By Max, CryptoCity

US Treasury Redefines Stablecoin Issuers as Financial Institutions Under Groundbreaking GENIUS Act

In a pivotal move set to reshape the digital asset landscape, the U.S. Treasury Department officially initiated a critical regulatory framework on April 8th. Its Financial Crimes Enforcement Network (FinCEN) and Office of Foreign Assets Control (OFAC) jointly unveiled a proposed rule designed to fully implement the GENIUS Act, a landmark legislation passed in July 2025.

At the heart of this comprehensive regulatory push is the formal classification of “Permitted Payment Stablecoin Issuers” (PPSIs) as “financial institutions” under the stringent purview of the Bank Secrecy Act (BSA). U.S. Treasury Secretary Scott Bessent emphasized the dual objectives of this proposal: to fortify the U.S. financial system against evolving national security threats while simultaneously ensuring American enterprises maintain their competitive edge within the rapidly expanding payment stablecoin ecosystem.

This legislative drive underscores the Trump administration’s ambitious vision to position the United States as a global leader in digital assets, alongside a resolute commitment to national security defense.

Bolstering AML & Sanctions Compliance: Issuers Granted Authority to Freeze Transactions

Under these proposed regulations, stablecoin issuers will shoulder legal obligations mirroring those of traditional banking institutions. This mandates the establishment of robust Anti-Money Laundering (AML) and Combating the Financing of Terrorism (CFT) programs, alongside the crucial capacity to proactively detect and report suspicious activities. Critically, the new rules stipulate that issuers must possess the technical infrastructure and authority to “intercept, freeze, and reject” specific transactions, enabling swift action in response to law enforcement directives to block illicit fund flows.

Snir Levi, CEO of blockchain intelligence firm Nominis, highlighted the transformative nature of this shift, stating, “This change will essentially convert issuers into bank-like gatekeepers. We anticipate a significant increase in wallet freezes, transaction intercepts, and asset seizures across the market.”

The Treasury Department asserts that these obligations are “tailor-made” to be effective and proportionate. The official stance is to calibrate standards based on the size and operational complexity of each issuer, striving for a delicate balance between combating financial crime and fostering technological innovation, thereby avoiding an undue administrative burden on the industry.

Rigorous Compliance Officer Requirements & Collaborative Digital Cash Ecosystem

To guarantee the efficacy of these compliance programs, the proposal introduces stringent criteria for personnel appointments within issuing entities. Future stablecoin issuers will be required to designate a dedicated compliance officer responsible for overseeing AML and CFT defense systems. This individual must be a U.S. resident and is strictly prohibited from having any prior criminal record, including offenses such as insider trading, cybercrime, or financial fraud.

Beyond the Treasury, other key regulatory bodies, including the Federal Deposit Insurance Corporation (FDIC) and the Office of the Comptroller of the Currency (OCC), have also released their respective implementation guidelines. The FDIC, in its proposal, clarified a vital distinction: while stablecoin issuer reserve deposits will receive protection, individual stablecoin holders will not be afforded federal deposit insurance. Warren Kornfeld, Senior Vice President at Moody’s, suggests that the full implementation of these regulations will establish a multi-tiered “digital cash ecosystem” within the existing banking framework, further blurring the historical boundaries between traditional finance and digital assets.

- Related Insight: US FDIC Rules: Stablecoin Reserves Face Strict Requirements, No Individual $250K Deposit Insurance

Market Trajectories & Political Headwinds: Opportunities and Challenges for Stablecoin Issuers

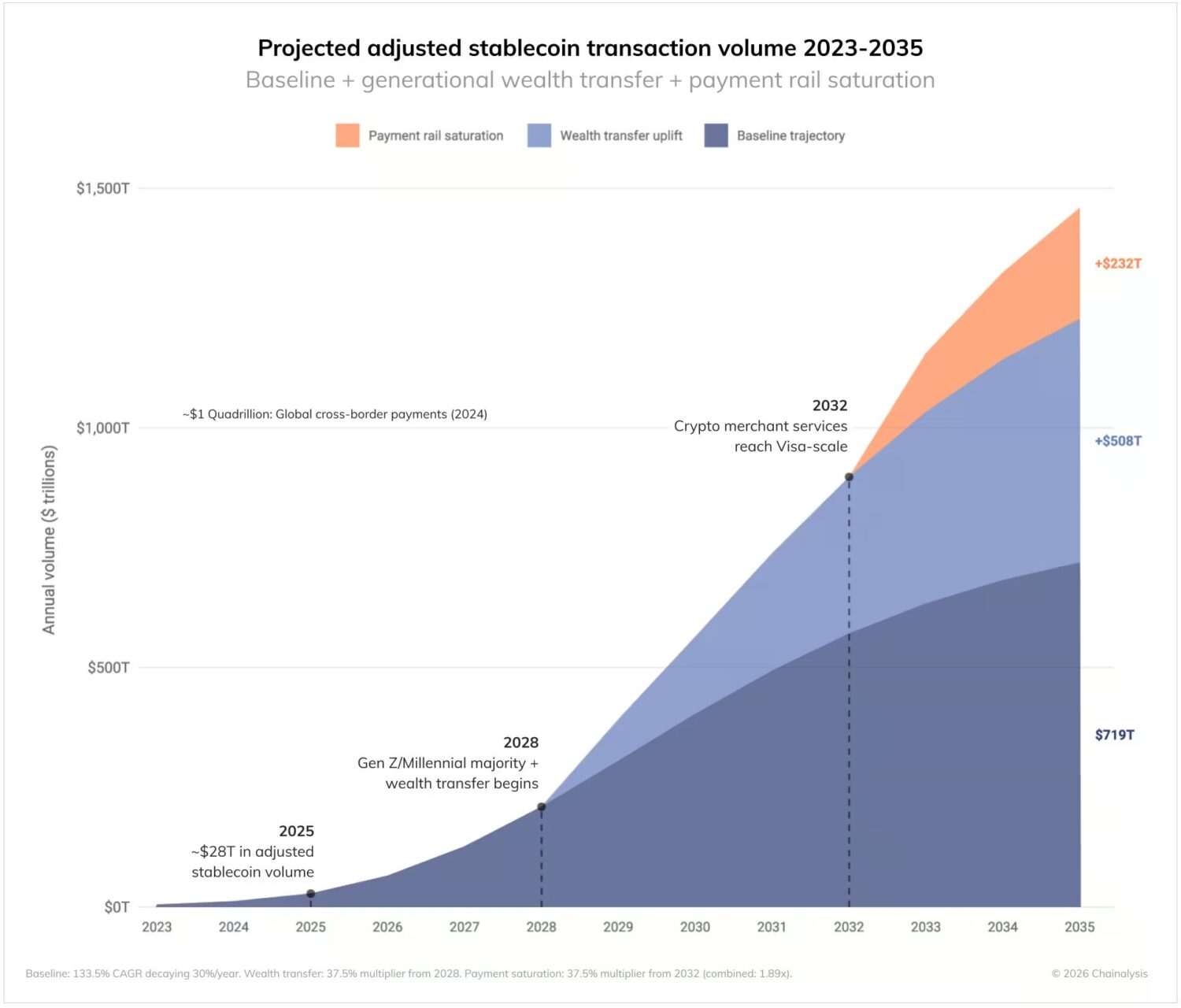

With the GENIUS Act slated for full enforcement by 2027, major stablecoin issuers such as Tether, Circle, Ripple, and the Trump-affiliated World Liberty Financial are keenly awaiting the finalization of these intricate rules. Despite the undeniable increase in regulatory scrutiny, industry consensus largely points to regulatory clarity as a catalyst for mainstream adoption of stablecoin assets. A report from Chainalysis projects an astounding surge in annual stablecoin transaction volume, potentially reaching $1.5 quadrillion by 2035.

Nevertheless, the political arena remains dynamic. Debates surrounding the Senate’s CLARITY Act are currently deadlocked, and the White House Council of Economic Advisers (CEA) has voiced opposition to a proposed stablecoin yield ban, arguing it would neither protect bank loans nor serve consumer interests, instead increasing user costs.

Globally, geopolitical tensions are also influencing the regulatory urgency. Iran’s recent announcement to impose a $1 per barrel Bitcoin toll on oil tankers traversing the Strait of Hormuz, ostensibly to circumvent sanctions, highlights the growing threat of illicit finance linked to such conflicts. This international backdrop further propels the U.S. Treasury’s accelerated efforts to establish robust control mechanisms through the GENIUS Act.

(The above content is an authorized excerpt and reprint from our partner “CryptoCity”, original link)

Disclaimer: This article provides market information only. All content and views are for reference purposes and do not constitute investment advice. They do not represent the views or positions of BlockTempo. Investors should make their own decisions and trades. The author and BlockTempo will not bear any responsibility for direct or indirect losses resulting from investor transactions.