Author: Nancy, PANews

MicroStrategy’s Pivotal Shift: Selling Bitcoin to Navigate Mounting Financial Pressures

Just over a month ago, MicroStrategy (often referred to as “Strategy”) made headlines with a modest sale of 32 Bitcoin (BTC). While the scale was minor, it sent ripples through the market, causing both Bitcoin’s price and MSTR stock to dip. Now, the company has executed a far more substantial move, offloading 3,588 BTC at a reported loss exceeding $55 million. This hundredfold increase in selling volume, however, has been met with a surprisingly subdued market reaction.

Indeed, facing an annual dividend bill exceeding $1.7 billion and a decelerating capital-raising “flywheel,” the world’s largest corporate Bitcoin holder appears to be bidding farewell to its staunch “buy-only” ethos. Instead, MicroStrategy is entering a defensive phase, prioritizing cash flow and liquidity above all else.

MicroStrategy’s Bitcoin Divestment: Hodling Model Confronts Payment Pressures

On July 5th, Michael Saylor once again updated MicroStrategy’s Bitcoin holdings tracker. Traditionally, such disclosures were swiftly followed by announcements of further BTC acquisitions. However, this time, even as Bitcoin prices showed signs of recovery, the market received news not of continued accumulation, but of MicroStrategy’s first large-scale Bitcoin divestment.

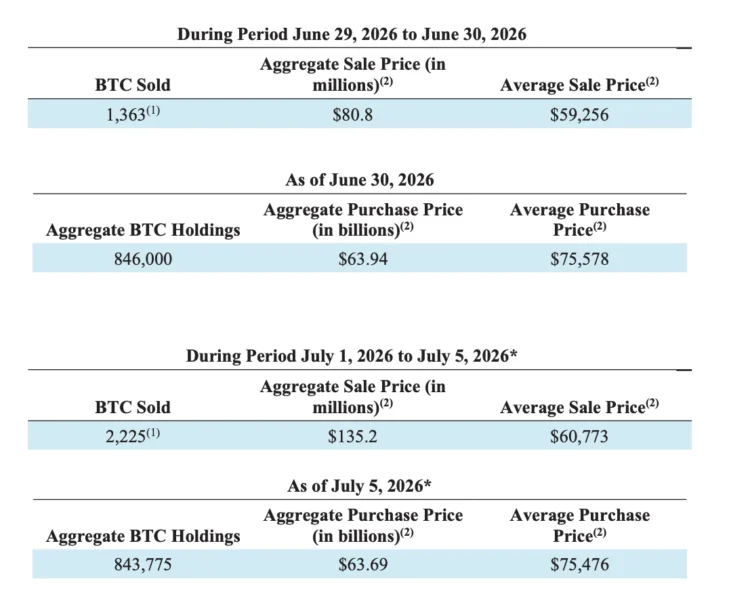

According to the latest revelations, MicroStrategy cumulatively sold 3,588 BTC between June 29th and July 5th, generating approximately $216 million in proceeds. Specifically, 1,363 BTC were sold from June 29-30 at an average price of roughly $59,256 (totaling approximately $80.8 million), followed by the sale of 2,225 BTC from July 1-5 at an average price of about $60,773 (totaling $135.2 million).

The primary use of these funds is to cover preferred stock dividends, including quarterly payments for STRF, STRE, STRK, and STRD, as well as the full June dividend for STRC. A portion of the proceeds will also bolster the company’s U.S. dollar reserves, which now reportedly cover approximately 17.4 months of dividend expenditures.

Following the announcement, Bitcoin experienced a brief dip before recovering its losses. Similarly, MicroStrategy’s stock (MSTR) saw an intraday decline but subsequently rebounded to erase its initial drop.

This isn’t MicroStrategy’s inaugural Bitcoin sale. On June 1st, the company sold 32 BTC, marking the first deviation from its long-standing “buy-only” policy since 2022. That initial, symbolic sale triggered an immediate plunge in Bitcoin’s price, a significant drop in MSTR stock, and an accelerated fall below par for STRC preferred shares, briefly sparking market panic.

In stark contrast to that initial foray, the recent sale of 3,588 BTC represents a more than hundredfold increase in scale and constitutes a genuine “loss-making” transaction. Based on MicroStrategy’s average holding cost of approximately $75,651 per BTC, this latest sale incurred an estimated loss of $55.45 million. The smaller June sale, notably, was executed at a price still slightly above the company’s cost basis.

The fundamental driver behind this surge in selling volume is the relentless escalation of dividend payment pressures.

Since its inception, MicroStrategy has consistently raised the dividend rate for its STRC preferred shares. This not only reflects evolving market perceptions of risk but also signifies a growing burden of fixed cash outflows for the company. Recently, MicroStrategy further intensified this pressure by transitioning STRC to a semi-monthly dividend mechanism and increasing its annual dividend rate to 12%.

Considering the current total notional amount nearing $10.49 billion, STRC alone demands approximately $1.258 billion in annual cash dividends. When factoring in other preferred shares, MicroStrategy’s total annual dividend expenditure now stands at an estimated $1.763 billion. Under the assumption of no external financing and neutral cash flow from its traditional software business, MicroStrategy’s current $2.55 billion in U.S. dollar reserves can only cover approximately 24.3 months of STRC dividend payments.

From a capital allocation perspective, this partial Bitcoin divestment appears to be a more pragmatic and certain capital optimization decision for MicroStrategy at this juncture. Currently, STRC trades around $88.5, showing a significant recovery from its lows but still some distance from its $100 par value target.

According to Wall Street investment bank Cantor, MicroStrategy’s paramount objective is to restore STRC to its $100 par value. This is deemed crucial for reigniting the Bitcoin acquisition engine and stabilizing the company’s overall capital structure. MicroStrategy has explicitly stated its goal to maintain STRC’s long-term trading price within the $99-$100 range, supported by strategies such as variable dividend rates, continuous augmentation of U.S. dollar reserves, enhancement of Bitcoin’s credit rating, removal of convertible bonds, implementation of stock buybacks, and product feature upgrades.

For MicroStrategy, in a period where its capital market financing capabilities are not fully restored, prioritizing dividend commitments and bolstering U.S. dollar reserves takes precedence over further Bitcoin accumulation. This approach aims to fortify market confidence in its preferred shares and overall capital structure. Grayscale also posited that MicroStrategy’s Bitcoin sale should help restore market confidence in its financing framework, potentially contributing to a more sustainable Bitcoin price floor and mitigating tail risks.

Facing Billions in Unrealized Losses, MicroStrategy Enters Defensive Mode

Despite its considerable size, the sale of 3,588 BTC represents only about 0.42% of MicroStrategy’s total holdings of 843,775 Bitcoin. This suggests that the company’s core strategic commitment to long-term Bitcoin ownership remains largely unshaken. As of now, MicroStrategy still holds over $53 billion worth of Bitcoin, solidifying its position as the world’s largest corporate Bitcoin holder.

However, the persistent downturn in Bitcoin’s price has undeniably intensified MicroStrategy’s operational and financing pressures. Based on an average holding cost of approximately $75,476 per BTC, MicroStrategy currently faces an estimated $11.34 billion in unrealized losses, representing a floating loss of nearly 18%.

More significantly, the market’s valuation methodology for MicroStrategy is undergoing a fundamental transformation.

In the past, investors were willing to pay a substantial premium for MicroStrategy’s compelling growth narrative – a story built on continuous financing and relentless Bitcoin accumulation, creating a self-perpetuating capital flywheel. However, with Bitcoin’s price retraction, the narrowing premium on MSTR stock, and the shattering of the “never sell Bitcoin” market expectation, investors are now re-evaluating MicroStrategy’s business model, effectively applying the brakes to its once-unstoppable capital flywheel.

In response to this evolving landscape, MicroStrategy recently unveiled its Digital Credit Capital Framework. This framework aims to maintain its long-term Bitcoin holding strategy while simultaneously enhancing digital credit securities, improving liquidity, and supporting long-term shareholder value.

Under this new framework, MicroStrategy will establish dedicated U.S. dollar reserves specifically for preferred stock dividends and debt interest payments. Furthermore, it has authorized a $2 billion share repurchase program, allocating $1 billion for preferred stock buybacks and another $1 billion for Class A common stock buybacks. The board has also approved a Bitcoin monetization plan of up to $1.25 billion, intended to replenish U.S. dollar reserves, cover dividends and interest, or fund share repurchases.

This signifies a profound shift for MicroStrategy: from a model heavily reliant on continuous financing for expansion, it is transitioning towards a proactive capital management approach that prioritizes liquidity management, capital structure optimization, and cash flow stability. While retaining its core Bitcoin position, MicroStrategy aims to build more robust cash reserves, providing a greater safety buffer against future market volatility.

However, market opinions on this strategy remain divided. Alex Thorn, Head of Research at Galaxy, noted that while this capital strategy might temporarily alleviate market concerns regarding MicroStrategy’s liquidity and preferred share redemption pressures, it primarily “buys time” rather than genuinely resolving its structural issues. MicroStrategy still carries substantial preferred share payment obligations. The market’s true concern isn’t a lack of assets, but whether the company possesses sufficient U.S. dollar liquidity to consistently meet its payment obligations without compromising the interests of common shareholders, preferred shareholders, or Bitcoin holders. The Bitcoin monetization plan, in particular, is contentious, as it implies MicroStrategy may sell portions of its Bitcoin holdings based on future funding needs. Given that MicroStrategy’s identity and MSTR’s premium are built upon its narrative as a long-term Bitcoin exposure vehicle, such sales could significantly dilute this core story.

Alex Thorn suggests that MicroStrategy should explore avenues to generate yield from its Bitcoin holdings, such as conservatively lending out small, segregated amounts of Bitcoin for interest, or employing options strategies to capture volatility premiums, rather than resorting to direct sales.

Considering the current scale of divestment, it remains plausible that MicroStrategy may continue to sell portions of its Bitcoin holdings based on market conditions. Investors should closely monitor the future scale, frequency, and trigger conditions of any subsequent sales. Should Bitcoin sales become a regular occurrence or even increase in volume, market confidence in MicroStrategy’s long-term holding strategy and capital operations could face renewed scrutiny. More broadly, MicroStrategy’s strategic pivot might just be the beginning. If, amidst Bitcoin price pressure and rising financing costs, an increasing number of “Bitcoin DAT” (Digital Asset Treasury) companies begin to emulate MicroStrategy by selling BTC to alleviate liquidity pressures, it could further depress coin prices and erode market confidence in the DAT model itself.

MicroStrategy’s long-held “hodling” conviction has been challenged, marking not merely a temporary stopgap but a genuine test of this high-leverage financial experiment during a downturn. Whether a business model so reliant on continuous capital market infusions can successfully navigate a bear market cycle remains an open question, with the answer perhaps just beginning to unfold.

(The above content is an excerpt and reproduction authorized by partner PANews. Original Link)

Disclaimer: This article is for market information purposes only. All content and views are for reference only and do not constitute investment advice. It does not represent the views or positions of BlockBeats. Investors should make their own decisions and trades. The author and BlockBeats will not bear any responsibility for direct or indirect losses resulting from investor transactions.