Crypto Miners’ AI Pivot: From Bitcoin Blocks to High-Performance Compute

By Nancy, PANews

As the cryptocurrency market continues its protracted downturn, crypto mining companies are facing increasingly severe existential pressures. In a strategic move to unlock new growth avenues, a growing number of miners are rapidly transitioning into the artificial intelligence (AI) sector. This transformative narrative has swiftly captured the attention of capital markets, propelling many mining stocks to significant gains, with some even reaching new all-time highs.

While AI operations inject a potent dose of growth potential into mining firms, they also demand immense capital expenditure, continuous investment, and a prolonged return cycle. This shift is pushing miners into yet another intense funding battle. At a time when traditional mining profitability remains under considerable strain, this high-stakes gamble on AI transformation is rigorously testing miners’ financial resilience and execution capabilities.

Stock Performance Soars: Miners’ Valuations Enter a New Era of Differentiation

Crypto miners are rapidly evolving into the compute landlords of the AI era. As the profitability of Bitcoin mining dwindles, pushing some firms into the red, the explosion of AI has fueled an unprecedented surge in demand for data centers, power resources, and GPU compute capacity globally. Consequently, a growing number of miners are accelerating their pivot towards AI infrastructure, seeking a vital new growth trajectory.

For these companies, this transition comes with inherent advantages. For years, to meet the demands of large-scale mining operations, miners have accumulated extensive power resources, land reserves, substation access capabilities, and mature heat dissipation and cooling systems – all critical assets. Compared to building data centers from scratch, miners can rapidly enter the AI infrastructure market by simply upgrading and repurposing existing facilities, thus catering to AI compute demand at lower costs and in shorter timeframes.

Since last year, the pace of miners’ AI transformation has markedly accelerated. Some firms have decisively de-emphasized or even exited traditional mining, fully committing to AI compute and data center operations. Others maintain a portion of their mining activities but are progressively reallocating resources and capital expenditure towards AI. Today, several mining companies have emerged as significant players in AI infrastructure development.

Looking at the timeline, early movers like CoreWeave, Applied Digital, and Bitdeer began deploying AI compute and data center operations as early as 2022-2023. More recently, Iris Energy, Terawulf, Hut 8, Riot Platforms, and Bitfarms have embarked on comprehensive infrastructure expansion starting in 2025.

Market sentiment strongly validates the AI transformation narrative, as reflected in stock performance. The average year-to-date gain for 11 tracked mining firms stands at an impressive 75.97%, significantly outperforming Bitcoin over the same period, with many reaching new historical highs post-transition. Bitfarms (129.62%), Hut 8 (131.87%), Terawulf (118.68%), and Riot Platforms (93.71%) have been particularly strong performers, benefiting immensely from this re-evaluation of AI infrastructure assets.

However, a clear divergence in market capitalization is emerging. CoreWeave, a prime example of successful transformation, boasts a market cap of $62.855 billion, far exceeding its peers and setting a new industry valuation benchmark. Iris Energy, Terawulf, Hut 8, Applied Digital, and Riot Platforms form a second tier with market caps ranging from $10 billion to $20 billion. Meanwhile, MARA Holdings, Core Scientific, Bitdeer, CleanSpark, and Bitfarms remain in the sub-$5 billion range. This stratification stems not only from first-mover advantage but also from the market’s differentiated pricing based on each miner’s AI strategy execution, client relationships, and data center deployment progress.

From a fundamental perspective, most miners are still in the heavy investment phase of their AI transition. While many have reported revenue growth in their latest quarterly earnings, overall profitability remains under pressure. On one hand, the volatility of crypto asset portfolios drags down earnings. On the other, the massive capital expenditure required for AI data center construction—including power expansion, foundational infrastructure, and GPU procurement—is driving operating costs steadily upward, leaving many miners in a state of unprofitability. Despite these widespread performance pressures, the substantial rise in stock prices indicates that the market’s focus is not on short-term earnings but on the long-term growth potential of these miners as next-generation compute infrastructure operators.

The Escalating Survival Battle: AI Emerges as a Critical Lifeline

The prolonged slump in the Bitcoin market is making the operating environment for miners increasingly challenging.

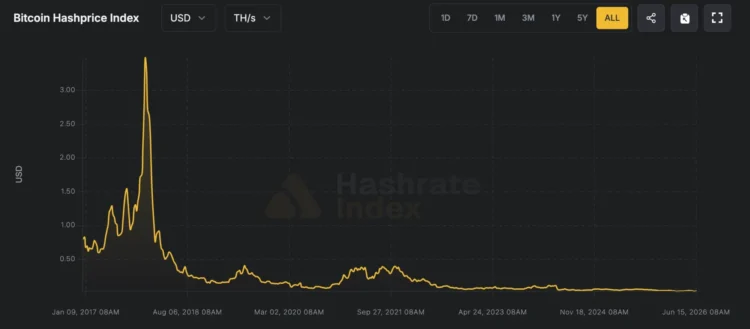

According to Capriole Investments data, as of June 18, the average Bitcoin production cost was approximately $63,707, with electricity alone accounting for around $50,965. This leaves miners with a slim profit margin of just 17.45%, which has contracted by 47.8% over the past 30 days. Concurrently, the Luxor Hashrate Index reported that as of June 18, the daily reward for 1 TH/s of compute power had fallen to $0.032, a significant drop from $0.053 in the same period last year.

With mining revenues continuously shrinking, many miners are forced to sell Bitcoin holdings to maintain cash flow, further intensifying the pressure on smaller operations. This dynamic is accelerating the concentration of mining resources among top-tier players. Currently, Foundry USA, AntPool, and F2Pool collectively command 59% of the global hashrate market share, a notable increase from the 44% held by the top three Bitcoin mining pools in 2022.

Despite the downturn in traditional mining, the explosive growth in AI data center demand is prompting a re-evaluation of miners’ intrinsic value. VanEck, in a recent research report, highlighted that miners’ most valuable assets are not their mining rigs, but rather their power resources, substation access capabilities, land reserves, and data center infrastructure—precisely the core resources currently most scarce in the AI industry. Given that AI clients are willing to pay significantly higher electricity rates and rental fees than traditional mining operations, AI infrastructure is poised to become the primary growth engine for mining companies over the next decade.

A report by Bernstein reveals that hyperscale cloud providers, AI cloud service providers, and chip companies have already announced over $90 billion in AI infrastructure partnerships, involving approximately 3.7 GW of power capacity. The pursuit of power resources has become central to AI infrastructure competition, with Bitcoin miners collectively controlling over 27 GW of planned power capacity. In certain regions of the United States, securing new 1 GW power access can take up to 50 months, making existing mining sites crucial hubs for AI data center expansion.

Navigating the AI Transition: Hurdles and Strategic Imperatives

However, the path to AI transformation is far from easy. VanEck notes that the market is still in the early stages of this transition, with enterprise valuations primarily based on Gross Energized Power. Miners with signed AI leases generally command higher valuation premiums, while projects merely in the planning phase struggle to gain market recognition. In the future, industry valuation logic will gradually shift from “power capacity” to “project delivery capability,” eventually returning to core metrics such as cash flow, return on capital, and tenant quality. With only about 25% of contracted capacity delivered to date, the ability to complete AI data center construction on time and within budget will be a critical determinant of enterprise valuation.

VanEck also emphasizes that the quality of AI tenants will directly impact miners’ valuation levels. Hyperscale cloud providers like Microsoft, Amazon, and Google bring more stable cash flows and lower financing costs, whereas smaller GPU cloud service providers correspond to higher operational risks and capital costs.

The enormous capital investment required for this transformation is also rigorously testing miners’ financial strength. VanEck estimates that miners transitioning to AI infrastructure face a short-term financing gap of approximately $50 billion, with long-term capital requirements potentially reaching $221 billion.

Under immense financial pressure, many miners have initiated various fundraising strategies. For instance, Iris Energy, TeraWulf, Bitfarms, and CleanSpark are raising capital through convertible bonds, leveraging lower coupon rates and future equity conversion potential to attract investors. Meanwhile, Core Scientific, Terawulf, MARA, Bitdeer, and Riot Platforms have opted to sell or even liquidate portions of their Bitcoin reserves to continuously fund their AI pivot.

Furthermore, many miners are securing future revenue by signing long-term AI or High-Performance Computing (HPC) contracts. This strategy helps them obtain project financing support and reduce overall operational risk. Examples include CoreWeave’s $6 billion AI cloud services partnership with Jane Street, IREN’s $9.7 billion AI cloud computing contract with Microsoft, Hut 8’s $9.8 billion data center lease agreement, and Bitdeer’s collaboration with Norway’s DCI to build the nation’s largest AI data center project.

For mining companies, AI undeniably offers a development path with far greater imaginative potential than traditional mining operations. However, this transformation is not a simple switch from mining to selling compute power; it is, at its core, a protracted competition centered on capital, resources, and execution capabilities.