from McKinsey and QED Investors declares that the fintech industry has transitioned beyond its “wild growth” phase, entering a “Fifth Era” characterized by a relentless focus on profitability and stringent compliance. While fintech currently accounts for just 4% of the global financial market, generating an impressive $650 billion annually, its revenue growth rate is a remarkable 3.5 times that of traditional banks. This sector is poised to remain a fertile ground for the emergence of multi-hundred-billion-dollar giants in the coming years.

(This report was collaboratively authored by Jon Steitz, Max Flötotto, Uzayr Jeenah, Vikram Iyer, and Edward Allanson from McKinsey’s Financial Services practice, alongside Nigel Morris, Nick Gasbarro, Amias Gerety, and Adams Conrad from QED Investors.)

Fintech at a Glance: Key Insights and Projections

- Market Scale & Outlook: Fintech revenue is projected to reach $650 billion by 2025, representing 4% of total financial services revenue. Sustaining recent growth trajectories, this figure could soar to $2 trillion by 2030, capturing 9% of the market.

- Investment Surge: Annual capital deployed into fintech has increased by over 40% since 2023.

- Elite Valuations: Five companies are currently approaching “hectocorn” status, valued at nearly $100 billion each.

- Fintech-Led M&A: Over half of all fintech acquisitions are initiated by other fintech firms, rather than traditional institutions or private equity sponsors.

- Digital Assets Landscape: Stablecoin transaction volumes are expected to hit $35 trillion by 2025. However, only 1% ($390 billion) is attributed to “real payments,” with the majority linked to trading and arbitrage.

- Regulatory Shift: The U.S. saw 21 bank charter applications in 2025, surpassing the combined total of the previous four years.

- Evolving Business Models: “Horizontal” software companies, which empower traditional institutions with digital solutions, now account for 13% of fintech revenue. These enablers are growing 25% faster than direct competitors.

I. Industry Dynamics: Rapid Growth Amidst Regional and Vertical Specialization

By 2025, the global fintech market generated approximately $650 billion in revenue, marking a 21% year-over-year increase from 2024 and a 23% compound annual growth rate (CAGR) over the past four years. This growth significantly outpaces the $15 trillion traditional financial services sector, which saw a 6% CAGR. Despite its rapid expansion, fintech still holds only about 4% of total financial services revenue, highlighting immense potential for future market penetration.

Regional Diversification: Latin America Leads the Charge

- North America: The largest market, generating $310 billion in revenue. Growth is increasingly extending into capital markets (21%) and insurance (15%).

- Latin America: The fastest-growing region, with $60 billion in revenue and an 8% penetration rate. It has achieved a 40% CAGR over the last five years, with its lending sector experiencing a remarkable 50% annual surge since 2021. The market is highly concentrated, with the top three players—Mercado Pago, Nubank, and PagBank—commanding 48% of the region’s total revenue.

- Asia-Pacific: Accounts for $150 billion in revenue (3% penetration). Growth has moderated from 23% to 15% due to regulatory influences. The revenue focus has shifted from lending (down to 29%) towards payments (up to 40%).

- Europe: Generates $110 billion in revenue (2.6% penetration). This market remains the most fragmented, with the top three companies—Adyen, Klarna, and Revolut—holding less than a 20% combined share.

Vertical Specialization: Payments Dominates, Insurtech Accelerates

- Payments: The largest vertical, contributing $250 billion in revenue (18% YoY growth from 2024-2025, 19% penetration). Leaders like PayPal and Stripe are effectively capturing the fastest-growing global transaction flows, including digital, embedded, cross-border, and platform-based commercial payments.

- Lending: Total revenue stands at approximately $120 billion (19% YoY growth), primarily concentrated in underserved markets such as Latin America, Asia-Pacific, and Africa. Global innovators like Nubank and WeBank are scaling by seamlessly embedding credit solutions into digital platforms. This sector exhibits the lowest concentration, with the top three firms accounting for only 16% of total revenue.

- Insurance & Capital Markets: Each vertical generates roughly $80 billion. While growing rapidly, they are starting from a lower base. Insurtech is experiencing the fastest growth (up 37% since 2021), yet its overall penetration remains below 1%.

- Customer Segments & Sub-sectors: B2C services comprise 47% of the market, while B2B accounts for 41%. In wealth tech, a “winner-take-all” dynamic is evident, with major cryptocurrency platforms like Bakkt, Binance, and Coinbase collectively capturing approximately 30% of the sector’s total revenue.

Capital Markets: A “Barbell-Shaped” Investment Landscape

- IPO Resurgence: 2025 saw 31 new listings, raising nearly $14 billion (a four-fold increase from 2024) and representing 12% of the total market capitalization of the top 100 global IPOs. Notable examples include Klarna (raised $1.3B / valued $11B), Circle (raised $1B / valued $20B), and Chime (raised $800M / valued $11B). The total market capitalization of listed fintech companies reached a record high of $850 billion across 202 firms.

- Investment Polarization: Capital is increasingly concentrating at the extreme ends of the funding spectrum. Late-stage scaling deals witnessed a 22% annual increase, while early-stage VC now comprises 37% of investments. Conversely, the share of mid-stage growth equity capital has plummeted from 45% in 2019 to just 25%.

- Giant Expansion: Companies like Revolut, Robinhood, and Stripe are nearing the coveted $100 billion valuation mark. Stripe, in particular, is making aggressive inroads into the digital asset domain through strategic acquisitions such as Bridge and Privy.

Customer Trust: Fintech Surpasses Traditional Finance

For the first time, McKinsey’s 2025 Retail Banking Survey reveals that customers place greater trust in fintech companies than in traditional banks. Consumers widely perceive fintech firms as more innovative, offering superior fee transparency, and delivering better overall value. On average, fintech companies achieve a Net Promoter Score (NPSSM) 2.5 times higher than their traditional counterparts, often scoring above 50 or even 70 points.

II. Four Transformative Trends Shaping Fintech’s Future

Trend One: AI as a Catalyst for Fintech Revolution

Artificial Intelligence is fundamentally reshaping the economics of the industry in four critical ways:

- Commoditization: Slashing product development cycles from years to mere weeks.

- Democratization: Making sophisticated financial tools accessible, such as April Tax Solutions embedding complex tax logic or Midas offering affordable wealth advisory.

- Unbundling: Breaking down traditional financial product packages.

- Disintermediation: Removing intermediaries in financial processes.

- Giants’ Strategic Pivot: Interestingly, established players like Coinbase, Nubank, Revolut, and Robinhood are leveraging AI to move in the opposite direction, aggregating products and using their scale to become central intermediaries for horizontal fintech solutions.

- Predicting the Winners:

- Pioneering Traditional Institutions: Early adopters of AI, both internally and client-facing, are projected to see their tangible return on equity (ROE) increase by up to four percentage points.

- “AI Second” Disruptors: Companies with deep domain expertise, proprietary data, or established distribution channels will gain a significant competitive edge by using AI to accelerate product development.

- Current AI Adoption: Fintech firms are boldly deploying AI customer service agents such as Decagon, Lorikeet, and Sierra. Traditional institutions that lag in adoption and scaled companies relying solely on outdated technological moats face an existential threat.

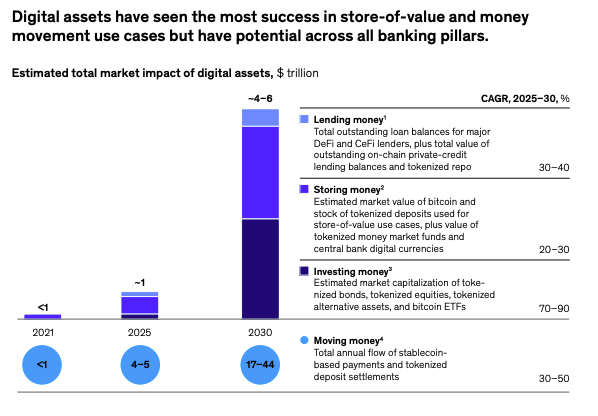

Trend Two: The Unstoppable Digital Asset Wave

After a decade of experimentation, digital assets are shedding their speculative image and evolving into investable infrastructure for mainstream financial institutions. The period of irrational exuberance from 2020-2022 has concluded, shifting market focus towards stablecoins and tokenized deposits. These innovations are poised to fundamentally transform money transfer, storage, lending, and investment, with all segments anticipating high double-digit growth by 2030.

- Bitcoin’s Role: Increasingly viewed as a viable alternative to both fiat currency and gold. As of Q1 2026, over 60% of Bitcoin has been held in wallets for more than a year, and its market penetration now represents approximately 3% of the global investable gold value.

- Stablecoins: With a current total issuance of $300 billion and $40 trillion in circulating value, stablecoins are projected to reach a market capitalization of $2 trillion to $4 trillion by 2030 (a 40% CAGR). Despite annual transaction volumes reaching $35 trillion, only 1% ($390 billion) represents genuine end-user payments; the remainder is largely composed of trading and arbitrage activities. Real-world applications include: global remittances ($90 billion, less than 1% of the global $100 trillion market), B2B payments ($226 billion), and capital market settlements ($80 billion, 0.01% of the global $200 trillion market). Furthermore, significant demand is emerging in developing markets (e.g., Argentina, Nigeria) seeking protection against local currency volatility.

- Tokenized Deposits: Effectively address the “cash leg” bottleneck in institutional settlements. JPMorgan’s JPMD and Kinexys (processing $2-3 billion daily), along with Citi Token Services (expected to support $100-140 trillion in flow by 2030), are spearheading this transformative trend.

- RWA (Real World Asset) Tokenization: Expected to reach a staggering $2 trillion by 2030. Major players like BNY Mellon and Goldman Sachs are integrating digital asset custody directly into their core platforms.

- Ecosystem Convergence: Klarna and PayPal have developed various payment stablecoins; Stripe (Bridge) is deploying stablecoin-enabled cards in over 100 countries; Visa and Mastercard are directly settling USDC; and AI agents are even beginning to utilize stablecoin-based micropayments for autonomous procurement of computing resources, heralding an era of programmable money-driven machine commerce.

Trend Three: The Race for Licenses (Embracing Regulatory Moats)

Fintech companies are no longer pursuing regulatory arbitrage; instead, they are proactively seeking bank licenses. This strategic shift positions licenses as a vital tool to access cheaper capital, expand product offerings, bolster customer trust, and solidify competitive moats.

- Key Data: In 2025, the U.S. saw 21 new charter applications, with approval times significantly reduced by 40% (e.g., Paycom took 421 days, while Erebor Bank secured approval in just 125 days).

- Prominent Players: This trend includes industry leaders such as Nubank, Circle (First National Digital Currency Bank), Stripe (Bridge), Fidelity, PayPal, Monzo, Zilch (following its acquisition of AB Fjord Bank), Revolut, Flutterwave, KakaoBank, and Airwallex.

- Potential Risks: Obtaining a license brings companies under direct regulatory scrutiny. Furthermore, their valuation logic may undergo a re-evaluation, potentially shifting from high-premium tech stock multiples to more traditional bank price-to-book multiples.

Trend Four: The Ascendance of “To B” Fintech

“Horizontal” fintech companies—those that do not offer direct consumer services but instead empower traditional institutions with digital software and infrastructure—are attracting a disproportionate share of investment. Illustrative examples include Omilia (AI solutions), Vitesse (claims digitalization), and Alloy/Footprint (compliance automation).

- Market Impact: This model already accounts for 13% of the industry’s total revenue. In the UK insurtech sector, funding for horizontal enterprises surged from 25% in 2021 to a remarkable 91% in 2024.

III. New Strategies for Success and Institutional Adaptation

Four Defining Characteristics of Future Winners

- Sustainable Economics: The era of “growth at all costs” is over. Future winners must demonstrate both high growth and robust unit economics. As Raman Bhatia of Starling Bank aptly states, “Technology barriers are falling, but business model barriers are rising.”

- Distribution & Trust: In a landscape where AI makes product replication effortless, enduring customer relationships and deeply accumulated trust represent the ultimate competitive moats.

- Superior Product Quality: Success demands a tangible advantage in terms of economics, speed, and risk management, moving beyond mere user interface enhancements. Justin Basini of ClearScore emphasizes that competitive advantage is increasingly tied to fundamental product superiority.

- Risk & Resilience: Compliance capabilities are emerging as a core differentiator. Dima Kats of Clear Junction posits, “The best investment a fintech company can make right now might be in compliance.”

Strategic Responses for Traditional Institutions

- Invest & Acquire: Build defensive positions through strategic capital deployment. JPMorgan, for instance, invested nearly $18 billion in technology in 2025. Visa has invested in or acquired over 50 companies and forged approximately 90 partnerships in the past five years.

- Reinvent & Modernize: Rapidly update core legacy systems by harnessing the power of AI and innovations from horizontal fintech providers.

IV. Forecast: Six High-Growth Opportunities on the Horizon

- Digital Asset Infrastructure & Networks: With the implementation of foundational legislation like the “GENIUS Act,” the focus will shift to core infrastructure: wallets, on/off-ramps, compliance tools, and programmable settlement layers.

- Agent AI for Financial Services: Targeting the multi-hundred-billion-dollar contact center, operations, and compliance cost pools by delivering automated, high-ROI solutions.

- Advanced Data Infrastructure: Leveraging open banking, real-time payments, and alternative data sources (e.g., payroll, rent) to revolutionize credit and risk decision-making.

- AI-Driven Wealth Advisory: Unlocking the largest underserved market by catering to the mass affluent segment with assets between $100,000 and $1 million, as exemplified by Robinhood’s cross-sector expansion.

- Horizontal Insurtech: Utilizing AI to unlock unstructured data (e.g., claims notes, satellite imagery) to enable personalized, real-time risk pricing.

- Identity & Trust Infrastructure: Building a universal, portable KYC/KYB/AML compliance layer to eliminate the industry’s most expensive and redundant pain points.

*Risk Warning: Scaled companies relying solely on technological barriers established over the past 5-10 years, as well as deposit-taking fintechs dependent on interest rate differentials, will face significant survival pressure amidst widespread AI adoption and intense high-interest competition.

(The above content has been excerpted and reproduced with permission from our partner PANews. Original Article Link)

Disclaimer: This article is provided for market information purposes only. All content and views are for reference only, do not constitute investment advice, and do not represent the views and positions of BlockTempo. Investors should make their own decisions and trades. The author and BlockTempo will not bear any responsibility for direct or indirect losses resulting from investor transactions.