Author: Nancy, PANews

Stablecoins Evolve: From Crypto Utility to Global Financial Cornerstone

The stablecoin landscape is undergoing a profound transformation, reshaping competitive dynamics as the era of compliance takes hold. USDC is expanding its influence through robust regulatory adherence and surging institutional demand, while USDT leverages its expansive global payment network to forge new growth avenues. This signals a clear divergence in their development paths.

Concurrently, innovative players like OUSD are disrupting the market with alliance distribution models, challenging the traditional growth and profitability paradigms of established stablecoin issuers. The stage is set for a significant re-calibration of the stablecoin ecosystem.

Beyond Crypto: Stablecoins Emerge as a New Global Asset Class

A recent Binance Research report, published on July 8, has captured significant market attention. Through extensive data analysis, the report systematically outlines the pivotal shift of stablecoins from mere crypto trading tools to essential global financial infrastructure, indicating their accelerating integration into mainstream financial systems.

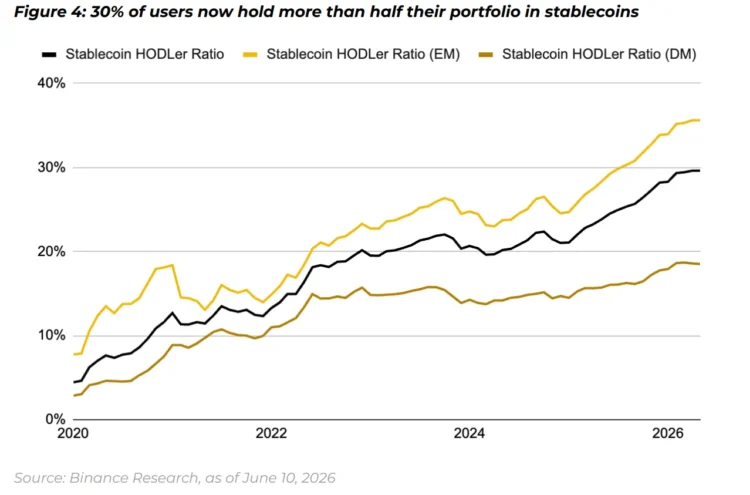

The report highlights a growing trend of users adopting stablecoins for long-term asset allocation. Approximately 30% of Binance users now allocate over half of their assets to stablecoins, a dramatic increase from just 4% in 2020. In emerging markets, stablecoins are becoming a vital alternative savings tool, offering a hedge against local currency devaluation, capital controls, and difficulties in accessing the U.S. dollar.

This trend is particularly pronounced in high-inflation economies. The report reveals that users in hyperinflationary environments sometimes pay premiums as high as 62% when acquiring stablecoins. This significant premium is not driven by transactional convenience but by the imperative to secure USD-denominated assets and preserve purchasing power.

Furthermore, the stablecoin ecosystem is evolving beyond simple value storage to encompass yield-generating assets. On-chain USD yield products are democratizing access to dollar-denominated income, offering a compelling alternative to traditional bank savings. Data from the report indicates on-chain USD yields of approximately 2-4%, with tokenized U.S. Treasury products mirroring traditional market returns, thus providing stablecoin holders with novel avenues for asset appreciation.

The utility of stablecoins is also transcending the crypto domain, establishing them as a crucial settlement layer bridging traditional finance and the blockchain world. The report points to the rapid growth in perpetual contracts linked to traditional financial assets. In the first five months of 2026, cumulative trading volume for “TradFi” perpetual contracts surpassed $1.1 trillion, representing about 11% of the total perpetual contract volume. Traditional assets such as equities, government bonds, and foreign exchange are now leveraging stablecoin infrastructure to enter on-chain systems, propelling financial markets towards 24/7, global operations. Stablecoins are transforming from mere crypto liquidity instruments into a critical gateway for the on-chain integration of traditional financial assets.

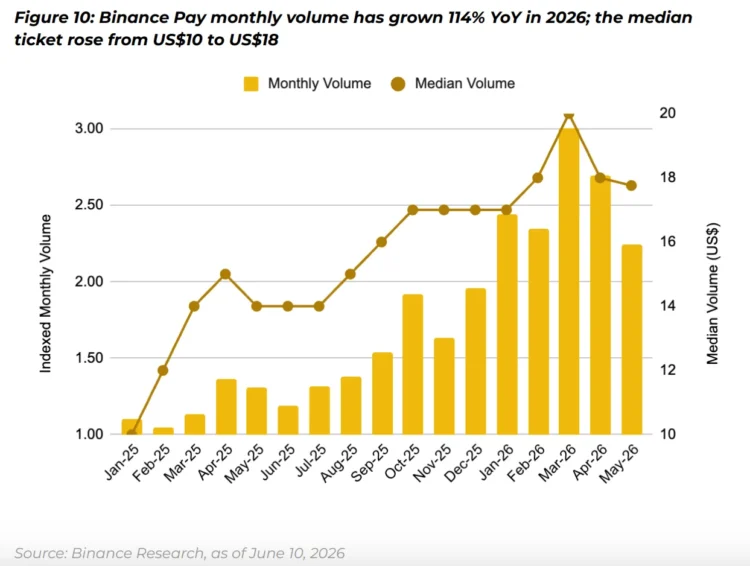

Concurrently, stablecoins are migrating from specialized financial trading into everyday payment applications. Binance Pay data illustrates this shift, with the median merchant payment amount increasing from $10 in 2025 to $18 in 2026, indicating a broader adoption of stablecoin payments beyond initial small-value crypto transactions into diverse commercial scenarios.

Regional markets exhibit distinct adoption patterns. Latin America has seen a remarkable surge in stablecoin transfer demand, with user share climbing from 17% in 2025 to 38%. Here, stablecoins are emerging as a key alternative for cross-border payments and remittances. East Asia and the Pacific, conversely, lead in stablecoin savings, contributing approximately 70% of Binance Earn’s stablecoin balances. The Middle East and North Africa region stands out as the fastest-growing savings market, experiencing a 67% increase in market share since 2025.

While USD-denominated stablecoins still dominate, the report also highlights the nascent but growing ecosystem of non-USD stablecoins. Local currency stablecoins, including EURI, AEUR, and KGST, have collectively surpassed $5 billion in cumulative trading volume on Binance since 2025, with an average monthly volume of $316 million. This evolution suggests that the future on-chain monetary system may not be solely reliant on the U.S. dollar but could evolve into a multi-currency global digital framework. The report also identifies AI payments and on-chain foreign exchange as two significant future growth areas.

In conclusion, the report asserts that with the continuous refinement of regulatory frameworks, enhanced reserve transparency, and expanding application scenarios, stablecoins are successfully transitioning from foundational crypto infrastructure to an indispensable component of the global financial system.

This data-driven analysis unequivocally demonstrates that stablecoins have transcended their initial role as niche tools for crypto trading, establishing themselves as a new financial rail connecting savings, payments, investments, and global settlements.

From Scale to Specialization: Stablecoins Enter an Era of Differentiated Competition

The mainstream adoption of stablecoins is inextricably linked to the accelerating era of compliance. This regulatory shift is not only fueling rapid market expansion but also fundamentally redefining the competitive landscape of the stablecoin industry.

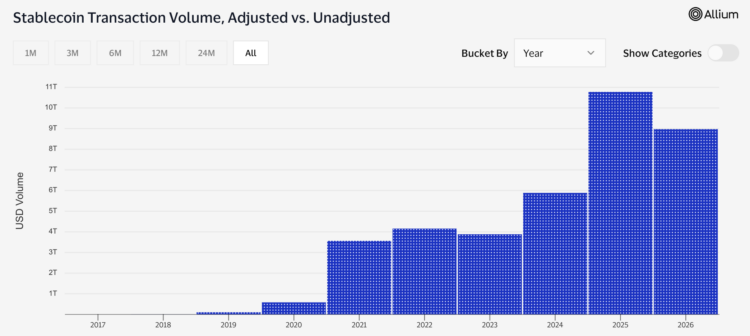

According to Visa’s on-chain dashboard data, the stablecoin market maintained robust growth through 2026. As of July 9, the total stablecoin transaction volume for the year has already reached an impressive $8.97 trillion. This figure not only surpasses the entire $5.89 trillion recorded in 2024 but also puts it within approximately $1.8 trillion of the all-time high of $10.78 trillion set in 2025.

Transaction activity has similarly surged. So far this year, the number of stablecoin transactions has hit approximately 1.3 billion, exceeding the full-year 2024 total and rapidly approaching the 2.25 billion transactions recorded in 2025.

These metrics underscore that stablecoins are not only facilitating increasingly vast capital flows but are also being deployed with greater frequency across diverse applications such as payments, settlements, and on-chain finance, solidifying their status as critical infrastructure for the digital economy.

However, the most compelling development in the stablecoin market this year isn’t merely the growth in scale, but rather the distinct and diverging development paths being carved out by different stablecoins.

Consider the two market leaders, USDT and USDC. USDC continues to amplify its influence in transaction volume and institutional adoption, buoyed by an improving regulatory environment and escalating institutional demand. Meanwhile, USDT, leveraging its long-established and extensive circulation network, maintains a strong advantage in payment and value transfer scenarios.

Visa data, as of July 9, indicates that USDC’s cumulative transaction volume this year (after filtering out bot activity, exchange transfers, and other non-economic transactions) exceeded $5.66 trillion, capturing approximately 63.1% of the total stablecoin transaction volume. USDT’s transaction volume during the same period stood at $3.27 trillion, accounting for about 36.4%.

Despite this, USDT still demonstrates higher activity in terms of transaction count. Year-to-date, USDT has processed over 930 million transactions, compared to approximately 360 million for USDC, meaning USDT’s transaction frequency is about 2.6 times higher.

When viewed alongside transaction volume, this disparity highlights the distinct market positioning of the two stablecoins. While USDC has fewer transactions, its higher average transaction size signifies its role in handling institutional funds, large-value settlements, and on-chain financial demands, a position significantly bolstered by the evolving global stablecoin regulatory frameworks. USDT, conversely, relies on its broad user base and extensive circulation network, maintaining robust penetration in high-frequency trading, cross-border payments, and everyday value transfer applications.

Evidently, USDT and USDC are each cultivating unique network effects along their divergent development trajectories.

Dune Analytics data for the first half of 2026 reveals that USDT settled approximately $95 billion in identified on-chain commercial payments, significantly more than USDC’s roughly $14 billion. In the business-to-business (B2B) payment sector, USDT commanded an impressive 92% market share, representing approximately $48 billion in payment volume. Furthermore, on the Tron network, 93% of USDT is held in ordinary wallets rather than exchanges, further cementing USDT’s role as a crucial tool for cross-border payments, remittances, and value transfers, rather than merely a trading medium.

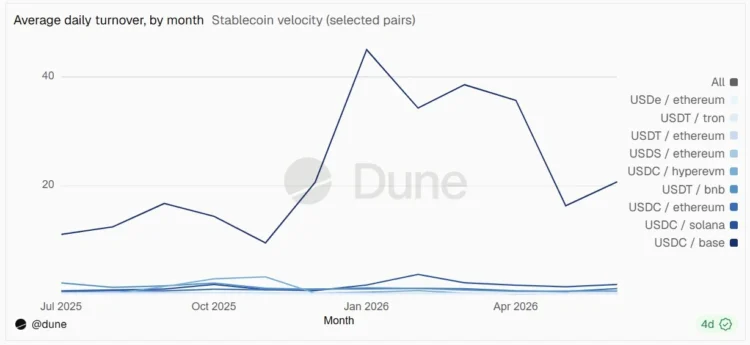

In stark contrast, USDC has emerged as the stablecoin of choice within the Decentralized Finance (DeFi) ecosystem. In June, USDC processed approximately $2.6 trillion in transfers on the Base chain and about $1.6 trillion on Ethereum. Its daily turnover rate reached an astonishing 20 times its circulating supply, underscoring its widespread use in trading, liquidity provision, and various DeFi protocols.

This clear distinction underscores that the stablecoin market is indeed entering an era of specialized, scenario-based competition.

Compliance as the New Frontier: Tether’s Strategic Response

As stablecoins navigate the compliance era, USDT is undeniably facing unprecedented competitive pressures. The entry of traditional financial institutions, armed with licensing advantages, robust compliance capabilities, and established institutional trust, is steadily encroaching upon the market share USDT previously secured through its first-mover advantage.

Most recently, with the conclusion of the MiCA regulatory transition period, Tether proactively withdrew from Europe. In contrast, USDC, having swiftly completed its compliance review, capitalized on this regulatory dividend, further solidifying its leading position in compliant European and American markets.

However, Tether has opted not to engage in direct competition with USDC in mature, highly regulated markets. Instead, it is actively seeking new growth opportunities. In recent times, Tether has been simultaneously expanding USDT’s payment network and aggressively pursuing strategic deployments in emerging markets and a diversified asset ecosystem.

On one front, Tether is relentlessly expanding USDT’s payment network and circulation capabilities. Recently, Tether announced USDT’s impending return to the Bitcoin network, with plans to natively issue USDT via the RGB protocol. UTEXO will oversee its commercial deployment, with an official launch anticipated as early as July. This innovative solution will support native Bitcoin addresses and Lightning Network transfers, combining RGB client-side validation with the Bitcoin UTXO model to deliver enhanced privacy, instant settlement, and low-cost payments. This marks USDT’s first return to the Bitcoin network in many years since its initial issuance via the Omni protocol in 2014.

On another front, Tether is rapidly building localized compliance networks in emerging markets. In April, Tether co-led an $8 million strategic funding round for KAIO, an Abu Dhabi-based compliant tokenization platform. KAIO holds relevant financial services licenses from the ADGM FSRA, providing essential compliant infrastructure for tokenized assets in the Middle East. The following month, Tether announced an investment in LemFi, a cross-border financial platform, with the goal of advancing stablecoin-driven remittance services in emerging markets and broadening financial accessibility. More recently, Tether disclosed a $20 million investment in Mercado Bitcoin, Latin America’s largest on-chain financial platform, which serves approximately 4.5 million users and holds over 10 regulatory licenses across Brazil and Europe.

These strategic investments are designed to establish compliant gateways and robust payment networks for Tether in key emerging markets. This proactive approach is no accident; compared to the increasingly stringent and competitive European and American markets, emerging economies currently represent the most fertile ground for stablecoin growth.

Beyond expanding the USDT network, Tether has also begun to unlock the financial value of its substantial gold reserves, aiming to reduce its sole reliance on stablecoin operations. As the largest holder of gold reserves outside of sovereign nations and banks, Tether commands approximately $23 billion in gold. Last month, it announced a partnership with digital bank and investment platform Fasset to launch the world’s first gold-backed Visa card, seamlessly integrating gold assets into everyday payment scenarios. Recently, Tether also unveiled plans to introduce XAUT collateralized lending services this year, connecting them to the crypto lending platform Ledn, thereby further enhancing asset utilization efficiency and diversifying its revenue streams.

The continuous influx of new players, the relentless iteration of business models, and the gradual establishment of new regulatory frameworks are fundamentally altering the competitive dynamics of the stablecoin industry. As stablecoins evolve from mere USD substitutes into indispensable global financial infrastructure, the traditional model of passively profiting from reserve yields faces multifaceted challenges. Issuers like Tether are now compelled to actively seek out more diverse application scenarios and new profit growth points to ensure long-term competitiveness in this rapidly evolving landscape.

(The above content is an excerpt and reproduction authorized by our partner PANews. Original link)

Disclaimer: This article is for market information purposes only. All content and views are for reference only and do not constitute investment advice. They do not represent the views and positions of BlockTempo. Investors should make their own decisions and trades. The author and BlockTempo will not bear any responsibility for direct or indirect losses resulting from investor transactions.